Our Locations

COVID-19: Liston Newton is here to support your business continuity planning. Get started

Our new head office is now in South Melbourne - See address

Call us today

Home downsizing services

Unlock equity and simplify life with our retirement downsizing accountants

Get a free 60-minute financial strategy session.

Book now

We’ve proved our expertise

A wealth of experience

With decades of experience, we’ve guided countless clients through the financial complexities of downsizing.

Tailored investment advice

We customise strategies to align with your financial goals and unique circumstances.

Long-term client partnerships

We’re committed to providing ongoing support as your needs evolve.

A full range of services

From financial planning to tax optimisation, we cover every aspect of your downsizing journey.

Downsizing your home can transform your retirement

Downsizing is a life-changing decision. It’s an opportunity to reduce expenses, simplify your living arrangements, and unlock the value tied up in your current home. But this process involves more than just finding a new place to live.

We help you plan strategically, ensuring your move maximises both your lifestyle and financial position. From understanding how downsizing impacts your retirement goals to exploring the tax implications, we provide expert guidance tailored to your needs.

Whether you’re looking to boost your retirement income, invest in property, or contribute to your super, we’ll help you navigate every step of the process with confidence.

How we help you downsize with confidence

Our team ensures your downsizing journey is seamless, from the initial planning stages to settling into your new home. We focus on aligning your financial strategy with your personal goals, making sure the equity you unlock works hard for you.

We’ll help keep your finances safe and secure

- Explore our comprehensive retirement planning services for a secure financial future

- Personalised downsizing strategies to maximise your wealth

- Discover tailored investment options for retirement to grow your wealth

- Clear guidance on super and pension contributions

- Get expert pension planning advice to optimise your retirement income

- Expert advice on managing debt and financing options

- Learn how to make the most of your transition to retirement with our step-by-step guidance

- Insights into property investment opportunities

- Proactive tax considerations to reduce liabilities

- Support with navigating government incentives and schemes

- Ongoing financial reviews to adapt to your changing needs

Take the first step toward a financially secure retirement

Get in touch

Make the most of downsizer contributions

One of the key financial benefits of downsizing is the ability to make a downsizer contribution to your superannuation. This process allows eligible Australians to boost their retirement savings with up to $300,000 in downsizer contributions from the sale of an investment property or their primary residence.

Our team will help you understand your eligibility, guide you through the process, and ensure you maximise the benefits of this valuable opportunity. With the right strategy, downsizer contributions can significantly enhance your retirement income.

%20160x160.avif)

Explore flexible financing options for your next home

Financing a downsized home requires careful consideration, especially if you’re transitioning from a mortgage-free property. We offer expert advice on options like:

Downsize with confidence

- Downsizing bridging loans: Ideal if you need to buy before selling your current home.

- Reverse mortgages: Access your home equity without selling, providing cash flow flexibility.

- Traditional home loans for retirees: Tailored lending options to suit your reduced income.

Unlock new opportunities with investment property

Downsizing doesn’t have to mean stepping away from property investment. If you’re considering using the equity from your home sale to invest in real estate, we’ll help you explore opportunities that align with your goals.

From rental properties to commercial ventures, our team will help you evaluate the risks and rewards, ensuring your investment strategy supports your long-term financial objectives.

Borrowing to downsize: what you need to know

If you’re considering borrowing to finance your downsized home, it’s important to understand how this decision fits into your broader financial plan. Borrowing later in life comes with unique challenges, but it can also be an effective strategy when managed correctly.

We help you assess your borrowing capacity, compare loan options, and structure your finances to ensure any debt remains manageable.

Key considerations we’ll guide you through include:

Assessing the impact of borrowing on your retirement income

- Understanding lender requirements for retirees

- Evaluating the cost of borrowing versus the benefits of downsizing

- Exploring debt repayment strategies that align with your financial goals

- Balancing debt with other retirement planning priorities

Backed by Australia’s top financial organisations

Our membership in Australia’s leading financial bodies reflects our commitment to delivering trusted, high-quality advice. These partnerships ensure we stay at the forefront of industry standards, providing you with the expertise you can rely on.

Our 5-star reviews

Kieran Liston and the Liston Newton team have been assisting me with my accounting matters since 1976. For the past 47 years, Kieran and the Liston Newton team have provided reliable accounting assistance, which has allowed me to focus on my business in primary production.

Their exceptional service has consistently exceeded my expectations and made me feel that they truly care about my financial well-being.

Liston Newton has given me really helpful guidance over the years for both my business and my personal finances. When you have an accounting team that you trust to give the right advice, it gives you the confidence to focus on growing your business and doing the things you love.

Liston Newton helped us move our accounting over to Xero. Their Accountant managed the set up and training so we felt comfortable with the software. We now have all our processes streamlined which gives us improved visibility of our business performance. This has allowed us to open 2 more stores without a significant increase in administration effort.

Download our essential financial guides

Our free guides offer practical insights to help you make informed decisions about your financial future. Download them today to get expert advice on:

- Retirement planning: Build a secure and fulfilling financial future

- Wealth creation: Grow your assets with proven investment strategies

- Financial goal setting: Create a personalised plan that aligns with your lifestyle

Smart wealth guide

Download Guide

Your guide to a successful retirement

Download Guide

Download our essential financial guides

Our free guides offer practical insights to help you make informed decisions about your financial future. Download them today to get expert advice on:

Virtual CFO guide

Download Guide

Smart wealth guide

Download GuideYour guide to a successful retirement

Download GuideYour guide to tax-effective business sales

Download Guide

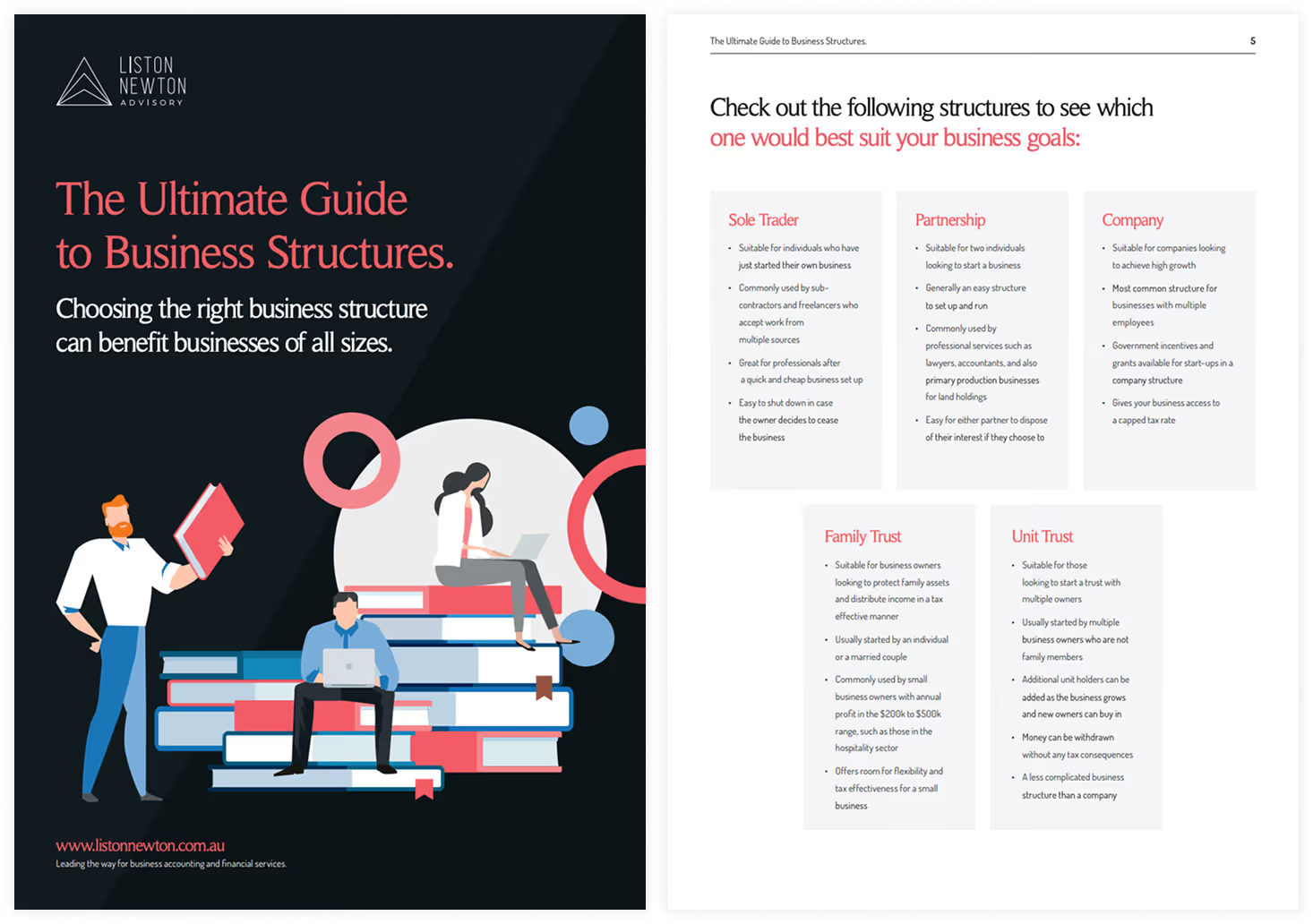

Your guide to business structures

Download Guide

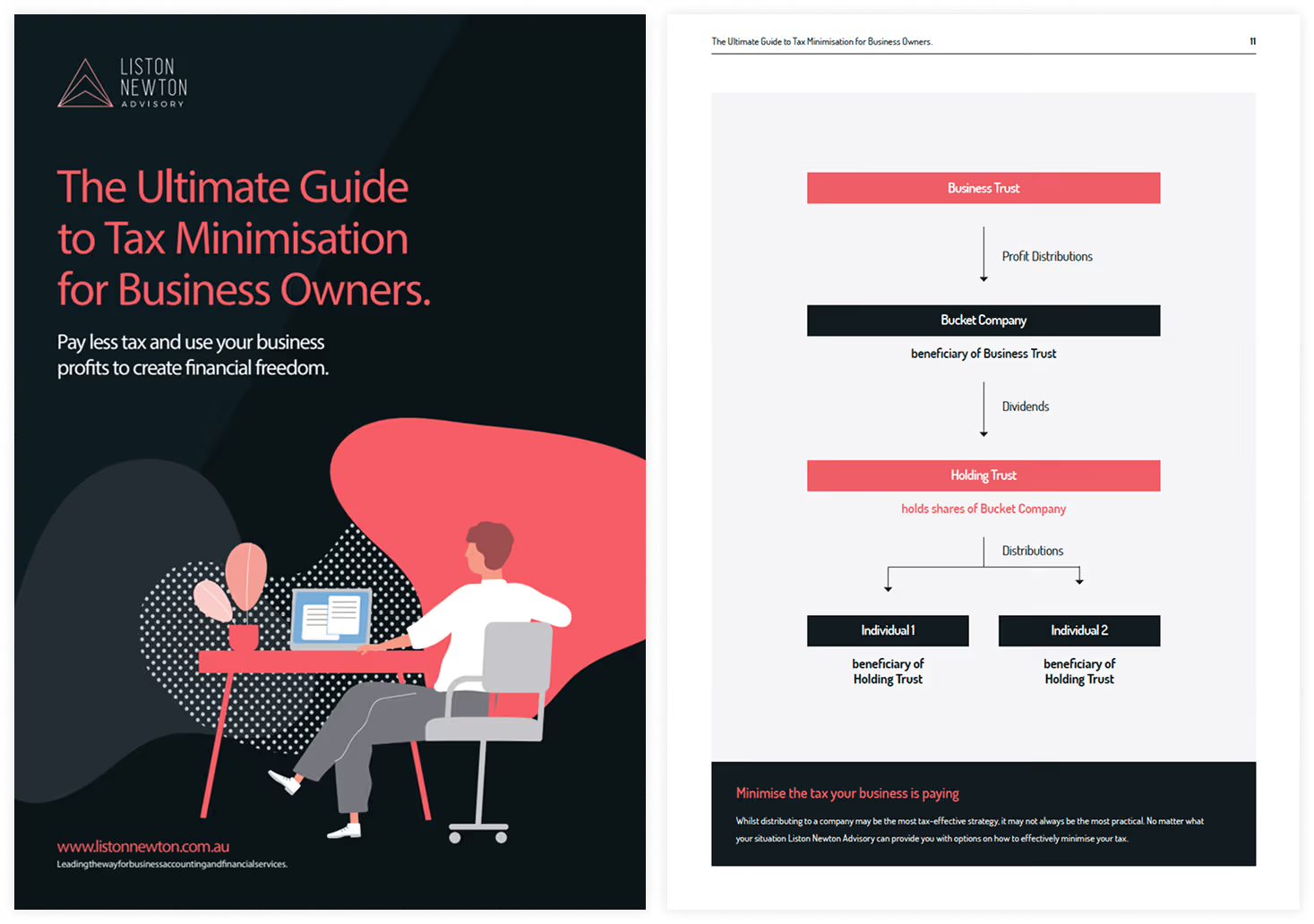

Your guide to tax minimisation

Download Guide

We’ve earned the trust of countless Australians. We’ll earn yours, too.

When you work with us, you’re not just getting financial advice — you’re gaining a trusted partner who will guide you through every stage of your downsizing journey. We’re here to help you make the most of your equity while ensuring your retirement goals are met with confidence.

Expect the best from your Liston Newton team

- Personalised strategies tailored to your financial goals

- Access to expert advice on superannuation and pension contributions

- Clear, actionable insights on managing debt and cash flow

- Expertise in property investment opportunities post-downsizing

- Transparent performance tracking and regular financial reviews

- Proactive risk management and tax planning

- Long-term partnerships focused on your financial success

“I look forward to working together for many years to come”

.avif)

Our proven approach to financial freedom

We use our Get Set, Get Moving, Get Free methodology to help you make the most of your downsizing decision:

Get Set

We build a strong foundation by optimising your income streams and tax strategies.

Get Moving

We help you unlock and grow your wealth through tailored financial planning and investment advice.

Get Free

We protect your assets, ensuring your financial future is secure and worry-free.

Our success stories

Close

Accounting

Chris & Leanne Roberts

After engaging Liston Newton's services, Chris & Leanne Roberts were able to purchase the B&B of their dreams by utilising their savings in the most tax-effective way.

Take a lookClose

Accounting

Claudia Martin

With Liston Newton’s help, Claudia Martin was able to sell her business tax-free, gain clarity in her retirement planning, and make smart investment decisions.

Take a lookClose

Accounting

Willow Urban Retreat

See how Willow Urban Retreat owner Jeremy gained clarity over his business performance and reduced time-consuming tasks with help from the Liston Newton team.

Take a lookSupporting clients across Australia

While our offices are based in Victoria, New South Wales, and Queensland, we work with clients across Australia. Whether you prefer face-to-face meetings or virtual consultations, we’re here to help you achieve your financial goals.

South Melbourne

Level 3/67 Palmerston Crescent, South Melbourne, VIC 3205

Melbourne

17/31 Queen St, Melbourne VIC 3000

Malvern

Suite 175/45 Glenferrie Road, Malvern, VIC 3144

Donald

36 Woods Street, Donald VIC 3480

Gold Coast

Level 10, 36 Marine Parade Commercial Tower, 36 Marine Parade, Southport QLD 4215

Sydney

Level 22-23, Salesforce Tower, 180 George Street, Sydney, NSW 2000

Expert insights and updates

Frequently asked questions

Can you make a downsizer contribution into a pension account?

Yes, you can make a downsizer contribution into your superannuation, which may later be used to fund an account-based pension. This strategy allows eligible Australians aged 55 and over to contribute up to $300,000 per individual ($600,000 per couple) from the proceeds of selling their primary residence.

Key points to consider:

- Eligibility: You must have owned your home for at least 10 years, and the property must qualify for a capital gains tax exemption.

- Impact on super: The contribution doesn’t count toward your contribution caps, but it may affect your total super balance and potential age pension entitlements.

- Tax efficiency: Once the funds are in super, they can be converted into a tax-free income stream if you’re over 60.

We’ll help you determine if a downsizer contribution is right for you and guide you through the process.

How does the downsizer superannuation contribution work?

The downsizer superannuation contribution enables Australians 65+ to use the proceeds from their home sale to make an after-tax contribution of up to $300k into their super account. Any contributions made in this matter don’t count towards your regular before- or after-tax super contributions.

In order to make eligible downsizer contributions, you must meet the following criteria:

- You’re 65 or older

- Your home is in Australia

- Your contribution comes directly from the sale of your home

- You make the contribution within 90 days of receiving the sale proceeds

- You have made no previous downsizer contributions.

Your super fund can supply you with a Downsizer contribution into super form to get you started.

What is the best way to finance the purchase of a downsized home?

The best financing option depends on your financial situation, timeline, and goals. Here are some common strategies:

- Selling first: Using the proceeds from your home sale is the most straightforward way to fund your new home purchase without taking on additional debt.

- A bridging loan: Ideal if you want to buy your new home before selling your current one. These short-term loans provide flexibility but come with higher interest rates.

- Reverse mortgages: Allow you to access the equity in your current home to fund your new purchase without immediate repayments.

- Home loans for retirees: Some lenders offer tailored home loans with flexible repayment options to suit those on a reduced or fixed income.

We assess your unique situation to recommend the most cost-effective and practical financing strategy for your downsizing journey.

What is the best age to downsize your home?

There’s no one-size-fits-all answer to the best age for downsizing. It depends on your financial goals, lifestyle preferences, and retirement plans. However, here are some common scenarios:

- In your 50s: Downsizing early can free up equity to invest or boost your superannuation while you’re still working.

- In your 60s: This is a popular time for downsizing, as many are transitioning into retirement and looking to reduce living expenses.

- In your 70s or later: Downsizing at this stage often focuses on moving to a more manageable property or closer to family and support networks.

We’ll help you evaluate your timing based on your financial position and long-term objectives, ensuring you make the move when it’s most beneficial.

When is a good time to downsize my home?

Downsizing a home means something different to everyone, so there are many different reasons for doing it. While there is no strict rule on the best time to downsize a home, you can often tell when the time has come.

- Do you have more rooms than you actually need? Maybe the kids have moved out, or you’ve gotten rid of a lot of belongings.

- You might be looking at a property with lower maintenance costs and less space to manage, or one that’s more accessible.

- For financial reasons, you might be looking at selling your larger existing property in favour of a smaller one.

- You might be looking to move closer to family.

- Or you simply might be looking to move to a new home, and you’re trying to make a sensible choice on the number of rooms you need to take care of.

There are many reasons you’d be looking at downsizing, and a good time to do it is when it feels right to you. But be sure to check with your financial adviser to discuss your options.

Is there a downside to downsizing?

While downsizing offers many benefits, it’s important to consider potential challenges:

- Emotional impact: Leaving a long-time family home can be emotionally difficult.

- Hidden costs: Expenses like stamp duty, property taxes, moving costs, and renovations can add up.

- Financial implications: Depending on how you use the proceeds, downsizing could affect your age pension eligibility or tax position.

- Market timing: Selling in a slow property market may reduce the amount of equity you can unlock.

Legal fees related to property transactions can impact your overall budget, so it’s important to factor them into your financial plan.

With careful planning, these downsides can be managed. Our team ensures you’re fully informed of the potential risks and benefits, helping you make a confident decision.

What to do first when downsizing?

The first step in downsizing is to get a clear picture of your financial and lifestyle goals. Here’s a practical approach:

- Evaluate your current financial position: Understand the equity in your home and how it fits into your retirement plan.

- Set your downsizing goals: Decide what you want to achieve — reducing expenses, simplifying your lifestyle, or freeing up funds for investments.

- Seek professional advice: Consulting with financial experts ensures you maximise the benefits and avoid costly mistakes.

- Declutter and prepare your home for sale: Start early to reduce stress and maximise your property’s value.

By following these steps, you’ll be well-prepared to begin your downsizing journey with confidence.

Do I need to buy a new home to access the downsizer super contribution?

No, once you sell your home, what you do next is your choice. You don’t need to buy a new home with the proceeds of your sale — you don’t need to use the money towards property, or even use it at all.

Will selling my home impact my ability to access the Age Pension?

Selling your property doesn’t impact your ability to access the age pension or your super pension under the assets test. Age Pension eligibility is based on the value of your assets and income at the time of the test. When selling your home, the proceeds from the sale are exempt for up to 12 months, as long as you plan to buy again, renovate, or build. It may impact your income, though, so check with your financial adviser to discuss your options.

Contact us to start your downsizing journey

Speak with one of our experts to get tailored downsizing advice and start planning your next move today.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Written by a specialist

No items found.

Powered by EngineRoom

Free financial strategy session*

Get a free 60-minute video consultation. See how it works.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.