Our Locations

COVID-19: Liston Newton is here to support your business continuity planning. Get started

Our new head office is now in South Melbourne - See address

Call us today

Financial debt advisor

Restore your peace of mind with direct, effective debt management advice

Get a free 60-minute financial strategy session.

Book now

Why choose us?

Holistic approach

We take a comprehensive view of your finances, not just your debts, to create strategies that boost your overall financial well-being.

Proven expertise

With decades of experience, we offer tailored advice and support, guiding you towards financial freedom.

Long-term partnership

We’re dedicated to your ongoing success, adjusting strategies as needed to keep you on track toward your financial goals.

Simplified process

Our straightforward approach makes debt management clear and manageable, giving you confidence every step of the way.

Regain financial control with personalised debt advice and strategies

Managing debt isn’t just about paying off balances — it’s about finding a strategic path to financial stability. Our advice goes beyond the basics, focusing on reducing your debt in a way that strengthens your overall financial position and gives you a solid foundation for the future.

Whether it’s business tax debt, personal loans, or high-interest credit cards, we tailor our strategies to address your unique challenges. By prioritising your debts, negotiating better terms, and finding practical solutions, we aim to alleviate the stress of debt and set you on a path to lasting financial well-being.

.png)

Our personalised approach to managing your debt

Our process starts with a detailed look at your financial picture, including your income, expenses, and current debts. We identify the root causes of your financial challenges and work with you to develop a tailored strategy that fits your needs.

We empower you with the tools and guidance to take control of your financial situation. From offering advice on prioritising repayments to providing support while negotiating terms with creditors, we’re here to help you navigate the complexities of debt management. Regular reviews and adjustments ensure your strategy remains effective as your circumstances change, all while prioritising compliance and risk management.

Key services we offer include:

- Comprehensive financial assessments and debt analysis

- Customised strategies that align with your financial goals

- Guidance on negotiating repayment plans and managing creditors

- Regular reviews and adjustments to your debt management plan

- Risk management and compliance with financial regulations

You’ll be supported by our expert team at every step of your journey

Talk to us today%2520(1).png)

Personalised debt advice for complex individual situations

Dealing with personal debt can be stressful, especially when it involves high-interest credit cards or uncertain repayments. We offer practical, tailored advice to help you manage your debts in a way that fits your lifestyle and financial goals, turning uncertainty into a manageable plan.

Our expertise includes:

- Personalised guidance for managing different types of personal debt effectively

- Targeted strategies for paying off credit card debt without feeling overwhelmed

- Support with doubtful debts, offering clear steps to mitigate financial risks

%20160x160.avif)

Business-focused debt management solutions

For businesses, effective debt management is key to maintaining financial health and operational stability. We specialise in advising on business debts, including managing tax obligations and navigating complex financial challenges, so you can focus on running your business with confidence.

Our business services include:

- Tailored business debt strategies that align with your company’s unique circumstances

- Expert advice on business tax debts, helping you stay compliant and avoid costly mistakes

- Ongoing debt management advice to support your business’s financial growth and resilience

Effective strategies for debt recovery and consolidation

Simplifying debt repayments through recovery and consolidation can be a game-changer, helping you regain control over your finances. Our approach offers clear, actionable steps to consolidate debts or recover outstanding amounts, making your financial journey smoother and more manageable.

Our services include:

- Debt recovery advice to help reclaim unpaid debts swiftly and effectively

- Guidance on debt collection, improving cash flow with professional support

- Debt consolidation strategies that simplify multiple debts into a single, manageable payment

We’ve proven our expertise

Our extensive network of partnerships with leading financial institutions ensures that you receive reliable, up-to-date advice. We’ve built our credibility on years of successful outcomes and a commitment to your financial well-being.

“I look forward to working together for many years to come”

Kieran Liston and the Liston Newton team have been assisting me with my accounting matters since 1976. For the past 47 years, Kieran and the Liston Newton team have provided reliable accounting assistance, which has allowed me to focus on my business in primary production.

Their exceptional service has consistently exceeded my expectations and made me feel that they truly care about my financial well-being.

Liston Newton has given me really helpful guidance over the years for both my business and my personal finances. When you have an accounting team that you trust to give the right advice, it gives you the confidence to focus on growing your business and doing the things you love.

Liston Newton helped us move our accounting over to Xero. Their Accountant managed the set up and training so we felt comfortable with the software. We now have all our processes streamlined which gives us improved visibility of our business performance. This has allowed us to open 2 more stores without a significant increase in administration effort.

Navigate your financial future with our downloadable guides

Gain the tools and confidence to take control of your finances with our expert-crafted guides. Whether you're planning for retirement or building wealth for the long term, our free downloads are packed with practical knowledge to support your journey forward.

Our guides include:

- Simple, effective strategies for growing your wealth

- Clear advice on how to plan and prepare for retirement

- Guidance to help you feel more confident in your financial decisions

Smart wealth guide

Download Guide

Your guide to a successful retirement

Download Guide

Navigate your financial future with our downloadable guides

Gain the tools and confidence to take control of your finances with our expert-crafted guides. Whether you're planning for retirement or building wealth for the long term, our free downloads are packed with practical knowledge to support your journey forward.

Virtual CFO guide

Download Guide

Smart wealth guide

Download GuideYour guide to a successful retirement

Download GuideYour guide to tax-effective business sales

Download Guide

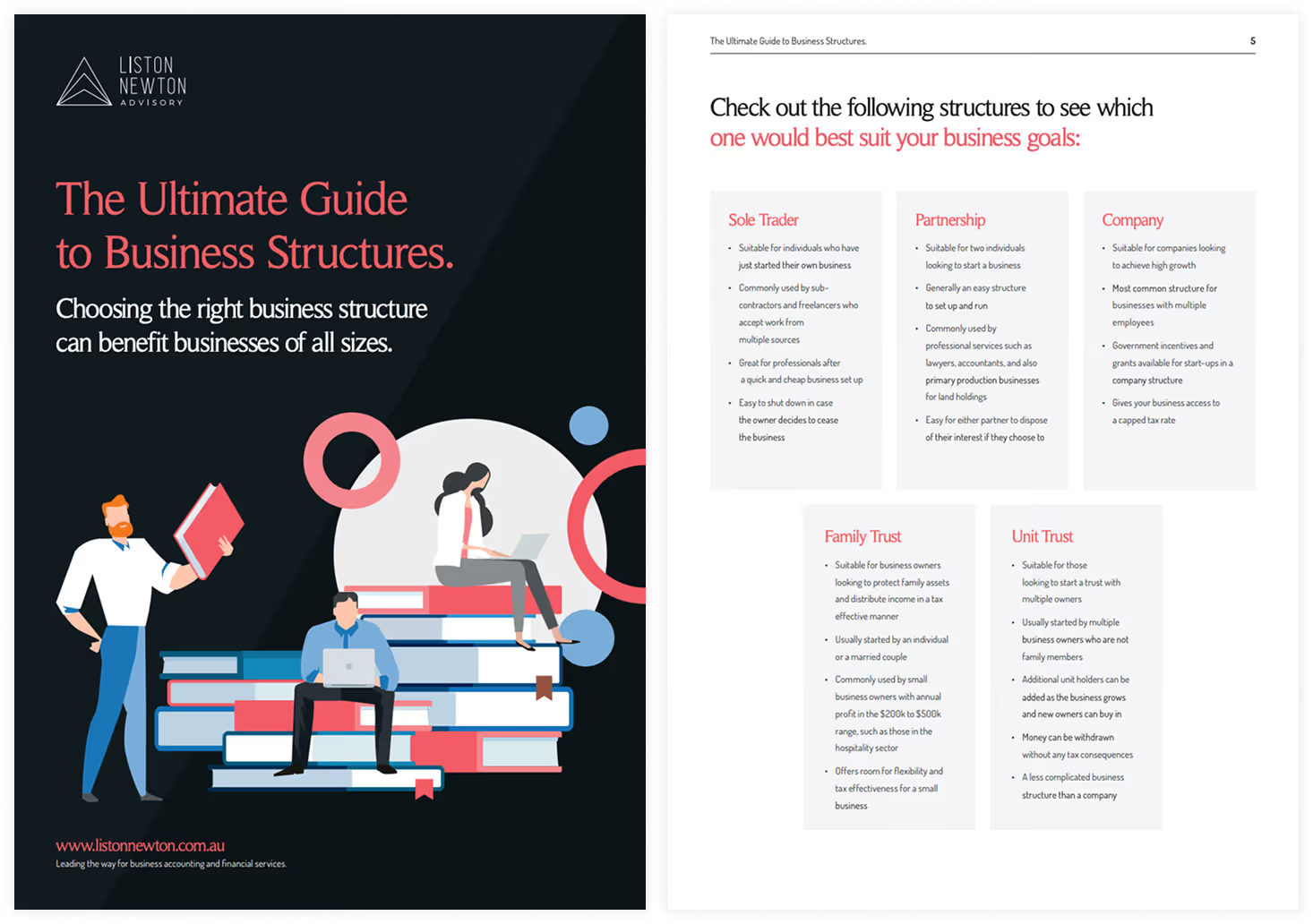

Your guide to business structures

Download Guide

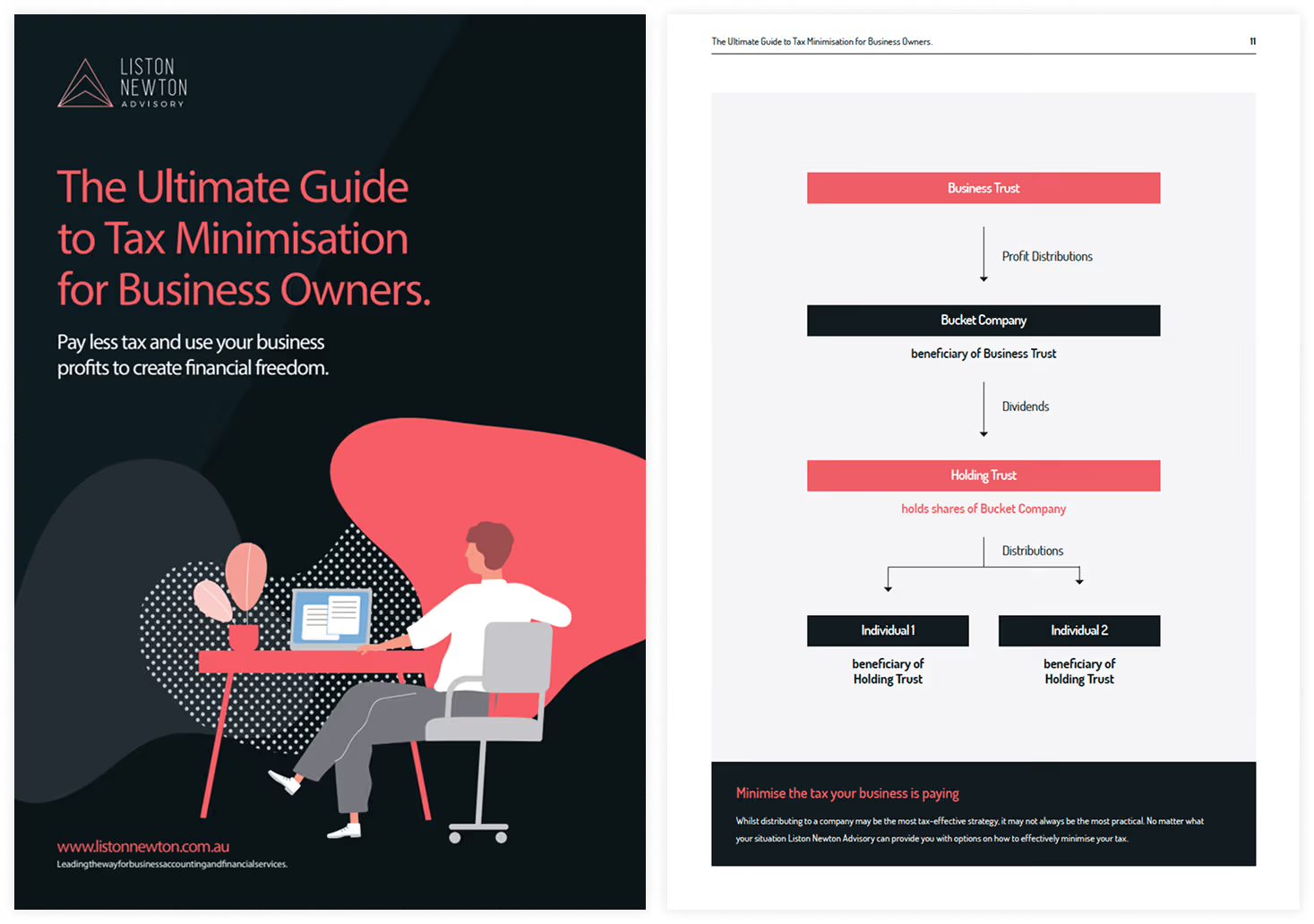

Your guide to tax minimisation

Download Guide

Navigate your financial future with our downloadable guides

At Liston Newton, we pride ourselves on offering tailored investment strategy solutions that help our clients achieve financial freedom. With decades of experience in financial advisory and a deep understanding of the industry, we’re committed to supporting you every step of the way.

We combine our comprehensive industry knowledge with a client-first approach to address immediate debt concerns and support your long-term financial growth. Trust our expertise to confidently guide you through the complexities of debt management.

The benefits of partnering with us

- Personalised strategies tailored to your unique financial needs

- Over 40 years of experience in financial advisory and debt management

- Award-winning services recognised across the financial industry

- Ongoing support and strategic adjustments to adapt to changing conditions

- Access to leading financial tools and insights that empower decision-making

.avif)

A clear path to financial freedom

Getting back on track is easier with a clear plan. Our straightforward process provides the guidance and support you need with transparent steps and consistent communication.

Initial consultation:

We take a comprehensive look at your financial goals and assess your current situation.

Strategy development:

We create a personalised plan with actionable steps to address your financial challenges.

Implementation and review:

We guide you through implementing the plan and regularly review it to keep it on track.

Case studies

Close

Accounting

Chris & Leanne Roberts

After engaging Liston Newton's services, Chris & Leanne Roberts were able to purchase the B&B of their dreams by utilising their savings in the most tax-effective way.

Take a lookWe work with clients across Australia

While our offices are located in Victoria, New South Wales and Queensland, we gladly work with clients across Australia via virtual consultations. Whether you prefer in-person or online support, our dedicated team is here to guide you through your financial challenges.

South Melbourne

Level 3/67 Palmerston Crescent, South Melbourne, VIC 3205

Melbourne

17/31 Queen St, Melbourne VIC 3000

Malvern

Suite 175/45 Glenferrie Road, Malvern, VIC 3144

Donald

36 Woods Street, Donald VIC 3480

Gold Coast

Level 10, 36 Marine Parade Commercial Tower, 36 Marine Parade, Southport QLD 4215

Sydney

Level 22-23, Salesforce Tower, 180 George Street, Sydney, NSW 2000

Essential reading

Frequently asked questions

How does debt management work?

Debt management involves creating a plan that strategically reduces your debts, setting you on a path to financial stability. We start by reviewing your financial situation, including income, expenses, and existing debts. From there, we develop a personalised strategy to prioritise your debts, negotiate with creditors, and implement a payment plan that aligns with your goals.

How does debt consolidation work?

Debt consolidation can be a smart way to reduce your overall interest rate and pay down debt sooner. Debt consolidation works by taking out a new loan at a lower rate to pay off a number of other loans you may have at higher rates.

For example, let's say you have a home valued at $1m and a loan against the home of $500k. You also have 2 credit cards with a total of $20,000 owing on the cards. The credit cards are charging 15% per annum. You also have a car loan of $30,000 at a rate of 6%.

It may be possible to draw down a further $50,000 against your home to payoff (consolidate) the credit cards and car loan and instead of paying 15% or 6% on the debt, you reduce it down to a home loan rate under 3%.

How can personal debt advice help with paying off credit card debt?

High-interest credit card debt can quickly become overwhelming. Our personal debt advice provides strategies to tackle credit card debt effectively, including budgeting tips, balance transfers, and debt repayment plans. We help you create a manageable path to pay off your credit cards and improve your financial health.

Should I pay off my home loan or contribute to super?

Like many questions relating to financial advice, the short answer is: it depends.

Good advice always depends on your individual circumstances. However, it’s possible to educate yourself on the outcomes of each choice.

Conventional wisdom has usually said you should pay off your home as quickly as possible and then turn your attention to building a nest egg.

The main aspect to consider is the return you can get on investments in your super vs. the interest rate on your home loan. With home loan rates at record lows in recent years, it can often make more sense to get a 7%-8% return from money in your super, rather than repay your home loan which is effectively the same as earning 2 to 3% per year.

If you do decide to invest in super rather than pay your home loan, it all comes down to planning. You may choose to prioritise investing in super for a period of 10 years. At the end of those ten years, you may then access your super and use some of this money to pay down the loan. If you plan correctly, you may be able to achieve both goals of building your super and repaying your debt — it's just the timing is different.

When should I consider paying off debt?

The right time to pay down debt will always depend on your personal situation.

There are three key factors to consider when assessing the merits of paying down debt: first, your comfort level with debt. Second, the interest rates on your debt. And third, the tax effectiveness of your debt.

Your comfort with debt is the most important factor. Regardless of how cheap the interest rates on debt may be, if your debt levels are keeping you up at night, then you should prioritise working to pay off debt.

The interest rates on your debt will be the second key factor in when or if you pay down debt. In recent years, the cost of debt has become cheaper. Therefore, it can make sense to invest your excess cash flow rather than prioritise paying down your debt. For example, a home loan debt can be as low as 2%, while the return on investing in shares can be as high as 8% per annum. Paying down your home loan is the same as getting a 2% return on your money.

The other key consideration is the tax effectiveness of your debt. It can make sense to ensure you pay down non-tax-deductible debt over tax-deductible debt. This can mean paying down the loan on your primary place of residence rather than your investment property.

Ready to take control of your financial future?

Book a consultation with our financial debt advisors today and discover how personalised advice can help you achieve your financial goals.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Powered by EngineRoom

Free financial strategy session*

Get a free 60-minute video consultation. See how it works.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.