Our Locations

COVID-19: Liston Newton is here to support your business continuity planning. Get started

Our new head office is now in South Melbourne - See address

Call us today

Salary sacrifice financial advice

Maximise your savings with strategic salary sacrificing

Get a free 60-minute financial strategy session.

Book now

Why choose us?

Holistic approach

We take a comprehensive view of your finances, not just your salary sacrifice arrangement, to create strategies that boost your overall financial well-being.

Proven expertise

With decades of experience, we offer tailored advice and support, guiding you towards financial freedom while maximising your tax benefits.

Long-term partnership

We’re dedicated to your ongoing success, adjusting strategies as needed to keep you on track toward your financial goals and ensuring your salary packaging remains effective.

Simplified process

Our straightforward approach makes managing your salary package clear and manageable, giving you confidence every step of the way.

How salary sacrifice financial advice supports your goals

Effective salary sacrificing isn’t just about reducing taxable income; it’s about creating a strategy that aligns with your financial goals, whether it's saving for retirement or optimising your tax benefits. We provide insights into how salary sacrifice contributions can work within your broader financial plan, ensuring you take full advantage of the concessional contributions cap and avoid unnecessary tax implications.

By tailoring your salary sacrifice arrangement, we help you leverage opportunities such as exempt benefits and reduce your marginal tax rate. Our strategies are designed to maximise your savings, minimise your tax liability, and support your financial growth, giving you peace of mind as you work towards your goals.

.png)

The process of salary sacrifice financial advice

Our process begins with a detailed assessment of your financial situation, including your current salary package, income, expenses, and future goals. We develop a customised plan that incorporates salary sacrificing, employer contributions, and potential fringe benefits to optimise your financial strategy.

Throughout the process, we ensure compliance with all relevant regulations, including those related to paying fringe benefits tax and understanding what your employer pays. We provide ongoing reviews and adjustments to ensure your salary sacrifice arrangement remains effective, adapting to changes in your financial situation or tax laws.

Key assessments and services include:

- Comprehensive financial evaluations

- Customised salary sacrifice strategies

- Coordination with employers on contributions and salary packaging

- Regular reviews and adjustments

- Risk management and compliance with tax regulations

Simplify your sacrifices and maximise your benefits

Talk to us today%2520(1).png)

Tailored salary packaging solutions for individuals and business owners

We offer comprehensive salary packaging solutions designed to meet the unique needs of both individuals and business owners. Whether you’re an employee looking to optimise your salary sacrificing strategy or a business owner seeking efficient ways to offer fringe benefits, our personalised approach ensures that you receive expert guidance tailored to your specific circumstances.

Our services include:

- Customised advice on salary packaging for both personal and business contexts.

- Strategies to maximise your tax benefits and reduce tax liabilities, tailored to your goals.

- Guidance on managing salary sacrifice contributions to stay within the concessional contributions cap, optimising your financial outcomes.

%20160x160.avif)

Why trust our expertise?

With strong partnerships with leading financial institutions, we ensure you receive reliable and up-to-date advice. Our credibility is built on years of successful client outcomes and a commitment to your financial well-being.

“I look forward to working together for many years to come.”

Kieran Liston and the Liston Newton team have been assisting me with my accounting matters since 1976. For the past 47 years, Kieran and the Liston Newton team have provided reliable accounting assistance, which has allowed me to focus on my business in primary production.

Their exceptional service has consistently exceeded my expectations and made me feel that they truly care about my financial well-being.

Liston Newton has given me really helpful guidance over the years for both my business and my personal finances. When you have an accounting team that you trust to give the right advice, it gives you the confidence to focus on growing your business and doing the things you love.

Liston Newton helped us move our accounting over to Xero. Their Accountant managed the set up and training so we felt comfortable with the software. We now have all our processes streamlined which gives us improved visibility of our business performance. This has allowed us to open 2 more stores without a significant increase in administration effort.

Find out more with our downloadable financial guides

Equip yourself with the knowledge to take control of your financial future. Our comprehensive guides explore topics such as growing personal wealth and preparing for a secure retirement, helping you make confident decisions every step of the way.

Our guides include:

- Strategies to maximise your long-term wealth

- Practical steps to plan a fulfilling retirement

- Tips for setting and achieving financial goals

Smart wealth guide

Download Guide

Your guide to a successful retirement

Download Guide

Find out more with our downloadable financial guides

Equip yourself with the knowledge to take control of your financial future. Our comprehensive guides explore topics such as growing personal wealth and preparing for a secure retirement, helping you make confident decisions every step of the way.

Virtual CFO guide

Download Guide

Smart wealth guide

Download GuideYour guide to a successful retirement

Download GuideYour guide to tax-effective business sales

Download Guide

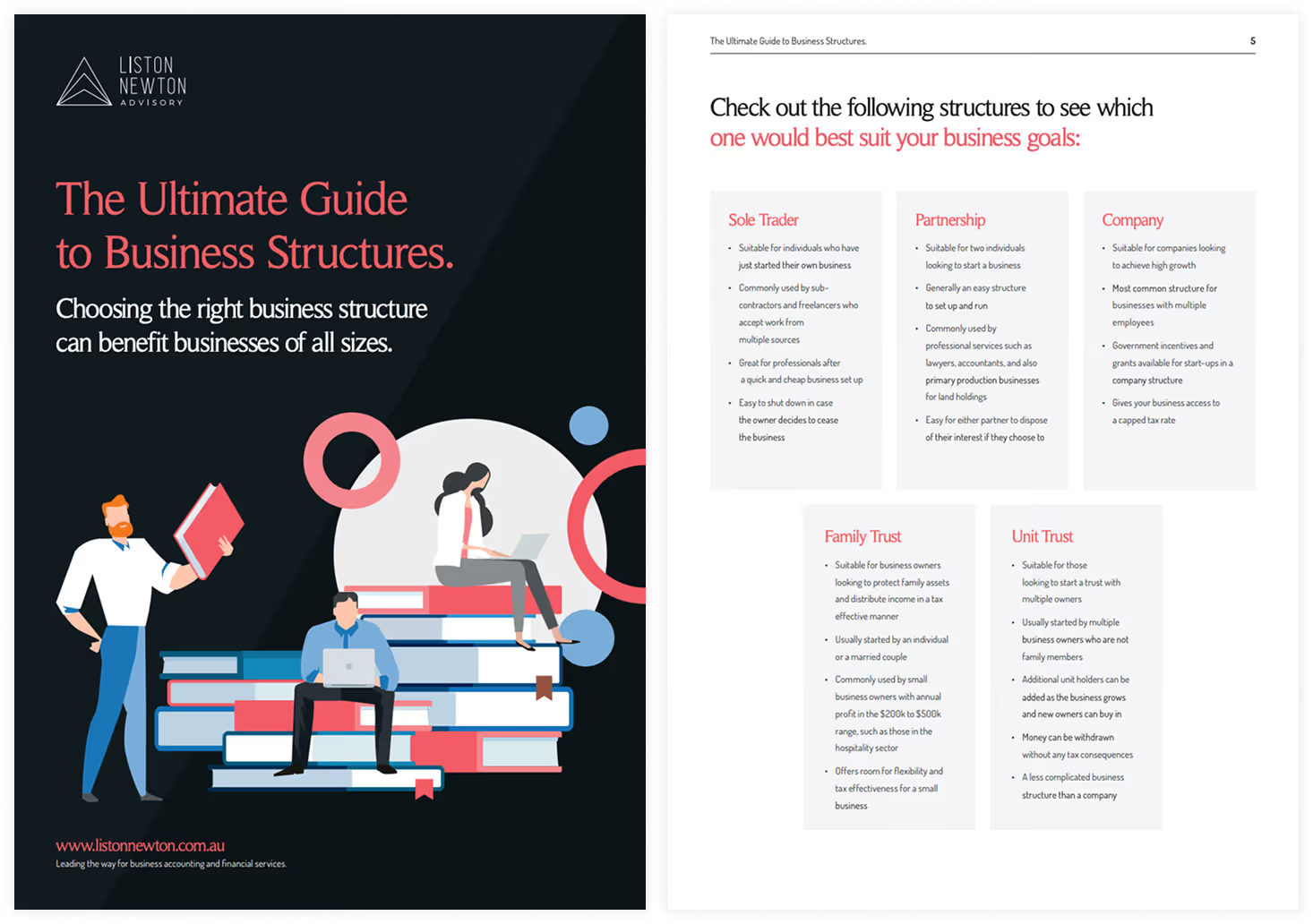

Your guide to business structures

Download Guide

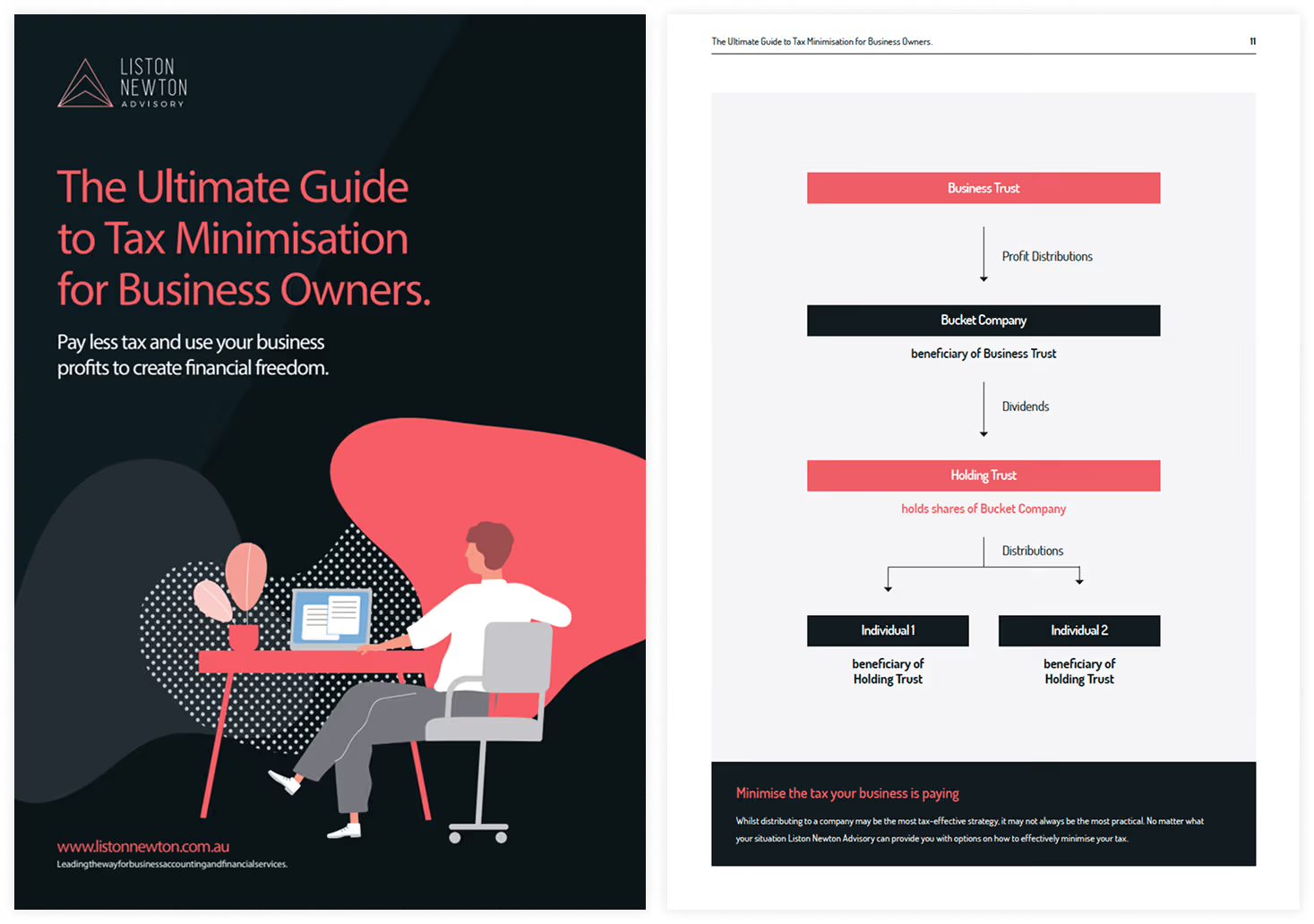

Your guide to tax minimisation

Download Guide

We’ve served our clients for nearly half a century

We pride ourselves on offering tailored financial advice that helps our clients achieve financial freedom. With decades of experience in financial advisory and a deep understanding of the industry, we’re committed to supporting you every step of the way.

We combine our comprehensive industry knowledge with a client-first approach to address immediate salary sacrifice concerns and support your long-term financial growth. Trust our expertise to guide you confidently through the complexities of salary sacrifice financial advice.

The benefits of partnering with us

- Personalised strategies tailored to your unique financial needs

- Over 40 years of experience in financial advisory

- Award-winning services recognised across the financial industry

- Ongoing support and strategic adjustments to adapt to changing conditions

- Access to leading financial tools and insights that empower decision-making

.avif)

Your path to achieving financial freedom

Achieving your financial goals is easier with a clear plan. Our streamlined process provides the guidance and support you need with transparent steps and consistent communication.

Initial consultation

We take a comprehensive look at your financial goals and assess your current salary package.

Strategy development

We create a personalised plan with actionable steps to optimise your salary sacrifice arrangement.

Implementation and review

We guide you through implementing the plan and regularly review it to keep it on track.

Case studies

Close

Accounting

Claudia Martin

With Liston Newton’s help, Claudia Martin was able to sell her business tax-free, gain clarity in her retirement planning, and make smart investment decisions.

Take a lookWe work with clients across Australia

Our services are accessible nationwide, with offices in Melbourne, Sydney, and Brisbane, as well as virtual consultation options. Whether you prefer in-person meetings or online support, our dedicated team is here to guide you through your financial journey.

South Melbourne

Level 3/67 Palmerston Crescent, South Melbourne, VIC 3205

Melbourne

17/31 Queen St, Melbourne VIC 3000

Malvern

Suite 175/45 Glenferrie Road, Malvern, VIC 3144

Donald

36 Woods Street, Donald VIC 3480

Gold Coast

Level 10, 36 Marine Parade Commercial Tower, 36 Marine Parade, Southport QLD 4215

Sydney

Level 22-23, Salesforce Tower, 180 George Street, Sydney, NSW 2000

Essential reading

Frequently asked questions

What is salary sacrificing, and how does it work?

Salary sacrificing allows you to reduce your taxable income by directing some of your pre-tax salary into benefits like superannuation, reducing the amount of tax you pay. By restructuring your salary package, you can maximise your tax benefits and improve your overall financial position.

How do salary sacrifice contributions affect my concessional contributions cap?

Salary sacrifice contributions count towards your concessional contributions cap, which is the limit on the amount of concessional contributions you can make to your super each year. Staying within this cap is essential to avoid additional taxes, and our advisors can help you navigate these limits effectively.

What are the tax implications of salary sacrificing for fringe benefits?

A fringe benefit received through salary sacrificing can be exempt from tax, providing significant savings. However, some benefits may require you to pay fringe benefits tax, so it's important to understand how these rules apply to your specific situation. Our accountants will help you pay tax on your fringe benefits in the most efficient way possible.

Ready to optimise your salary sacrifice strategy?

Book a consultation with our salary sacrifice financial advisors today and discover how personalised advice can help you maximise your financial potential.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Powered by EngineRoom

Free financial strategy session*

Get a free 60-minute video consultation. See how it works.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.