Are super contributions tax deductible? Yes. In fact, superannuation isn’t just a way for you to save for retirement — it’s one of the most effective tax minimisation tools available to high-income earners. By making super contributions, you can claim tax deductions, lower your taxable income, and build long-term wealth in a tax-friendly environment.

But to get the most out of your super, you need to understand how the system works. The tax benefits change depending on your income, your business structure, and whether you’re in the accumulation or pension phase. Done right, you can significantly reduce how much you pay in tax — both now and in the future.

In this guide, we’ll explore the key tax advantages of super, including:

- How you can claim tax deductions for your super contributions

- Why super is a powerful tool for future financial planning

- How high earners like you can protect your assets using super

- The best superannuation tax strategies to reduce your tax bill and grow your wealth

Smart tax planning starts with knowing what’s possible. For personalised advice on using super to minimise tax, speak with our award-winning SMSF advisors today. We’ll help you tailor a strategy that fits your business, your financial goals, and your stage of life.

[smsf_awards][/smsf_awards]

Super contributions tax for high-income earners: what you need to know

As a high-income earner in Australia, you pay a 15 per cent tax on concessional super contributions, including employer and salary sacrifice contributions. However, if your income exceeds $250,000, you may be subject to Division 293 tax, which applies an additional 15 per cent tax on contributions — bringing the total tax to 30 per cent. Despite this, contributing to super remains one of the most tax-effective ways for you to reduce taxable income, as it is significantly lower than the top marginal tax rate of 45 per cent.

Super contributions are generally taxed at just 15%, with capital gains on assets held for over 12 months taxed at just 10%. Once you turn 60 and retire, both withdrawals and investment earnings become entirely tax-free — making super a highly effective way to grow your wealth while minimising tax.

[tip_box]

How your income affects super tax benefits

The tax advantage of super contributions comes from the difference between your income tax rate and the super tax rate, which is generally 15 per cent.

- Earn up to $18,200: No income tax, but super still taxed at 15% (minimal benefit).

- Earn $18,201 – $45,000: Income tax up to 19%, super still 15% (small savings).

- Earn $45,001 – $135,000: Income tax up to 30%, super 15% (save up to 15% tax per dollar contributed).

- Earn $135,001 – $190,000: Income tax 37%, super 15% (save 22% tax per dollar contributed).

- Earn over $190,001: Income tax 45%, super 15% (save 30% tax per dollar contributed).

Extra tax for high earners

If your income + super contributions exceed $250,000, Division 293 tax applies, increasing your super tax rate to 30% — still lower than the 45% income tax rate.

Even with extra tax on high earners, super remains one of the best ways to reduce taxable income and grow wealth tax-efficiently.

[/tip_box]

Superannuation and tax: myths vs. reality

Superannuation is one of the most tax-effective ways to build wealth, but there are plenty of misconceptions about how it works. By understanding the facts, you can make the most of its benefits while avoiding costly misconceptions. Let’s separate fact from fiction so you can make informed financial decisions.

Myth 1: You can’t access your super until you retire

Reality: While super is primarily designed for retirement, there are exceptions where you may be able to claim a tax-free withdrawal. For example, in cases of severe financial hardship or under the First Home Super Saver Scheme, eligible individuals can access their super contributions early.

Myth 2: Superannuation contributions aren’t tax-deductible

Reality: If you make a personal contribution to your super, you can often claim a tax deduction for it. Concessional contributions, such as salary sacrifice or personal deductible contributions, reduce your taxable income — helping you pay less tax.

Myth 3: Super co-contributions are only for low-income earners

Reality: The government’s super co-contribution scheme provides a tax-free boost to your super if you make after-tax personal contributions and earn income below a certain threshold. Even if you’re a high-income earner, other tax benefits — such as concessional contributions caps — can help you grow your super while reducing your income tax.

Myth 4: Once you contribute to super, you can’t change your investment strategy

Reality: You have full control over how your super is invested. Whether you’re in an industry fund, retail fund, or self-managed super fund (SMSF), you can adjust your investment options to suit your risk tolerance and financial goals.

Myth 5: You don’t need to worry about super if you’re self-employed

Reality: If you're self-employed, you won’t receive employer super guarantee contributions — but you can, and should, make your own contributions. Doing so not only offers valuable tax benefits but also helps you build a strong financial foundation for retirement.

Claim tax deductions through super to reduce your taxable income

Making super contributions is not just about preparing for retirement — it is one of the most effective ways for you to reduce taxable income while growing your long-term wealth. Tax-deductible super contributions allow you to lower your tax bill and retain more of your profits.

Here’s how you can claim tax deductions on super contributions:

Pay super directly from your business

If you pay your own super as an employee of your business, you can claim a tax deduction as part of your business expenses. This reduces your business’s taxable income and overall tax liability.

Contribute personally and claim the deduction when you lodge your tax return

If you make super contributions from your personal funds, you may be eligible to claim a deduction in your personal tax return. This reduces your individual taxable income while still building your retirement savings.

Key considerations to keep in mind

- Annual concessional cap: The maximum tax-deductible contribution is currently $30,000 per year, including employer contributions.

- Carry-forward contributions: If your total super balance is under $500,000, you can carry forward unused concessional contributions for up to five years. This allows you to make larger contributions in high-income years to maximise deductions.

- Tax on contributions: While super contributions are taxed at 15 per cent, this is still significantly lower than the highest marginal tax rate of 45 per cent, making super a tax-effective strategy for high-income earners.

Strategic use of super contributions can help you minimise tax, improve cash flow, and build wealth in a way that is both legally compliant and financially beneficial.

Is it worth claiming a tax deduction on super contributions?

How valuable tax deductions on super contributions are depends on how much you earn. If you’re a high-income earner, contributions will help you reduce taxable income and grow your retirement savings in a low-tax environment. Your personal concessional contributions are taxed at 15 per cent — or 30 per cent if you earn over $250,000 — which is still much lower than the 45 per cent top marginal tax rate. This means every dollar you contribute to super reduces your overall tax liability while benefiting from long-term, tax-effective investment growth. However, the benefits depend on your financial situation and cash flow. If you expect a lower income in the future, you may want to carry forward unused concessional cap amounts to maximise deductions in higher-income years.

Use super to grow wealth and pay less tax in retirement

Superannuation is one of the most tax-effective investment vehicles available to business owners. By keeping your investments inside your super fund, you can pay less tax and build long-term wealth while preparing for retirement.

If you hold investments outside of super, any income or capital gains may be taxed at your marginal tax rate, which could be as high as 45 per cent. However, investments held within super are taxed at significantly lower rates:

- Investment income (such as dividends or interest) is taxed at only 15 per cent.

- Capital gains tax (CGT) is taxed at 10 per cent if the investment is held for more than 12 months.

Once you reach age 60 and stop working, the tax benefits become even greater:

- 0 per cent tax on investment income

- 0 per cent capital gains tax

- 0 per cent tax on withdrawals from your super

This means that, with the right planning, you can build wealth inside super while paying less tax during your working years — and eventually access your super tax-free in retirement.

How you can make the most of super investments

- Consider holding long-term investments inside super to benefit from lower tax rates.

- Maximise concessional contributions while you are earning a high income to reduce your tax bill and boost your retirement savings.

- Use salary sacrifice arrangements to make additional contributions and take advantage of the 15 per cent tax rate.

If structured correctly, superannuation can be a powerful tax-saving tool that helps you protect your wealth while setting yourself up for financial security in retirement.

Protect your super from creditors in case of bankruptcy

For business owners like you, financial risks are unavoidable. Market downturns, cash flow issues, or unforeseen challenges can sometimes lead to financial difficulties. One of the major benefits of superannuation is that it is generally protected from creditors, making it a valuable asset protection strategy in the event of bankruptcy.

How your super is protected in bankruptcy

Your superannuation benefits do not form part of a bankrupt estate. This means that if you become insolvent, your super is not typically included in the assets a trustee can claim.

Funds held within a regulated super fund remain protected, ensuring that your retirement savings are safeguarded — even if your business fails.

Important considerations

Super contributions made before bankruptcy can be reviewed by the courts. If you transfer large amounts of money into super with the intention of avoiding creditors, these funds may be clawed back by the trustee in bankruptcy.

Transfers into super should be part of a long-term financial strategy — not a last-minute protection tactic. Regular, strategic super contributions are unlikely to be challenged, whereas sudden large transfers just before bankruptcy may raise legal concerns.

How you can use super for asset protection

- Make regular super contributions over time rather than large lump sums when financial difficulties arise.

- Use super as part of a broader wealth-building strategy, ensuring that your retirement savings remain protected while also benefiting from tax advantages.

- Seek professional advice before making large contributions to ensure compliance with superannuation and bankruptcy laws.

No one can avoid facing at least some degree of financial hardship; superannuation provides an essential safety net for business owners like you, ensuring that your retirement savings remain secure and protected — even in tough times.

[free_strategy_session]

Free financial strategy session

A 90-minute strategy session gives you a clear plan for claiming super contributions as a tax deduction, without the confusion.

- Get clarity on how personal and business super contributions are treated

- Receive tailored advice on maximising deductions and avoiding common errors

- Understand timing, caps and compliance requirements for your situation

[/free_strategy_session]

Superannuation strategies to minimise tax and build wealth

Maximise the $30,000 tax deduction

If your cash flow allows, maximising concessional contributions is a great way to minimise tax and set yourself up for later in life. Over the course of a financial year, you can contribute $30,000 into super and claim it as a tax deduction.

Running a business from a family trust can offer flexibility in maximising super contributions. A common scenario is distributing profit to a family member and then having them contribute the money to super and claim a tax deduction.

Let’s take a look at an example

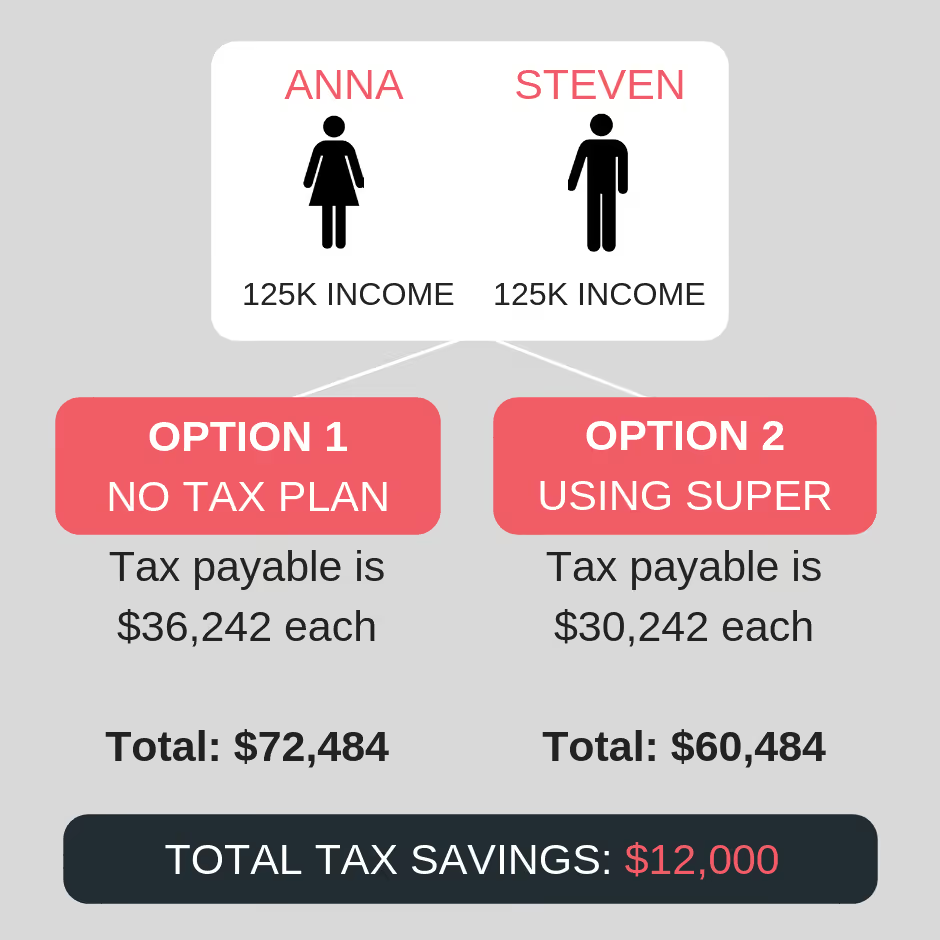

Steven and Anna are husband and wife. They run a bakery together and use a family trust structure. This financial year, the bakery has $250,000 in profit.

- If no tax planning takes place, Steven and Anna each receive a distribution of $125,000 and have tax payable of $36,242 each.

- If they contribute $30,000 into super, their taxable income is reduced to $100,000, and their tax payable drops to $26,117 each.

- Both Steven and Anna save $10,000 in tax on their personal tax returns.

- When you contribute to super and claim a tax deduction, you will pay $3,750 in tax from your super fund at the 15% rate — still representing a saving of over $6,000 each.

A step further

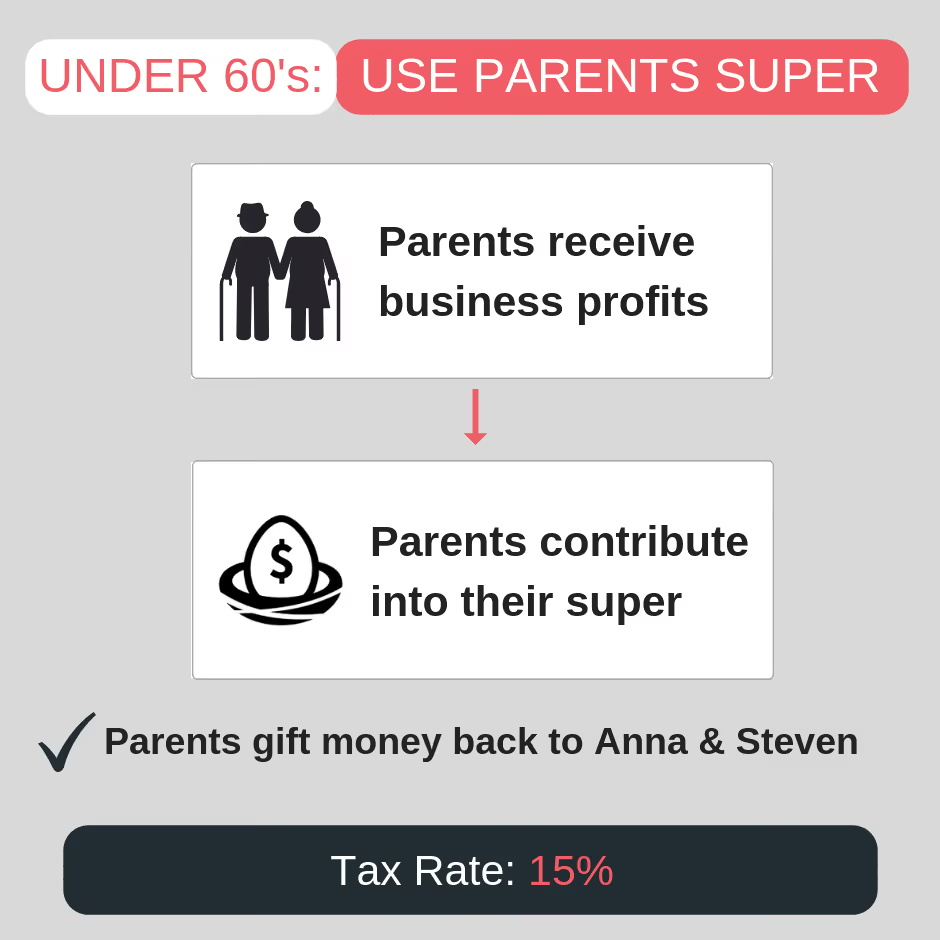

This strategy becomes even more effective when those making the contributions are over the age of 60.

For example, if Steven and Anna were 65, they could contribute money into super, claim the tax deduction, and then withdraw the money again.

If they were not yet 60, they could use their parents as a beneficiary of the trust:

- The parents receive the business profits and contribute them into super.

- They pay 15% tax on this contribution and then withdraw the money.

- The parents then gift the money back to Steven and Anna or use it for expenses like school fees.

2. Buy commercial property in your SMSF

Another smart strategy is to purchase a commercial property through your Self-Managed Superannuation Fund (SMSF). If structured correctly, you can rent the property back to your business — provided it’s done at commercial market rates. This is a legal and tax-efficient way to build wealth inside your super while supporting your business.

For example, if you own a professional services firm, you may choose to buy an office through your SMSF:

- You can borrow within your SMSF to buy the property (typically up to 60% to 70% of the purchase price).

- You need a minimum deposit of 30% to 40% in your SMSF, plus stamp duty.

- Once the property is purchased, you can rent it out to your business.

- Your business pays rent into your SMSF, which is then claimed as a rental expense by your business.

- If your SMSF has a loan, the interest on the loan will mostly offset the income, reducing taxable earnings.

- If there is no loan, your SMSF pays only 15% tax on rental income.

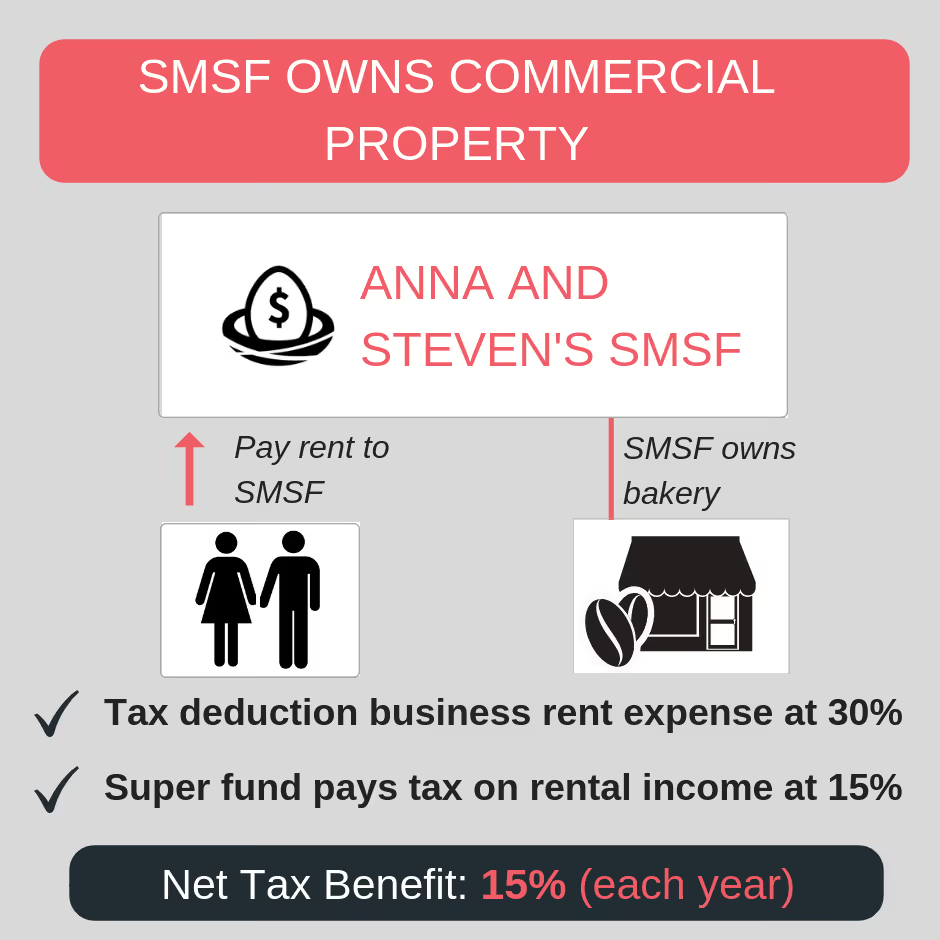

A quick example

Steven and Anna’s bakery business operates through a company or trust, with a tax rate of 30% or more. To optimise their tax strategy, they purchase the bakery premises through their SMSF:

- Steven and Anna now pay rent to their SMSF, which owns the bakery property.

- They get a tax deduction for the rent expense at 30% (or more).

- The SMSF only pays 15% tax on the rental income it receives.

- The net tax benefit to Steven and Anna equals 15% of the rental income each year.

Once Steven and Anna reach age 65 and start withdrawing money from their SMSF:

- Their SMSF pays no tax on rental income, meaning they keep the full 30% (or more) on the rent paid each year.

- If the SMSF sells the property before the pension phase, it pays only 10% capital gains tax (CGT) compared to up to 22.5% outside of super.

- If the SMSF is in the pension phase, the CGT rate is 0% — offering a huge advantage in building wealth inside super.

Comparing tax minimisation strategies: which one is right for you?

There are multiple ways to reduce your income tax through superannuation, but not all strategies are equally beneficial depending on your situation. Here’s a side-by-side comparison of key super tax strategies and their advantages and disadvantages.

[table]

[thead]

[tr][th]Strategy[/th][th]How it works[/th][th]Key benefits[/th][th]Potential downsides[/th][/tr]

[/thead]

[tbody]

[tr][td]Concessional super contributions[/td][td]You make a personal contribution and claim a tax deduction (up to the concessional contributions cap).[/td][td]Lowers income tax liability, builds retirement savings, taxed at just 15%.[/td][td]Excess contributions may attract extra tax, contributions are preserved until retirement.[/td][/tr]

[tr][td]Salary sacrifice[/td][td]You direct part of your salary to super before tax is deducted.[/td][td]Reduces taxable income, contributions taxed at just 15%.[/td][td]Must stay within superannuation guarantee and concessional caps, funds are locked until retirement.[/td][/tr]

[tr][td]Super co-contribution[/td][td]If you make an after-tax contribution, the government may match a portion of it.[/td][td]Free boost to your super account, tax-free earnings.[/td][td]Only available to those under the income threshold.[/td][/tr]

[tr][td]Buying property in SMSF[/td][td]Use your super to invest in commercial property and lease it back to your business.[/td][td]Business rent is tax-deductible, property growth is taxed at lower CGT rates.[/td][td]Requires high SMSF balance, complex compliance rules.[/td][/tr]

[tr][td]Prepaying deductible expenses[/td][td]You pay for eligible expenses (e.g., insurance, interest) before June 30 to bring forward deductions.[/td][td]Immediate tax relief, reduces amount of tax you pay this year.[/td][td]Requires available cash flow, doesn’t reduce long-term tax obligations.[/td][/tr]

[/tbody]

[/table]

Understanding the strengths and limitations of each strategy ensures you make contributions that align with your financial goals. If you want to claim the best deductions and optimise your tax planning, our SMSF advisors can help tailor a solution that works for you.

[free_strategy_session]

Download our tax minimisation guide

This guide could help reduce your tax bill and improve your financial position

Inside you’ll find practical strategies and essential information to help you minimise tax legally and effectively—whether you're an individual, investor or business owner.

- Understanding legitimate tax deductions and offsets

- How to structure your business to reduce tax

- The benefits of super contributions and trust structures

- Tax-effective investment strategies

- Common tax traps and how to avoid them

[/free_strategy_session]

Give us a call, and let's figure out how we can claim a deduction

Superannuation is one of the most powerful tax planning tools available to business owners like you. Whether you’re looking to reduce your taxable income, protect your assets, or build long-term wealth in a low tax environment, using super strategically can help you pay less tax today while securing your financial future.

We strongly recommend doing a bit of your own research — the ATO website is a natural place to start researching personal super contributions.

Get in touch with our veteran SMSF accountants today and let’s chat about how you’d be able to claim a tax deduction for personal super contributions to reduce your tax bill and grow your wealth the smart way.