.avif)

Personal services income sounds like a straightforward concept, but in practice, it can be quite tricky to navigate.

In this article, we discuss what personal services income is, when it applies to your business, and what this means for you if it does.

Liston Newton Advisory is here to take the mystery out of personal services income. Get in touch with us today to book in a 90-minute strategy call, and see how we can help make your income tax as hassle-free as possible.

Understanding personal services income

Personal services income (PSI) has quite a broad definition. In short, it’s when at least 50% of your income is derived from your skills or efforts as an individual, as opposed to a wage or salary. As such, this mostly applies to contractors or consultants.

If 50% or less of your income for an individual invoice or contract was for your skills or labour, then none of this income is classified as PSI.

For example, you won’t earn PSI if your income is derived from:

- A salary or wage paid by your employer

- Renting an asset to produce income, such as machinery or vehicles

- Supply or selling products, even if you’re the one that made them

- Licencing your intellectual property, such as with a patent

Understanding when PSI applies to your business

The ATO created rules around PSI to ensure that individuals earning income in this manner can't abuse the tax system. This includes things like diverting your income through a business structure to different beneficiaries, accessing company tax rates, or having another business entity take on your losses.

Here are the steps to take to determine whether or not PSI applies to your business.

Step 1. Does PSI apply to your business?

Look at the income you’ve received from each individual invoice or contract.

- Has more than 50% of this income been generated from your personal skills, labour, or expertise? If so, the total amount of income for that invoice or contract is classified as PSI.

- If none of your invoices or contracts are classified as PSI, then the PSI rules don’t apply to your business.

If one or more contracts or invoices is classified as PSI, then you may be considered a personal service business (PSB), and you will need to pass one of the following tests. Move on to Step 2.

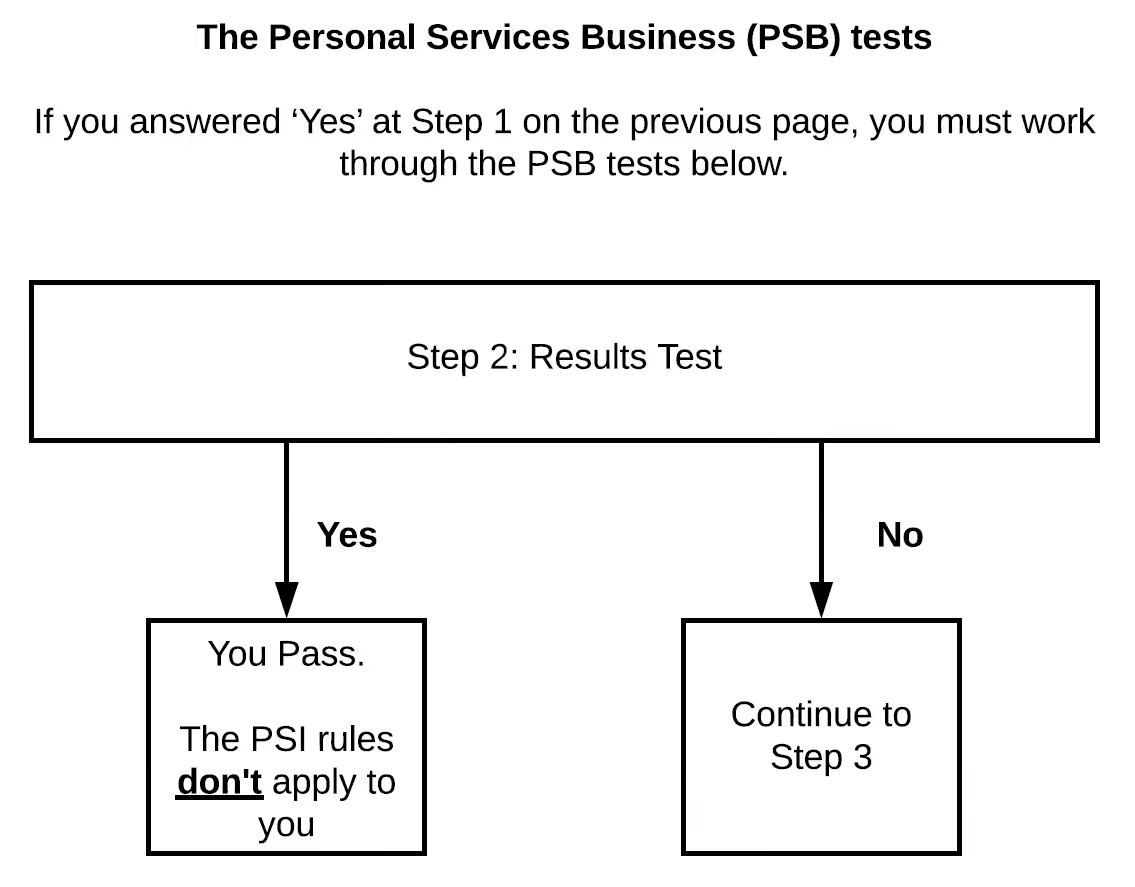

Step 2. Results Test

Based on the PSI generated, ask the following questions:

- Was my business paid to produce a specific result?

- Was I required to provide the tools or equipment to produce this result?

- Was I required to fix any mistakes at my own expense?

If you answered ‘yes’ to all three of these questions, for 75% or more of your income, then you classify as a PSB and the PSI rules don’t apply.

If you answered ‘no’ to one or more of these questions, then the PSI rules may apply to your business, and you should move on to Step 3.

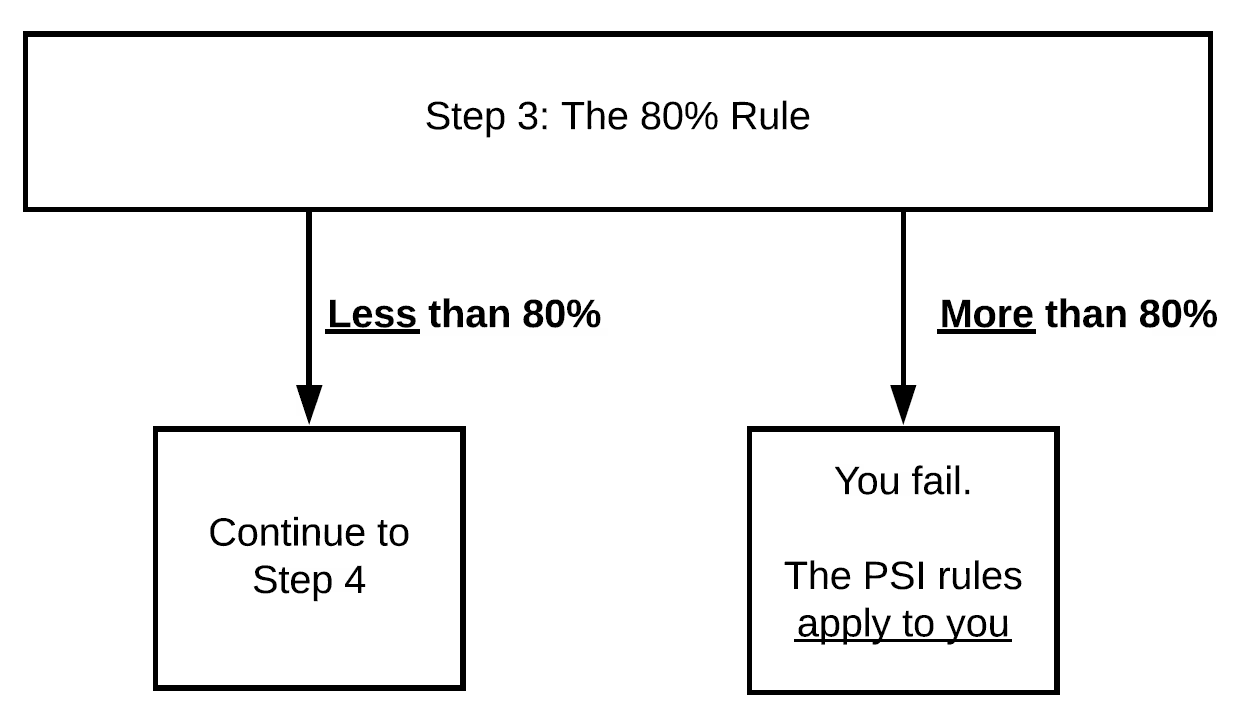

Step 3. The 80% Rule

If you answered 'no' to one or more of the questions above, then you need to work out how much of your client base generates PSI.

If 80% or more of your PSI comes from one specific client, or group of clients, then the PSI rules do apply to your business. This is known as the 80% rule.

If your income is diversified across a number of clients, then you should move on to Step 4.

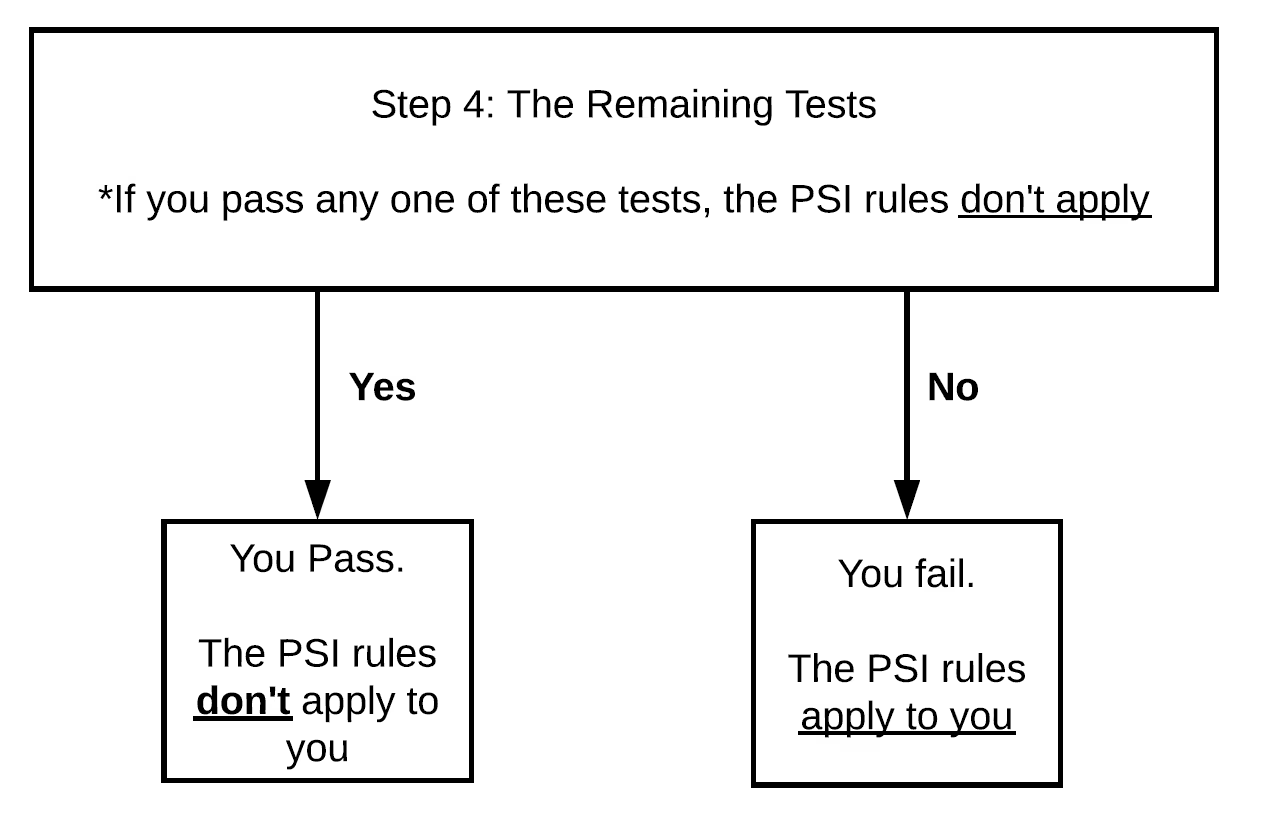

Step 4. The remaining tests

If your PSI income is diversified across a number of clients, it becomes a little more muddled. You can perform any of the following tests to determine conclusively whether the PSI rules apply or not.

If you pass one of these tests, then PSI rules do not apply to your business:

- Unrelated clients test. If you complete work for two or more unrelated clients, and you’re actively seeking out new work — whether it’s through your website, referrals, tenders, etc — then you pass the test.

- Employment test. If you hire a contractor or employee to complete 20% or more of your billable work — excluding bookkeeping or administrative tasks — then you pass the test.

- Business premises test. If you run your business operations from separate premises to your other work, then you pass the test.

If you do not pass at least one of these tests you can apply to the ATO for a PSB determination.

The ATO has a useful flow chart that breaks this PSI determination down into easy-to-understand chunks. You can check it out here.

What to do if PSI applies to your business

If the PSI rules apply to your business, this will change how you report your income and the types of deductions you can make.

Changes to your tax rate

If PSI rules apply to your business then, regardless of your business structure, you’re required to pay tax on your income as an individual. It makes how you structure your business less tax-effective, and it means that you can’t distribute profits to beneficiaries in order to minimise tax.

Income tax deductions

In general, any expenses you incur in running your business and in completing your contracts can be claimed against tax. For example, you can claim the following things as deductions:

- Accounting and bank fees

- Insurance expenses

- Any costs for marketing or advertising

- Salary or wage payments to employees

- Depreciation on assets that generate income

Conversely, any expenses incurred that don't directly help you complete a contract cannot be claimed as a tax deduction. This includes items like rent, mortgage repayments, or payments or superannuation to employees for non-operational business work.

Income that’s not defined as PSI

If you generate income that’s not classified as PSI, simply treat this as your regular income. This means that you can take full advantage of the benefits denied under PSI rules.

When it comes to tax time, you’ll still need to declare any PSI amounts where necessary.

The difference between contractors and employees

As mentioned above, employees that derive a wage or salary aren’t classified as earning PSI. But in some cases, the differences between employees and contractors can blur.

Your staff can be considered employees if:

- You direct where, when, and how they work

- They’re paid regularly for the hours they work, not the specific outcome

- They don’t make a profit or loss from the job they’re completing

- You provide their equipment and tools

- They are considered as part of your business

Your staff can be considered contractors if they:

- Are paid on a contractual basis to deliver a certain result or outcome

- Provide their own tools or equipment

- Are free to work how, where, and when they want, as long as they get the job done

- Are free to work with other businesses outside of yours, and even turn your contract down or negotiate the terms

- Make a profit or loss from the work they’re completing for you

The final word

As a business or a contractor, it’s important to determine early whether your income falls under PSI rules or not. This can influence how you structure your business for tax purposes, and what you’re allowed to claim during the financial year.