Our Locations

COVID-19: Liston Newton is here to support your business continuity planning. Get started

Our new head office is now in South Melbourne - See address

Call us today

Setting up a self-managed super fund

Talk to our SMSF accountants today

Get a free 60-minute financial strategy session.

Book now

Insights and advice from an SMSF firm-of-the-year winner

A wealth of experience

We’ve been providing award-winning SMSF advice for over 40 years. Our experience is second to none.

Long-term client partnerships

We make it our mission to fully understand your unique priorities and help you to form the best plans for your future.

Leading industry innovation

Our industry-leading technology and software are designed to make successful super investments easier and more straightforward than ever.

Set up an SMSF investment strategy today with tomorrow’s needs in mind

The primary benefit of a self-managed super is control: the ability to design your fund to suit your unique lifestyle needs and future goals, and to adapt how it operates as your needs evolve. Setting up an SMSF can be a prudent, rewarding decision — but it has its risks. Our advisors will help you minimise those risks and maximise your returns.

While we certainly invite you to glance through the list of awards we’ve won or been shortlisted for, they don’t fully capture the level of service we provide. To understand that, you’d have to meet the nearly 300 clients who’ve trusted us to set up their supers, and to continue running them for decades.

Trust is the currency our business runs on, and we will earn yours.

Setting up your super fund is only the first step. Let’s keep going.

We didn’t earn our laurels by stopping at the start. Getting the most out of a self-managed fund means remaining in an ‘always-on’ state and setting up a process for regular fund reviews and investment calibrations. It’s a challenging task, but one we have significant proven experience in.

Liston Newton’s SMSF advisors will help you set up a unique fund tailored to your unique goals. We’ll help you:

- Oversee the SMSF establishment and ongoing fund administration

- Discern the best structure for fund members

- Compose a trust deed

- Consolidate multiple super accounts

- Design an SMSF investment strategy

- Clarify how to accept contributions

- Pay expenses and ongoing costs

- Submit financial statements

- Guarantee SMSF tax compliance

- Claim tax concessions

- Plan how and when to access fund assets

Set up the perfect SMSF with Liston Newton Advisory

Talk to us

%20160x160.avif)

Our bona fides

Our accredited SMSF advisory services give you complete peace of mind.

“The Liston Newton team were exceptional”

Kieran Liston and the Liston Newton team have been assisting me with my accounting matters since 1976. For the past 47 years, Kieran and the Liston Newton team have provided reliable accounting assistance, which has allowed me to focus on my business in primary production.

Their exceptional service has consistently exceeded my expectations and made me feel that they truly care about my financial well-being.

Liston Newton has given me really helpful guidance over the years for both my business and my personal finances. When you have an accounting team that you trust to give the right advice, it gives you the confidence to focus on growing your business and doing the things you love.

Liston Newton helped us move our accounting over to Xero. Their Accountant managed the set up and training so we felt comfortable with the software. We now have all our processes streamlined which gives us improved visibility of our business performance. This has allowed us to open 2 more stores without a significant increase in administration effort.

Seize every opportunity with our downloadable financial guides

Fortifying your super isn’t the only way to grow and protect your wealth.

Our financial specialists have written a suite of free downloadable guides to educate you on a range of key topics. These guides offer unique insights and facts, as well as actionable tips and strategies.

Topics we cover include:

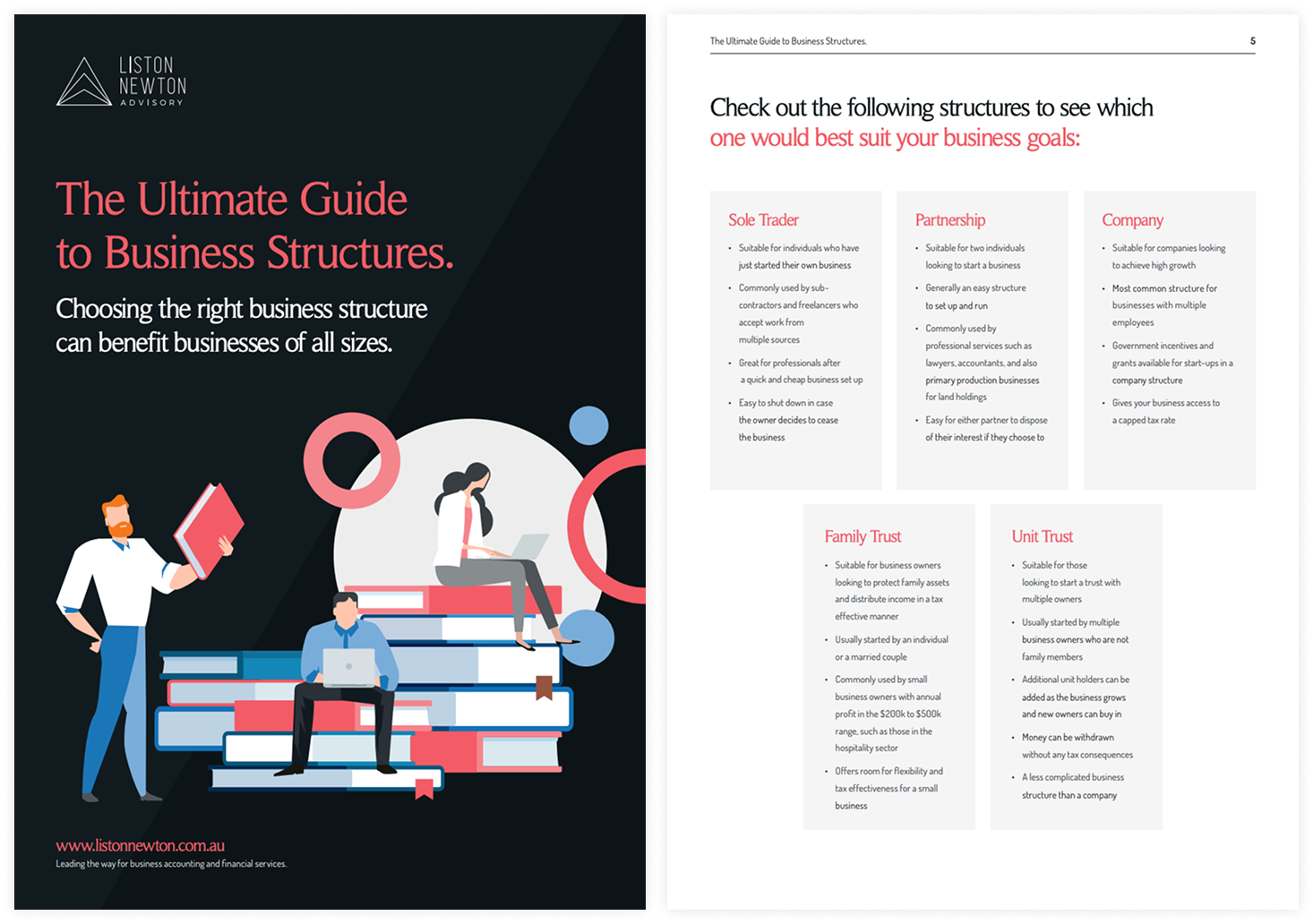

Your guide to business structures

Download Guide

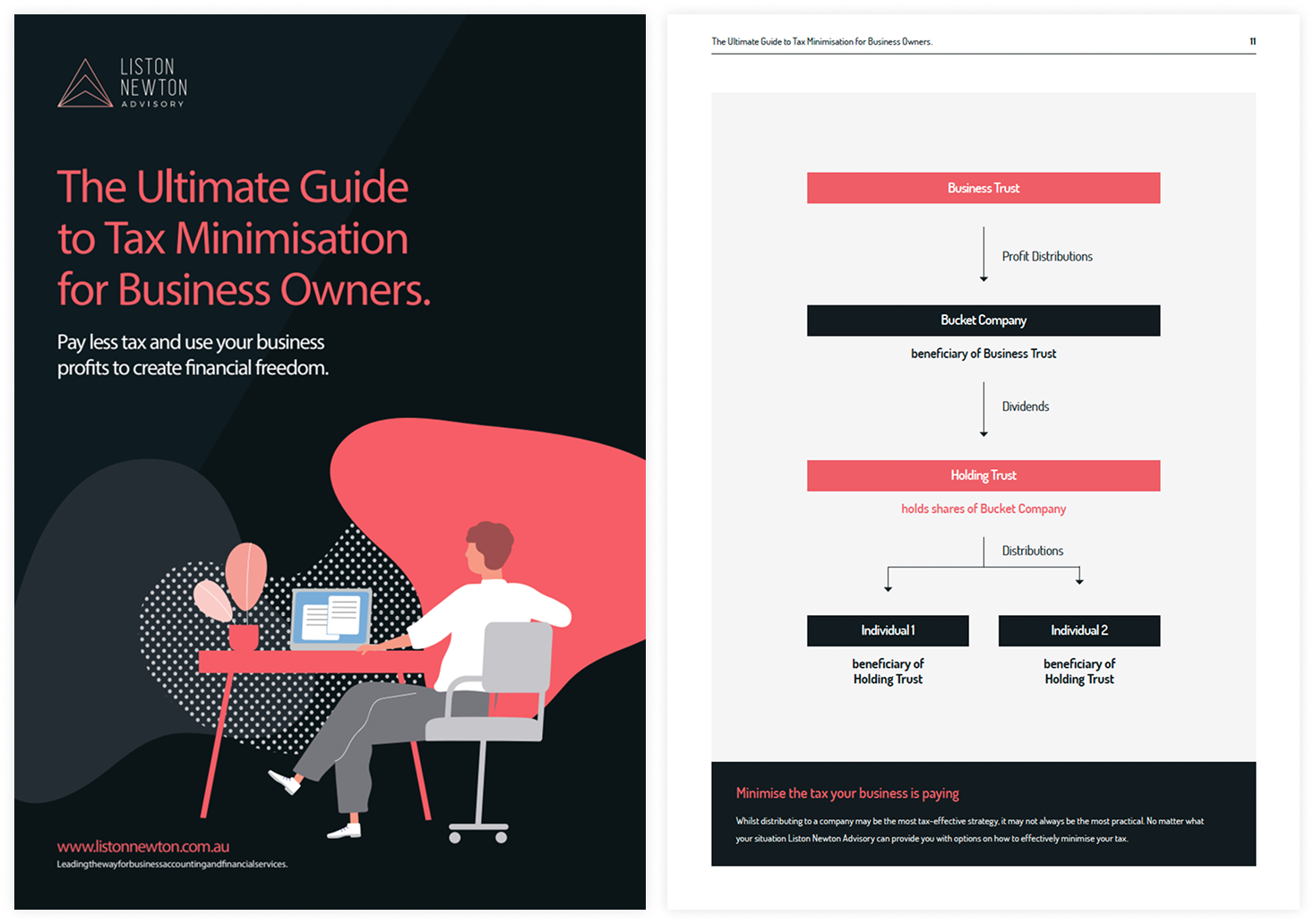

Your guide to tax minimisation

Download Guide

Seize every opportunity with our downloadable financial guides

Fortifying your super isn’t the only way to grow and protect your wealth.

Our financial specialists have written a suite of free downloadable guides to educate you on a range of key topics. These guides offer unique insights and facts, as well as actionable tips and strategies.

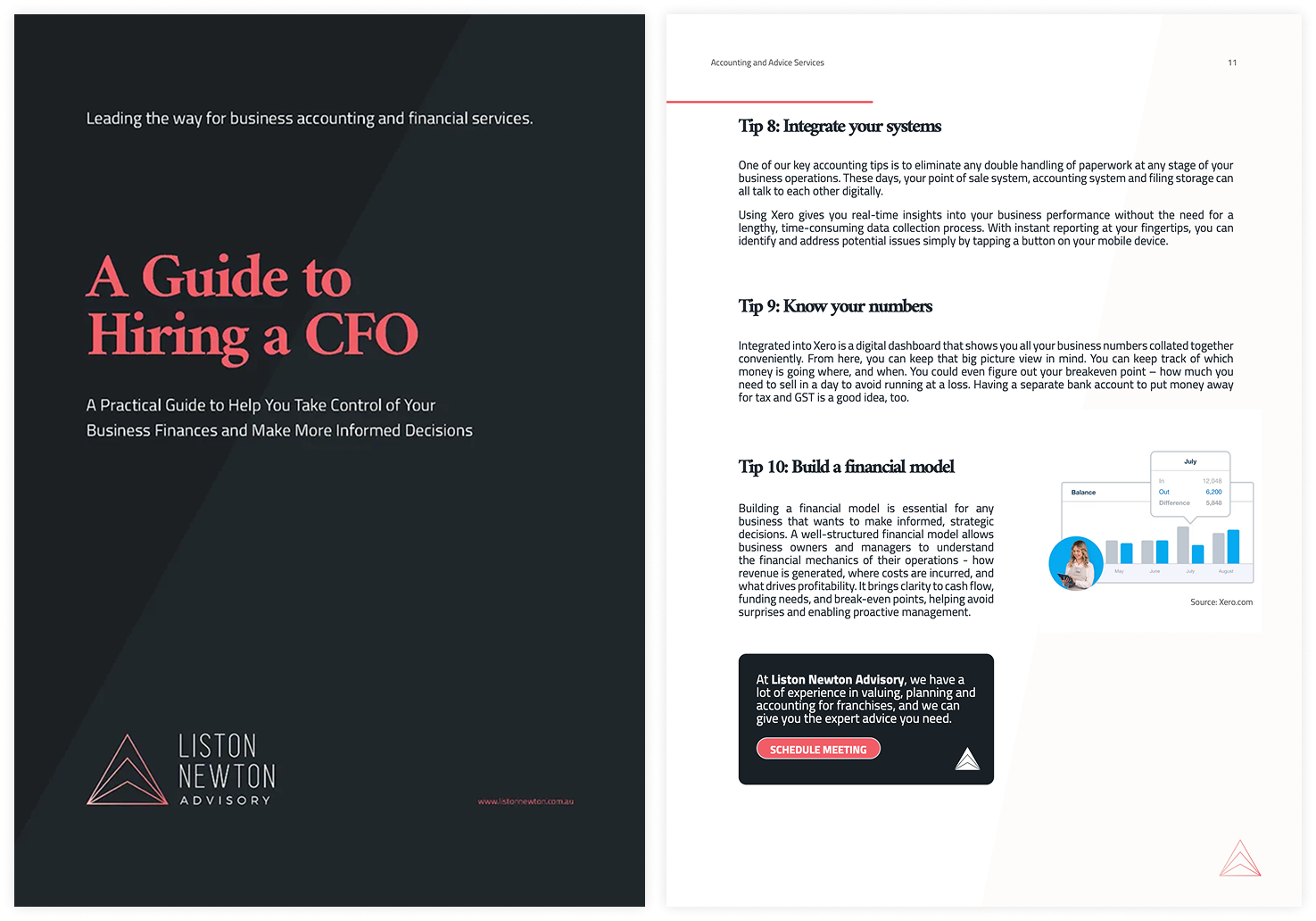

Virtual CFO guide

Download Guide

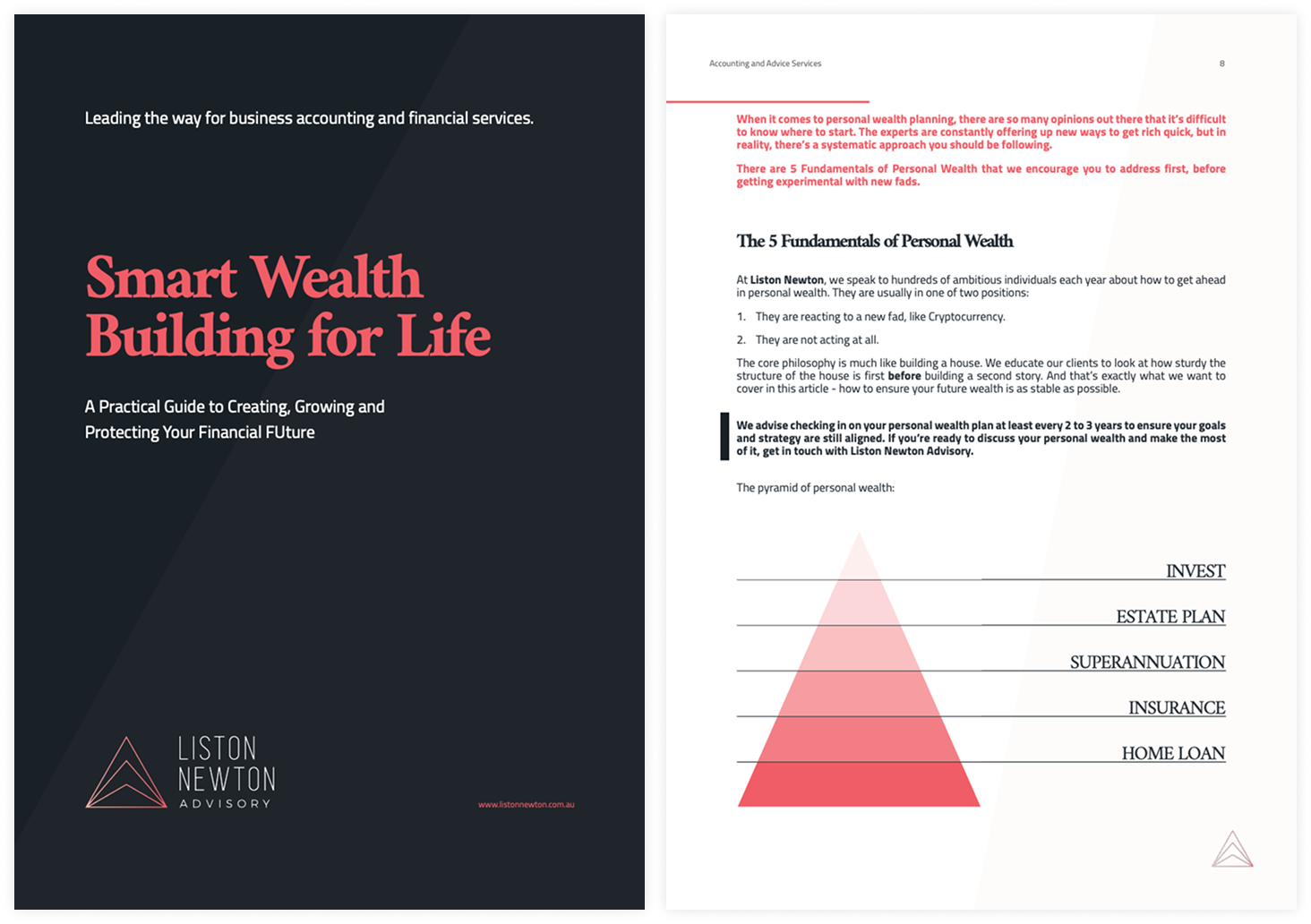

Smart wealth guide

Download Guide

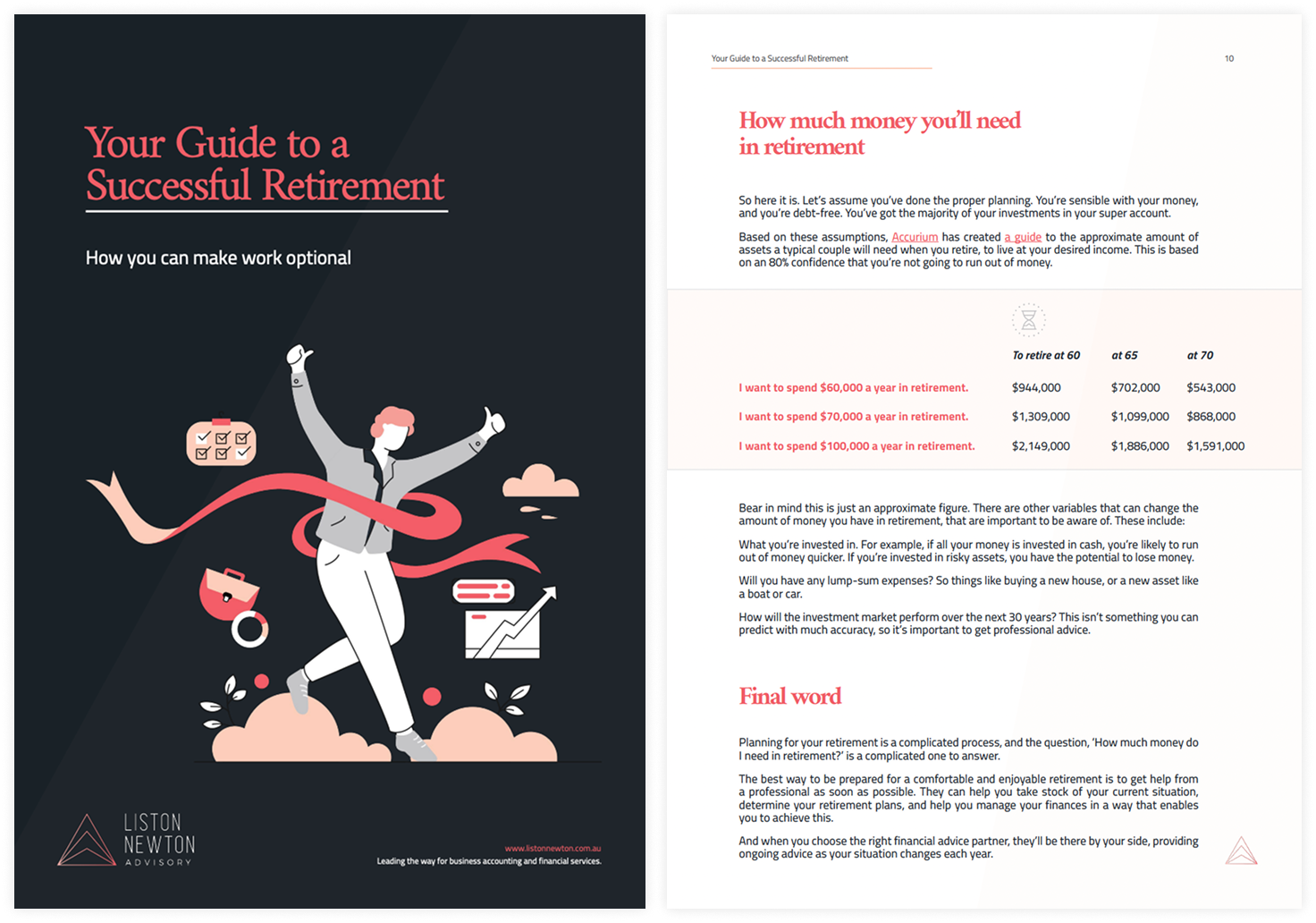

Your guide to a successful retirement

Download Guide

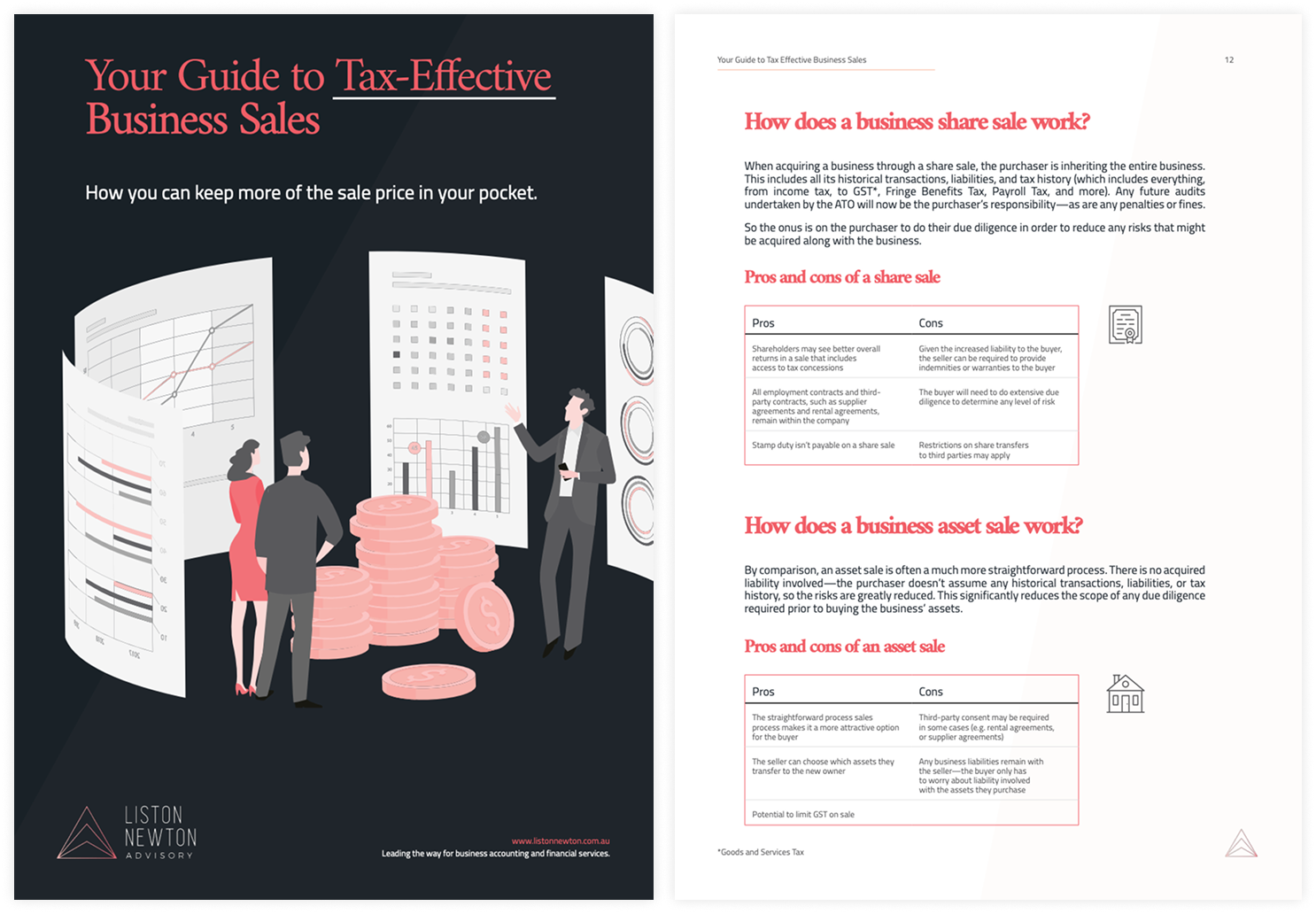

Your guide to tax-effective business sales

Download Guide

Your guide to business structures

Download GuideYour guide to tax minimisation

Download GuideDecades of experience. Hundreds of clients.

Liston Newton Advisory was established just over a decade before supers became compulsory. We’ve studied how these funds have evolved since their nascency, tracking legislation and learning how best to tailor funds to each client’s unique needs.

Today, we guide the self-managed super funds of nearly 300 clients. And that’s only our SMSF clients.

When you partner with Liston Newton, you gain access to one of the most comprehensive financial advisory services in Australia.

The benefits of a Liston Newton partnership

- 40 years of industry experience

- Award-winning financial management services

- Guaranteed ATO compliance

- Xero Platinum partner

- Tailored business advisory offerings

Meet your SMSF team

.png)

.png)

.png)

Your next steps

Ours will be an ongoing partnership that will, hopefully, last well into your retirement. Here’s how it’ll begin.

Consult

We'll first meet for a no-obligation chat to determine whether we are right for each other. We’ll discuss your financial and personal goals.

Optimise

We’ll implement short-term strategies to organise your funds, including locating and consolidating lost accounts.

Grow

With the basics now sorted, we’ll then work on more comprehensive strategies, which may mean restructuring or setting up entirely new accounts, to get you the best possible returns.

Close

SMSF

Chris & Leanne Roberts

After engaging Liston Newton's services, Chris & Leanne Roberts were able to purchase the B&B of their dreams by utilising their savings in the most tax-effective way.

Take a lookOur locations

We have six offices across the east, from which we can provide accounting services for metropolitan and regional businesses alike. Rest assured that our services are available to you no matter what state or territory you’re based in, and we’ll gladly make the trip over for a handshake, coffee and a consultation.

South Melbourne

Level 3/67 Palmerston Crescent, South Melbourne, VIC 3205

Melbourne

17/31 Queen St, Melbourne VIC 3000

Malvern

Suite 175/45 Glenferrie Road, Malvern, VIC 3144

Donald

36 Woods Street, Donald VIC 3480

Gold Coast

Level 10, 36 Marine Parade Commercial Tower, 36 Marine Parade, Southport QLD 4215

Sydney

Level 22-23, Salesforce Tower, 180 George Street, Sydney, NSW 2000

Related resources

Frequently asked questions

Do I need to set up and run my investment fund myself?

Not at all. While we do believe that if you're taking the time to set up an SMSF, you should take a keen interest in how it's run and gradually educate yourself more each year, the beauty of an SMSF is that you can have as little or as much input into your investment decisions as you like.

Our advisers are here to help you run your SMSF in a way that will best benefit you and your family, now and in the future.

How much can I contribute each year?

You can choose from two main types of contributions:

- With the first, each member makes a tax-deductible contribution of up to $25,000 annually (including whatever amount your employer contributes to you).

- With the second, each member can also contribute $100,000 per year as a non-tax deductible contribution.

Additionally, you can make several other special contributions. For example, if you sell a small business, you can contribute up to $500,000 of the capital gain to reduce your tax.

Can I invest in property in my SMSF?

Yes, you can. You may invest in residential, commercial or industrial property. Commercial or industrial property may be leased back to your business. If you invest in residential property, it must be leased to an unrelated party.

Investing in property can be a good option for some SMSFs. However, you must carefully consider whether this is the best strategy for your retirement planning. In recent years, the interest rates and fees for property loans have increased dramatically. Also, for high-income earners, it can make more sense from a tax perspective to invest in property outside super.

How do franking credits work in a SMSF?

Investing in Australian shares in an SMSF can be a great option due to the additional franking credits available.

Franked dividends are dividends or profits paid to shareholders by a company that pays company tax in Australia on part or all of the profit distributed as a dividend.

Generally, a listed company pays tax at a rate of 30 per cent. A shareholder who receives a franked dividend can claim a tax offset for the franking credits (otherwise known as imputation credits) attached to the franked dividend.

In practice, this would mean that if your SMSF owned BHP shares and a $1,000 dividend were declared, you would receive $700 as cash, and BHP would pay $300 (30%) in tax. If your SMSF is in pension mode on a 0% tax rate, you would then receive the $300 tax as a refund when you lodge your tax return.

What happens to my SMSF when I pass away?

SMSFs offer great flexibility with your estate planning needs. A member of an SMSF can make binding death benefit nominations (BDBN) that do not lapse — unlike many public offer superannuation funds, which tend to require binding death benefit nominations to be updated every three years.

A BDBN is like a Will for your SMSF. It allows you to direct your SMSF balance to the exact person you want to receive that money. If set up correctly, a BDBN is very difficult to challenge in a dispute.

What is the difference between an individual and corporate trustee structure?

Choosing between an individual trustee structure and a corporate trustee structure can impact how your fund is managed and administered. Here are the key differences:

Individual trustee structure

- Trustee requirements:some text

- Requires at least two individual trustees, and all members of the fund must be trustees.

- Asset ownership:some text

- Fund assets are held in the names of the individual trustees, which means ownership changes if membership changes.

- Liability:some text

- Trustees face unlimited personal liability, putting their personal assets at risk if the fund incurs liabilities.

- Administration:some text

- Changing trustees can be administratively challenging, as it involves re-registering assets in the new trustees' names.

Corporate trustee structure

- Trustee requirements:some text

- Involves a company acting as the trustee, with all fund members as directors of the company.

- Asset ownership:some text

- The company holds the legal ownership of the fund’s assets, maintaining consistent ownership even if membership changes.

- Liability:some text

- Offers limited liability protection, reducing personal risk for directors.

- Administration:some text

- Simplifies management and succession planning, as the corporate trustee remains constant regardless of membership changes.

Talk to our SMSF accountants today

The first step is a free, no-obligation consultation. Let’s have a chat and see what we can do for you.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Powered by EngineRoom

Free financial strategy session*

Get a free 60-minute video consultation. See how it works.

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.