.avif)

If you’re a business owner who’s ever thought about making loans within your company, understanding Division 7A is essential. Get it right, and you can minimise your tax liability and keep your business running smoothly. But get it wrong, and you could face heavy penalties and end up paying significantly more tax than necessary.

At Liston Newton Advisory, we specialise in business tax planning and compliance, helping business owners just like you structure their finances for maximum tax efficiency. With decades of experience navigating Division 7A and related taxation laws in Australia, our team knows exactly how to protect you from unwanted tax bills and compliance issues.

In this guide, we’ll give you a clear and frank overview of everything you need to know about Division 7A loans, why they matter to your business, and how you can stay on the right side of the ATO. Of course, you can always contact us to book a consultation with our business accountants for tailored advice.

[general_awards][/general_awards]

What is Division 7A in Australia?

Division 7A is a set of tax rules established by the ATO to prevent private companies from making tax-free payments or loans to shareholders or their associates. Its primary purpose is to ensure that profits distributed from a company are taxed appropriately, rather than disguised as loans to avoid tax.

If you’re a business owner distributing profits from a trust to a bucket company to cap your tax rate at 25% or 30%, you might be familiar with the issue of getting those funds into your personal account. This often involves loans made from your company to you as an individual.

[feature_link]Looking to minimise your tax with a bucket company? Read our guide to ensure you’re using them effectively and staying compliant.[/feature_link]

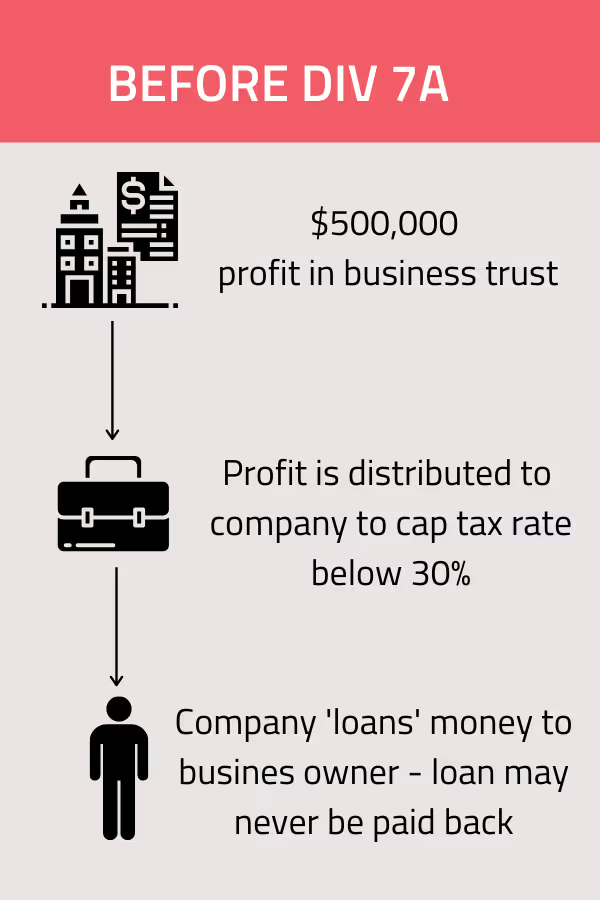

Before Division 7A was enforced, companies would lend money to shareholders or their associates, either with no intention of repayment or with very lenient repayment terms. The ATO’s view is that these types of transactions are ‘disguised contributions’ — effectively a form of tax avoidance.

To combat this, the government introduced Division 7A to ensure that such loans are structured properly, with formal agreements and set repayment terms, so they’re treated as genuine loans rather than untaxed income.

[tip_box]

Download our tax minimisation guide

This guide could help reduce your tax bill and improve your financial position

Inside you’ll find practical strategies and essential information to help you minimise tax legally and effectively—whether you're an individual, investor or business owner.

- Understanding legitimate tax deductions and offsets

- How to structure your business to reduce tax

- The benefits of super contributions and trust structures

- Tax-effective investment strategies

- Common tax traps and how to avoid them

[/tip_box]

What is a Division 7A loan?

A Division 7A loan is a formal loan made by a private company to a shareholder or their associate, structured to comply with Division 7A rules. If properly structured, it allows you to access company funds without the distribution being classified as assessable income.

For a loan to be Division 7A-compliant, it must:

- Be made under a written agreement.

- Include a set interest rate and repayment terms.

- Be repaid within specific timeframes (unsecured loans have a maximum term of 7 years; secured loans have a maximum term of 25 years if backed by sufficient security).

Div 7A also applies to:

- Forgiven loans: When a company writes off a loan, making it non-repayable.

- Payments on behalf of a shareholder: Such as expenses paid directly by the company.

- Any financial transaction that could be considered equivalent to a loan.

Properly structuring your Division 7A loan ensures you avoid additional tax penalties and remain compliant with the ATO’s guidelines.

What Are Unpaid Present Entitlements (UPEs)?

A UPE arises when a trust declares that it will distribute income to a private company beneficiary, but the funds are not physically paid to the company. Instead, the money is retained within the trust for various reasons, such as reinvestment or cash flow management.

For example, if your family trust distributes $200,000 to a bucket company to take advantage of the company's lower tax rate, but the money remains in the trust rather than being paid to the company, that $200,000 becomes a UPE.

How UPEs Relate to Division 7A

The ATO sees UPEs as a potential way to avoid Division 7A rules, especially when the funds are being retained by the trust but meant for the company. If the UPE is treated as a loan from the company to the trust, Division 7A can apply.

To avoid this, the ATO requires that UPEs be either:

- Paid to the company within a reasonable timeframe; or

- Converted into a compliant Division 7A loan, with a formal loan agreement, interest charges, and structured repayment terms.

If a UPE is not managed correctly, it may be deemed a Division 7A loan. This can result in the unpaid amount being treated as a deemed dividend, which is taxed as assessable income at the shareholder’s individual tax rate.

Why It Matters

Mismanaging UPEs can lead to significant tax penalties. If your business uses trusts and bucket companies to distribute income, it’s essential to ensure all UPEs are either:

- Paid out, or

- Properly structured under Division 7A guidelines.

Why you need a Division 7A-compliant loan

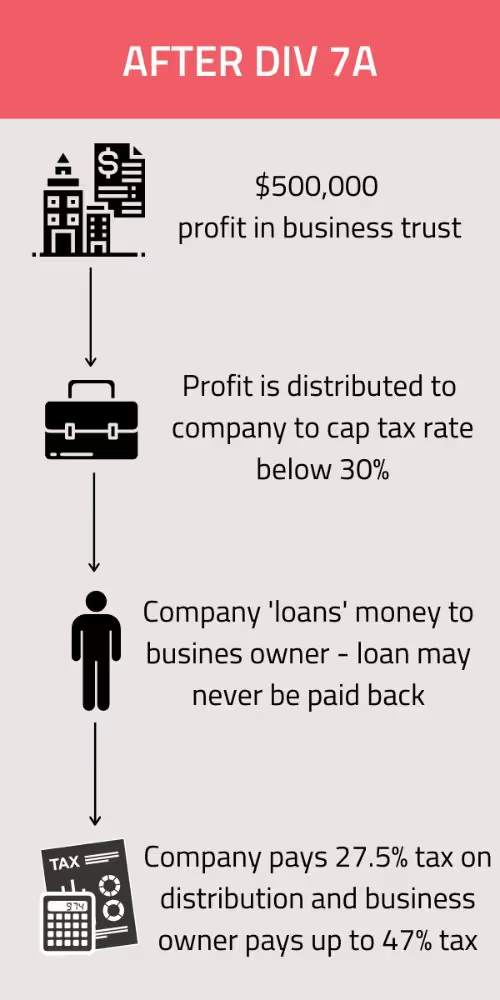

When you make a distribution that doesn’t meet Division 7A requirements, the ATO considers it non-compliant. The penalty? You’re hit with a higher tax bill. Instead of being taxed at the company’s rate of 25% or 30%, the distribution is taxed at your personal rate — potentially up to 47%. And here’s the kicker: you don’t get credit for the tax already paid by the company.

This means the effective tax rate on your distribution could skyrocket to as much as 61.5%. It’s the ATO’s way of ensuring that companies and shareholders don’t avoid paying the proper amount of tax by disguising dividends as loans.

For example, if you distribute income from a trust to a bucket company and then try to lend that cash back to yourself without following Division 7A rules, you’re in for a rude shock come tax time.

A compliant Division 7A loan is the only way to legally access your company’s funds without triggering a massive tax bill.

[free_strategy_session]

Book your free 90-minute Division 7A strategy session

Get a personalised plan to ensure your Division 7A loan arrangements are compliant, tax-effective and aligned with your business goals.

- Understand how Division 7A affects your company loans and repayments

- Get tailored advice on managing existing Division 7A loan agreements

- Learn how to structure future loans to avoid unexpected tax consequences

Book your free strategy session today.

[/free_strategy_session]

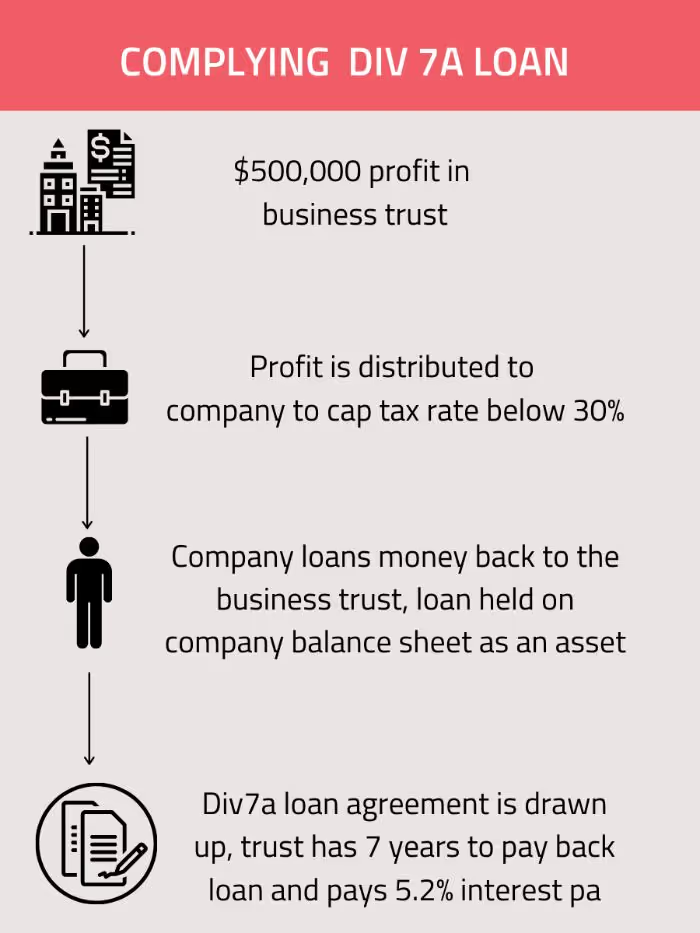

How a Division 7A-compliant loan works

A compliant Division 7A loan ensures that money lent from your company to yourself (or another shareholder) is treated as a legitimate loan — not a disguised dividend.

How is a Division 7A loan paid?

A Division 7A loan is paid by making regular repayments of principal and interest, which are put on a complying Division 7A loan agreement. Repayments must be made each income year by the lodgement date — the due date for the company's tax return.

If repayments aren’t made by this deadline, the unpaid amount becomes payable as a dividend and may lose the benefit of being treated as a loan. In certain circumstances, you can put the outstanding amount on a new complying Division 7A loan agreement to avoid having to pay tax on the loan amount.

The Two Types of Complying Division 7A Loans

When setting up a Division 7A-compliant loan, it’s essential to choose the right type of loan agreement. There are two primary options: unsecured loans and secured loans.

Unsecured Loans:

An unsecured loan is the simpler of the two options, but it comes with stricter terms. The maximum term allowed for an unsecured loan is seven years. Because of this shorter term, your repayments will generally be higher to ensure the principal is paid off within the required timeframe. This option is often chosen when a quick repayment plan is feasible.

Secured Loans:

A secured loan provides a much longer repayment window, with a maximum term of up to 25 years. This extended term is only available if the loan is properly secured by an asset, such as property or other valuable collateral. The advantage of a secured loan is that it offers more favourable repayment terms and lower annual payments. However, it requires careful documentation and compliance to ensure the security meets the ATO’s standards.

Key Requirements for Compliance:

- A formal written agreement outlining the loan terms.

- Payment of minimum yearly repayments including both principal and interest.

- Ensuring the interest rate matches or exceeds the ATO’s benchmark interest rate.

- Adhering to the repayment schedule until the loan is fully repaid.

A Division 7A loan allows you to access company funds temporarily while remaining compliant with tax laws. You’re not avoiding tax — you’re simply deferring the payment to a later date.

[feature_link]Are you eligible for CGT concessions for small businesses? Learn how to save on tax and make the most of your entitlements.[/feature_link]

Example of a Division 7A-compliant loan

David owns a consulting business that operates through a family trust. This financial year, his business made a profit of $500,000.

David has already paid himself $200,000 in salary, taxed at the highest rate of 47%. He doesn’t want to distribute the full $500,000 to himself because of the high tax rate. Instead, he distributes the money to his bucket company through a distribution minute in the family trust.

But his business has poor cash flow due to slow-paying clients. To access the money, he sets up a Division 7A-compliant loan, effectively lending a portion of the $500,000 from the bucket company to his trust. The loan terms are:

- Term: 7 years.

- Interest rate: Changes every year.

The trust treats the interest payments as tax-deductible expenses, while the company reports the interest as income. As long as David makes his required repayments on time and completes the loan within the agreed period, he remains fully compliant with Division 7A rules.

The final word

Division 7A is a highly complex area, and can trip up unsuspecting business owners if they aren’t prepared for it. Being across your Division 7A requirements is crucial in making a tax-effective loan within your company, and ensuring you remain tax compliant.

So, whenever you're considering making a loan from your business to a shareholder, it's important to carefully consider the following:

- You set defined loan repayment terms

- You repay the minimum repayment amount required on time

- There are no timing issues with the loan agreement

- All your distributable surplus is calculated correctly.

Making an error on any of these points means your Division 7A loan is no longer compliant, and the loan amount automatically defaults to being fully assessable for tax purposes.