A private company can pay dividends to shareholders by distributing profits after company tax has been paid. Directors must ensure the company can afford the payment, follow the company constitution, and formally declare the dividend before it is paid.

The dividend is then reported to shareholders with a dividend statement and may include franking credits representing tax already paid.

For a private company, dividends are a common way to distribute profits to shareholders. However, the company must meet legal and financial requirements before a dividend is paid.

A typical dividend payment process in Australia includes the following steps.

- Confirm the company has sufficient profits: Dividends are generally paid from retained earnings after company tax.

- Check the company constitution: The constitution may set rules on how dividend payments are approved and paid to shareholders.

- Declare the dividend: The company director or board passes a resolution confirming the dividend declaration.

- Decide whether the dividend is franked or unfranked: The company determines whether franking credits will be attached based on tax already paid.

- Issue dividend statements: Shareholders receive a statement showing the dividend amount, franking credits and payment date.

- Pay the dividend to shareholders: The company pays the dividend based on the number of shares each shareholder owns.

The Australian Taxation Office (ATO) requires dividend payments and franking credits to be properly recorded because shareholders must report dividend income on their tax return.

What are dividends and how do they work?

Dividends are payments a company makes to its shareholders from profits. When a company earns income and pays company tax, the remaining profit can be distributed as a dividend to shareholders.

Dividends represent a share of the company’s profits, which is why choosing the right business structure is important. If you own shares, you may receive part of these profits when the company pays dividends.

For example, if a company earns $100,000 in profit and pays company tax, the remaining profit may be paid as a dividend. Each shareholder receives a portion of the company's profits based on the number of shares they hold.

Dividends are usually paid in cash, although some companies may offer dividend reinvestment plans that allow shareholders to receive additional shares instead of cash.

Dividends may be fully franked, partly franked, or unfranked. When franking credits are attached, they represent company tax that has already been paid. Shareholders include dividend income and franking credits in their personal tax return and may receive a tax offset, depending on the applicable structure they hold their shares in, e.g., Family Trust, Company, or Personal names.

Why companies pay dividends to shareholders

Companies pay dividends to shareholders to distribute profits generated by the business. When a company earns income and pays company tax, the remaining profit can be returned to the business's owners as dividend payments.

In private companies, dividends are commonly used to provide income to business owners who hold shares. Instead of retaining all profits in the company, directors may decide to distribute part of them to shareholders.

There are several reasons companies pay dividends.

- Returning profits to owners: Dividends allow shareholders to receive income from the company’s performance.

- Managing retained earnings: Paying dividends can reduce excess profits held within the company.

- Providing regular shareholder income: Some companies establish a dividend policy so shareholders receive payments once or twice a year.

- Tax planning for business owners: Dividend income may be distributed to shareholders in a way that aligns with their personal tax position.

Directors must ensure the company still has the ability to pay its creditors after the dividend is paid. This is an important legal requirement under Australian corporate law.

For example, a consulting business operating through a company structure may generate $200,000 in annual profit. After company tax is paid, the directors may declare a dividend and distribute part of the remaining profit to shareholders.

If those shareholders have different marginal tax rates, dividend payments can be structured to efficiently distribute income while remaining compliant with Australian tax rules.

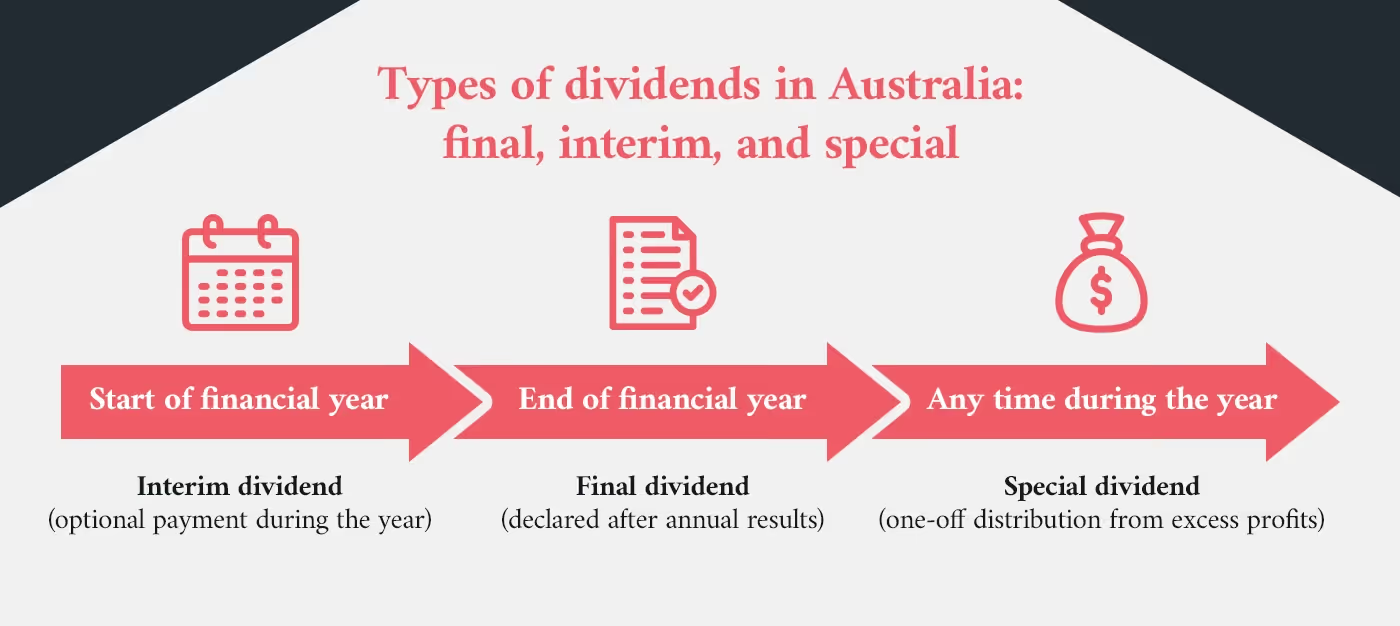

Types of dividends explained: final, interim, and special

Companies can pay several types of dividends depending on when the payment is made and why it is declared. The most common dividend types are final, interim, and special dividends.

Final dividends

A final dividend is usually declared at the end of a financial year once the company’s financial results are confirmed. It represents a distribution of profits after the company’s annual performance has been reviewed.

Interim dividends

An interim dividend is paid during the financial year before the company prepares its annual financial statements. These dividends are often declared when the company has strong cash flow or profits during the year.

Special dividends

A special dividend is a one-off payment made outside the company’s normal dividend schedule. Companies may pay a special dividend after a large profit, the sale of an asset, or when excess cash is available.

In many companies, dividends are usually paid twice a year through interim and final dividend payments. Private companies, however, have greater flexibility and may pay dividends whenever profits and cash flow allow.

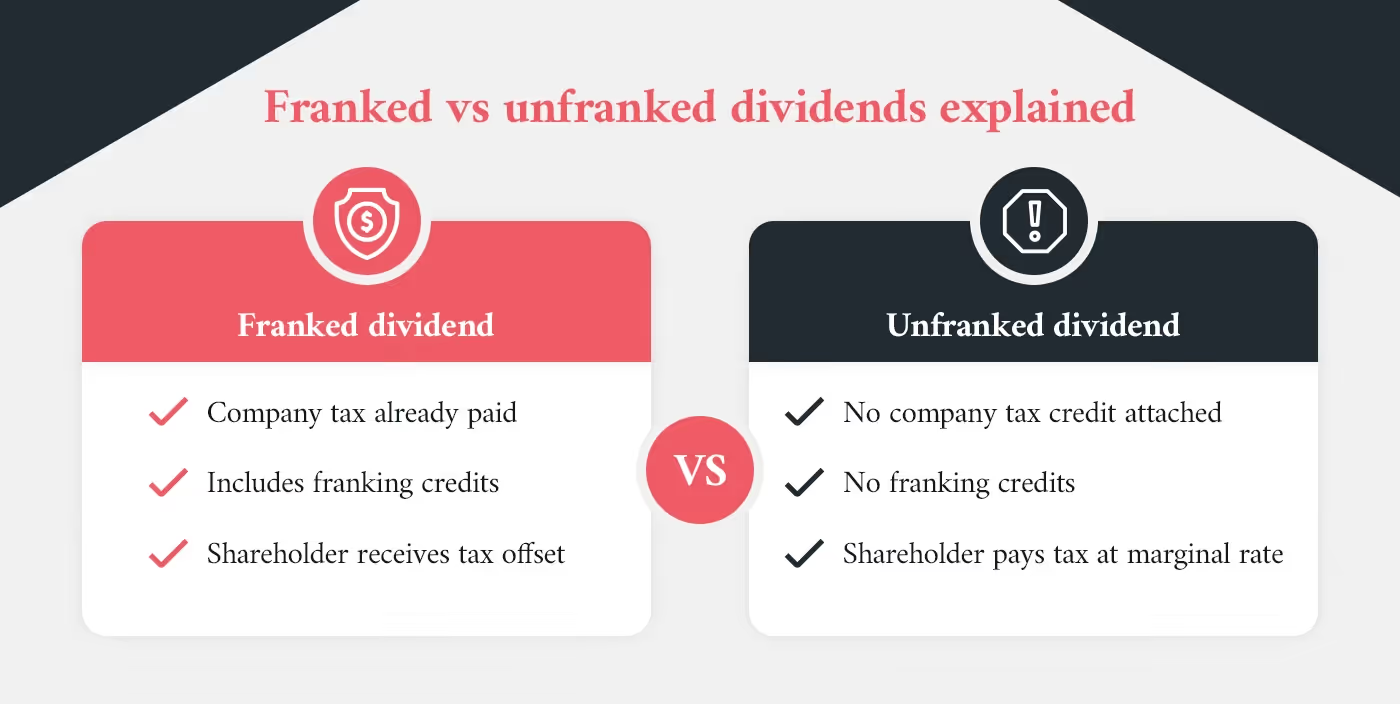

What are franked and unfranked dividends?

Franked and unfranked dividends describe how company tax has been treated before the dividend is paid to shareholders.

A franked dividend is paid from profits on which the company has already paid tax. The dividend includes franking credits that represent the company tax already paid. These credits are attached to the dividend, so shareholders do not pay tax twice on the same income.

For example, if a company pays tax on its profits and then distributes those profits as a dividend, the franking credits reflect the tax already paid at the company tax rate. Shareholders include both dividend income and franking credits in their personal tax returns.

An unfranked dividend is paid from profits for which company tax has not been paid, or for which franking credits are not attached. Because no franking credits are applied, the full dividend amount may be taxable on the shareholder’s personal tax return.

Understanding the difference between franked and unfranked dividends is important because it affects the amount of tax shareholders may be required to pay on their dividend income.

How much tax do you pay on dividends in Australia?

Dividend tax depends on whether the dividend is franked or unfranked and the shareholder’s marginal tax rate. When a company has already paid company tax on its profits, franking credits may be attached to the dividend. These credits represent tax already paid and can reduce the amount of personal tax a shareholder must pay.

When shareholders receive a dividend, they must include both the dividend income and any franking credits in their personal tax return. The total is added to their taxable income and taxed at their marginal tax rate. The franking credits are then applied as a tax offset.

The following table shows a simplified example of how dividend tax works.

[table]

[thead]

[tr]

[th]Dividend type[/th]

[th]How tax is treated[/th]

[th]Shareholder tax outcome[/th]

[/tr]

[/thead]

[tbody]

[tr]

[td]Fully franked dividend[/td]

[td]Company tax has already been paid and franking credits are attached[/td]

[td]Franking credits offset personal tax. Shareholders may pay extra tax or receive a refund depending on their marginal tax rate[/td]

[/tr]

[tr]

[td]Partly franked dividend[/td]

[td]Only part of the dividend has franking credits attached[/td]

[td]The franked portion receives a tax offset, while the unfranked portion is taxed at the shareholder’s marginal rate[/td]

[/tr]

[tr]

[td]Unfranked dividend[/td]

[td]No franking credits are attached because company tax has not been applied to the payment</td]

[td]The full dividend amount is generally taxed as ordinary income in the shareholder’s personal tax return</td]

[/tr]

[/tbody]

[/table]

Because dividend income affects both corporate and personal tax outcomes, many business owners carefully plan dividend payments. Working with a business accountant can help ensure dividend distributions are structured correctly and reported to the ATO.

Step-by-step: how to declare and pay dividends

Declaring a dividend is a formal process where company directors approve the distribution of profits to shareholders.

Before a company can pay a dividend, directors must confirm the company's ability to pay and ensure the payment of dividends will not affect its ability to meet its obligations. Certain payments to shareholders may also fall within the Division 7A rules on private company payments, which can treat them as dividends for tax purposes.

A dividend can be paid only after the directors determine that sufficient profits exist and that the payment is lawful under the company's constitution and Australian corporate rules. Once the dividend is declared, the company must record the payment and issue documentation for shareholders to report to the ATO.

Review the company’s profits and financial position

Directors must confirm the company's ability to pay and ensure the dividend can be paid without affecting creditors. The dividend to be paid must come from profits for which company tax has already been paid.

Determine the dividend amount

The board decides how much profit the company will distribute. In some cases, directors may intend to pay a large dividend if retained earnings are high.

Pass a resolution declaring a dividend

The directors formally approve the dividend. When the dividend is declared, it becomes the company’s obligation to complete the payment of the dividend to shareholders.

Determine the franking status

The company decides whether the dividend will include franking credits, also called bonus tax credits, which represent tax paid on those profits.

Issue shareholder dividend statements

Each shareholder receives a shareholder dividend statement showing the dividend amount, franking credits and the payment date.

Complete the dividend payment

The company issuing the dividend pays shareholders according to their shareholding. Shareholders who are eligible to receive the dividend must report the income on their personal tax return.

When and why companies pay dividends

Companies pay dividends when they have profits available to distribute to shareholders. Dividends paid represent the return business owners receive from the company’s performance. Many business owners use dividends as part of their income strategy after understanding the benefits of setting up a company structure.

Dividends are usually paid once or twice a year. A company may declare an interim dividend during the year and a dividend at the end of the financial year once profits are confirmed.

The timing of dividend payments depends on several factors:

- the company's ability to pay its creditors

- retained earnings and cash flow

- the company’s dividend policy

- whether directors intend to pay a large dividend or retain profits for growth

Dividends are most commonly paid in cash. In some cases, shareholders may reinvest the dividend and receive additional shares in the company instead.

Private companies have flexibility in when they distribute profits, which means business owners often plan when dividends are paid as part of their overall income strategy.

How franking credits affect dividend taxation

According to the ATO, franking credits represent company tax already paid before dividends are distributed. These credits are attached to dividends, so the same income is not taxed twice.

When paying franked dividends, companies must comply with the ATO's benchmark franking percentage rules by applying the correct franking percentage. The franking credits reflect company tax already paid. Shareholders include both the dividend and the franking credits in their tax return.

If a shareholder has a low marginal tax rate, the credits may reduce the tax payable or result in a refund. If their marginal rate is higher than the company tax rate, they may still be liable to pay income tax on part of the dividend.

If a dividend is unfranked, no credits are attached. In this case, the shareholder may be liable to pay income tax on the full dividend amount depending on their personal tax position.

Are dividends from private companies taxable?

Yes, dividends from private companies are generally taxable in Australia. When dividends are paid to shareholders, the amount received is included in their assessable income and reported in their personal tax return.

Dividends work by distributing company profits to shareholders when a business operates through a company structure. Once the company has paid tax on those profits, it may distribute the remaining earnings to owners as income, known as a dividend. Shareholders who are eligible to receive the payment must declare the dividend income to the ATO.

Dividends are most commonly paid in cash, but they can also be distributed in other ways. For example, dividends may be issued in the form of additional shares under a dividend reinvestment plan.

In some situations, payments made by a company may be treated differently for tax purposes. For instance, a payment may be treated as a return of capital rather than a dividend. This distinction is important because returns of capital payments may be taxed as capital gains rather than as ordinary dividend income.

Because tax treatment can vary depending on the circumstances, shareholders should understand how dividends work and how different distributions may be treated when preparing their tax return.

Which dividends are tax-free or exempt in Australia

Most dividends paid by Australian companies are taxable, but some payments may be treated differently depending on the circumstances.

In certain cases, a distribution may not be treated as a standard dividend. For example, a company may distribute funds to shareholders as a return of capital rather than a profit distribution known as a dividend. A return of capital may affect the cost base of shares and may trigger capital gains tax if the payment exceeds the share’s cost base.

The company's structure may also influence how distributions are treated. Companies with different classes of shares may distribute profits to different classes of shareholders depending on the rights attached to those shares.

Timing can also matter. Transactions occurring immediately before the dividend may influence how a distribution is classified or whether a shareholder is eligible to receive it.

Because companies may distribute profits in different ways, some payments may be treated differently for tax purposes.

[free_strategy_session]

Book a free financial strategy session

Get the tools you need to make an immediate impact

- Get a better understanding of your needs

- We generate a detailed report from your strategy session

- Understand your priorities and next steps

[/free_strategy_session]

How to declare dividends on your tax return in Australia

Dividend income must be reported on your personal tax return in the year the dividend is paid. When dividends are paid to shareholders, the payment and any franking credits are shown on the company's shareholder dividend statement.

The dividend statement includes the total dividends paid, the amount of franking credits attached, and the payment date. These details are required when declaring dividend income in your tax return with the ATO.

When preparing your return, shareholders include:

- the total dividend amount received

- any franking credits attached to the dividend

- whether the dividend is franked or unfranked

The ATO uses this information to determine how the dividend is taxed. Franking credits represent tax that has already been paid on those profits and may reduce the tax payable.

Because dividends work as a distribution of company profits, shareholders who are eligible to receive the dividend must report the income, even if the payment was reinvested through a dividend reinvestment plan.

If a payment from a company is not treated as a standard dividend, it may be classified differently for tax purposes. In some cases, distributions may be treated as a return of capital rather than dividend income, which can affect capital gains tax instead of ordinary income tax.

Get professional help with dividend tax and compliance

Paying dividends correctly requires more than simply distributing profits. Directors must confirm the company’s ability to pay, ensure the dividend is declared properly, and provide shareholders with accurate dividend documentation for ATO reporting.

Liston Newton provides dividend advice and compliance support to help business owners structure dividend payments correctly. Our team can guide you on declaring dividends, managing franking credits, and ensuring dividend distributions comply with tax and company rules.

If you are planning to pay dividends from a private company, speak with the Liston Newton team for clear advice on dividend tax and compliance.