Our Locations

COVID-19: Liston Newton is here to support your business continuity planning. Get started

Our new head office is now in South Melbourne - See address

Call us today

Lending advice

Get holistic lending advice to fund personal and professional goals

Get a free 60-minute financial strategy session.

Book now

How our lending advice benefits you

A wealth of experience

We have the knowledge and experience to help you find finance that suits you. We have a range of popular lending options, some of which may be new to you.

Connections with lenders

We have strong relationships with over 25 specialist lenders as well as the Big Four banks, who offer our clients reduced deposits.

Long-term client partnerships

By taking the time to understand your long-term goals, we can help you select the best lending choice for your circumstances.

Leading industry innovation

More than just bank loans, we can also offer lending advice on alternatives such as fintech and peer-to-peer lending.

Home and investment loan advice

Loans are invaluable (and, frankly, inevitable) for achieving your personal goals. Our lending advisors will help you manage that risk and secure a safe and manageable car or home loan.

In our line of work, we understand the importance of capitalising on opportunities as soon as they appear. In your case, that might mean purchasing that dream home before you’ve sold your current one. Our bridging loan advice will help you transition out of the old and into the new as quickly and easily as possible.

If you find that your existing loans are no longer manageable, we won’t leave you in the lurch. We can offer you comprehensive advice on refinancing your mortgage and put you in touch with lenders who can offer products that better suit your needs.

Tailored lending advice, all in one place

Talk to us

Business loan advice

Practically every business needs to cross this bridge at one time or another. Whether you’re looking for the capital to get up on your feet or you need a sudden safety net to survive unforeseen and uncontrollable challenges, the right loan can save your business.

Notice we said the “right” loan. Our loan accountants will help you vet products by assessing their fine print and ensuring that their terms and conditions serve your interests and abilities. With expertise in fintech and peer-to-peer lending and connections at major banks across Australia, we have the experience and resources you need to make the right decision.

Work with our business accountants to determine if and when seeking a loan is worth the risk.

%20160x160.avif)

Ongoing loan reviews to keep your obligations to a minimum

Why would we be happy with a job half done? Helping you select a loan is only the first step. Once you have, we’ll regularly assess your existing loans against evolving and emerging loan products to ensure that you always have the most competitive rates.

And that’s still not all. As you pay down your loan, we’ll run the numbers to determine whether you can borrow against your equity to build your wealth through other avenues (to build up your stock or property portfolio, for example).

But there’s still more. Unlike a standard broker, your Liston Newton loan advisor will help you structure your loan in the most tax-effective way possible, and guide you on borrowing in your own name or through a trust or company.

For us, it’s not just about finding the cheapest rate; it’s about building wealth. That’s the Liston Newton difference.

We're qualified and accredited

All our lending advisers are appropriately qualified and accredited to be the best in the business.

“This wouldn’t have been possible without Liston Newton Advisory…”

Kieran Liston and the Liston Newton team have been assisting me with my accounting matters since 1976. For the past 47 years, Kieran and the Liston Newton team have provided reliable accounting assistance, which has allowed me to focus on my business in primary production.

Their exceptional service has consistently exceeded my expectations and made me feel that they truly care about my financial well-being.

Liston Newton has given me really helpful guidance over the years for both my business and my personal finances. When you have an accounting team that you trust to give the right advice, it gives you the confidence to focus on growing your business and doing the things you love.

Liston Newton helped us move our accounting over to Xero. Their Accountant managed the set up and training so we felt comfortable with the software. We now have all our processes streamlined which gives us improved visibility of our business performance. This has allowed us to open 2 more stores without a significant increase in administration effort.

Free downloadable advice

We can’t imagine a drier sentence than “Would you like to read some financial advice brochures?” So believe us when we say we wouldn’t ask if we didn’t know it was worth your time.

Though they’re free, we haven’t held back on the details. Read these brochures at your leisure and they’ll give you a comprehensive overview of their topics.

If you’d like to ask questions, raise concerns and learn more, you know how to reach us.

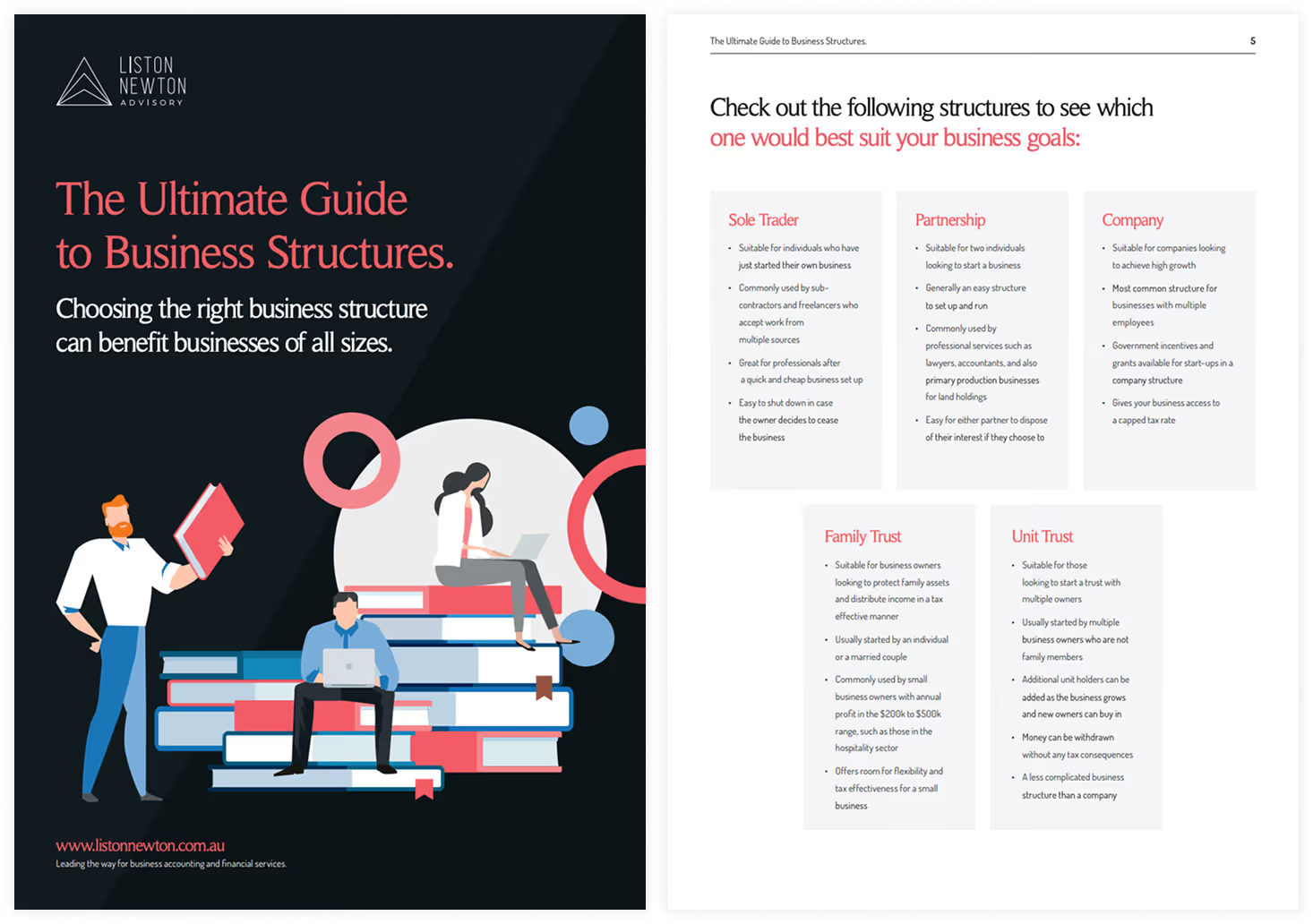

Your guide to business structures

Download Guide

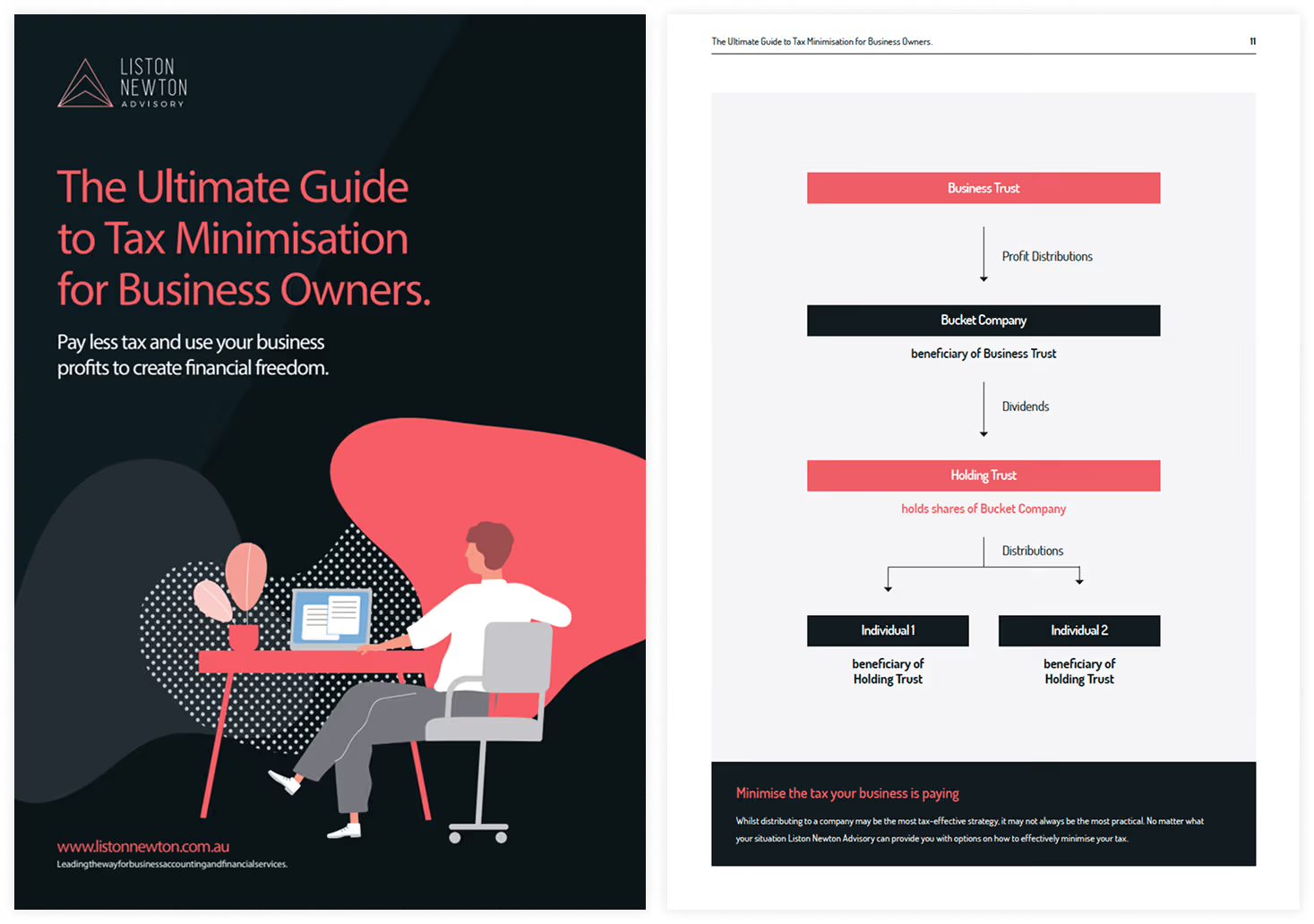

Your guide to tax minimisation

Download Guide

Free downloadable advice

Virtual CFO guide

Download Guide

Smart wealth guide

Download Guide

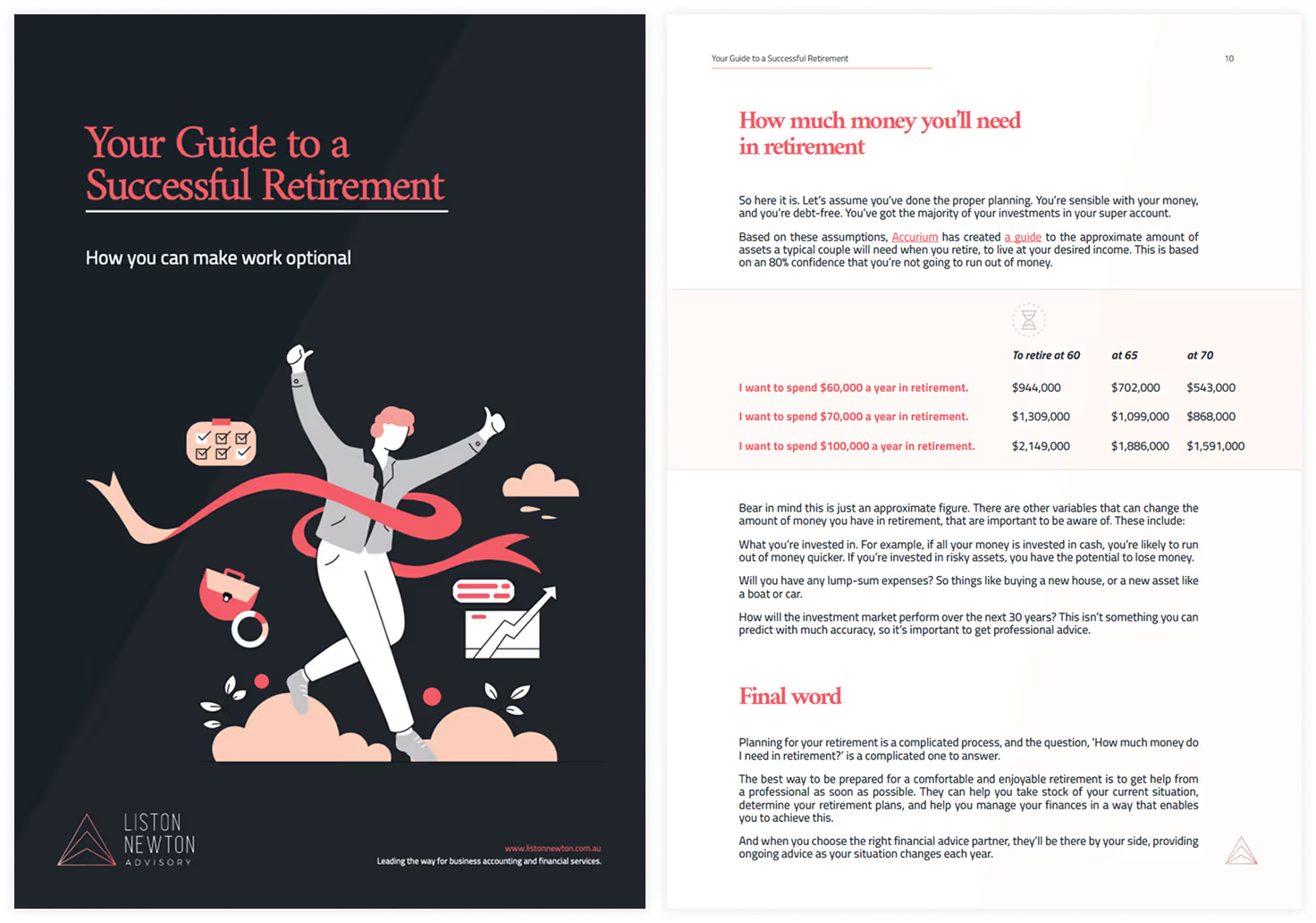

Your guide to a successful retirement

Download Guide

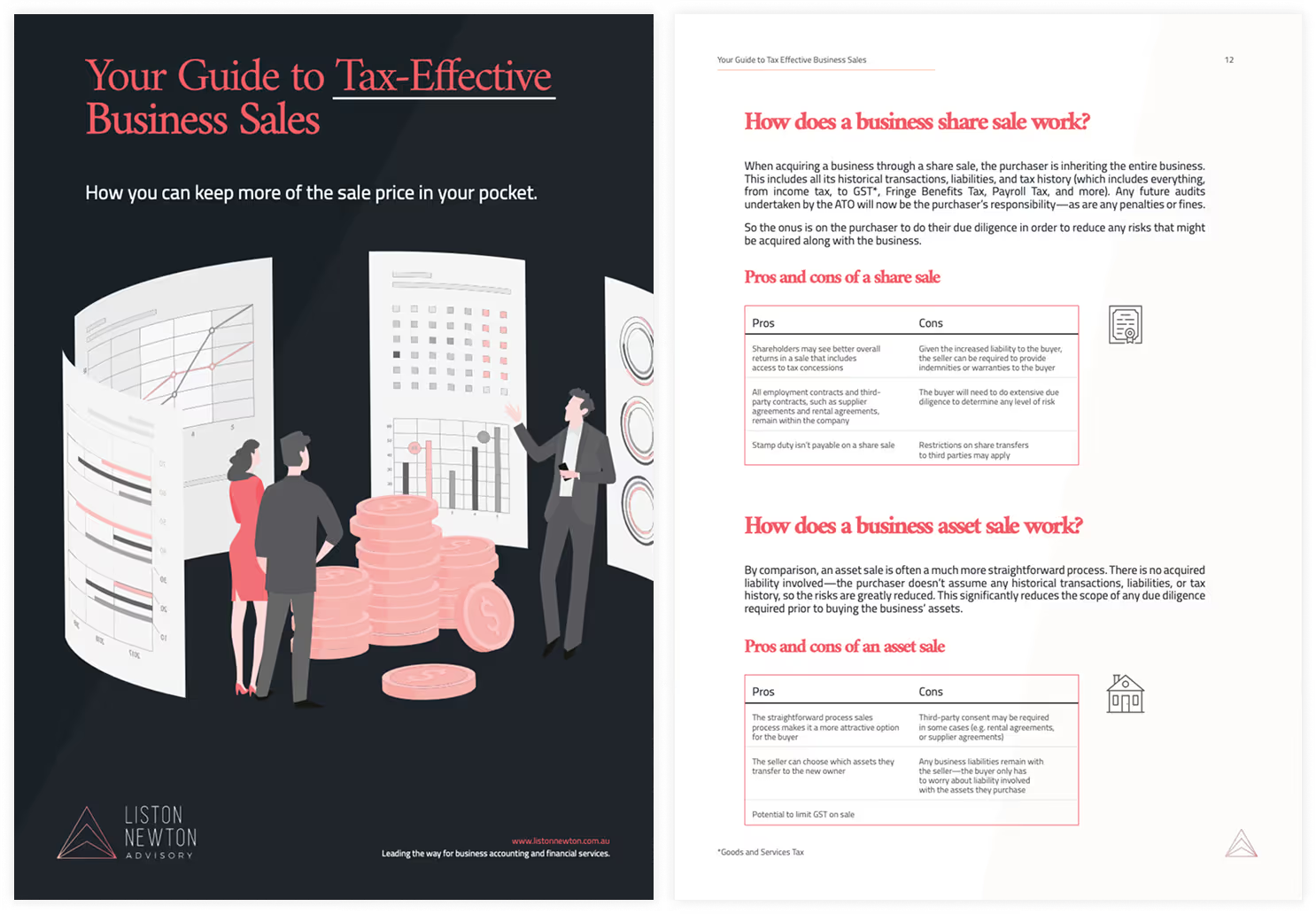

Your guide to tax-effective business sales

Download Guide

Your guide to business structures

Download GuideYour guide to tax minimisation

Download GuideWe’ve never betrayed the trust we’ve received

Everything in business is a risk; loans, especially. For us to offer you advice, we first have to earn your trust. Even if we have it, which we hope we do, you need to know that we won’t take it for granted.

This entire industry is built on trust, and we’ve thrived in it for nearly half a century. We’re proud to say we’ve earned several clients who’ve worked with us for a decade or more. We hope that fact tells you everything you need to know about who we are and how we do business.

The benefits of a Liston Newton partnership

- 40 years of industry experience

- Award-winning financial management services

- Guaranteed ATO compliance

- Xero Platinum partner

- Tailored business advisory offerings

.avif)

Reaching financial freedom

That’s the dream, isn’t it? Whether you’re looking to invest in property or make sure there’s a sizeable inheritance for your kids, you can pursue your professional and personal passions with the freedom of knowing that money isn’t going to be a barrier to stress about.We’ve designed a methodology to help you achieve that freedom. We call it Get Set, Get Moving, Get Free, and its a long-term strategy for our long-term clients. It’s worth the investment — it’s the exact same approach we take ourselves. Here’s how it goes:

Get set

We refine and fortify your existing business by getting your accounts in order and minimising risks.

Get moving

We grow and develop your business and your personal wealth through long-term strategies.

Get free

Our financial advisors help you plan for and meet your personal financial goals with the wealth you’ve built.

Case study

Close

Lending

Alison Bartlett

Alison Bartlett worked with Liston Newton’s lending team to help secure her dream holiday home. We stepped Alison through multiple repayment scenarios and servicing calculations.

Take a lookOur locations

The locations we’ve listed below are our offices, not our limits. We work with businesses across Australia, in all states and territories, and based anywhere from the capital cities to regional towns. We’ll gladly come out to your offices for a handshake, but we can also organise virtual conferences to make communication quicker and easier for all of us.

South Melbourne

Level 3/67 Palmerston Crescent, South Melbourne, VIC 3205

Melbourne

17/31 Queen St, Melbourne VIC 3000

Malvern

Suite 175/45 Glenferrie Road, Malvern, VIC 3144

Donald

36 Woods Street, Donald VIC 3480

Gold Coast

Level 10, 36 Marine Parade Commercial Tower, 36 Marine Parade, Southport QLD 4215

Sydney

Level 22-23, Salesforce Tower, 180 George Street, Sydney, NSW 2000

More worthwhile reading

Frequently asked questions

How much do I need to deposit?

Generally, most lenders require a 20 per cent deposit, while some lenders will allow you to go down to a 15 per cent deposit.

If you only wish to have a 10 percent or 5 percent deposit, you may need to pay Lenders Mortgage Insurance (LMI). LMI is an additional fee paid to a third-party insurer. Often, this fee can be added to the loan.

You must also factor in bank fees, legal fees, and stamp duty.

How do I get my mortgage down faster?

If you want to repay you mortgage as fast as possible, there are a number of things you can do, including:

- Repay your loan fortnightly rather than monthly, this will save interest over the life of the loan.

- Make additional payments.

- If you have a variable loan, you can use an offset account to place your savings into. This will offset the interest on your loan and will reduce interest charges.

- Look for the lowest rate possible.

Will the banks lend to me?

Banks will look at a number of factors when considering any finance application, including:

- Your employment

- Your cash savings

- Your business financials if you are self-employed

- Your credit history

- How much other debt you have outstanding

Often with the help of a professional, you can negotiate your way into a loan which is appropriate for your circumstances.

What is stamp duty?

Stamp duty is a type of tax that is paid when you purchase real estate in Australia. The amount of stamp duty you pay depends on the state you live in; it's generally between 5 and 5.5 per cent.

As a first-home buyer, you may be exempt from stamp duty or eligible for a stamp duty discount. For newly built homes and apartments, the stamp duty is often waived.

How much can I borrow?

This depends on your savings. Generally, you can borrow between 80 and 95 per cent of the value of the property you are purchasing. That means you need to have the remaining amount in savings.

You will also be assessed on your ability to service the loan. Serviceability is measured on how much income you earn each year, your expenditure and also any other outstanding debts.

Need to speak to an expert?

We've got answers to suit your situation. We have great relationships with the big banks, plus many more lending options to advise you on.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Powered by EngineRoom

Free financial strategy session*

Get a free 60-minute video consultation. See how it works.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.