Minimising tax isn’t about cutting corners — it’s about using smart, legal tax planning strategies to keep more of your hard-earned money. At Liston Newton, we’ve spent over 40 years helping business owners and high-income earners reduce their tax burden while staying compliant with Australian tax laws.

Our team of experienced tax accountants and financial advisers specialise in personalised tax planning for high-income earners to help you reduce your tax burden while staying compliant with Australian tax laws. In this guide, we explore eight ways high earners can maximise their tax returns.

- Structuring your assets effectively to ensure tax efficiency and long-term financial benefits.

- Investing in Early Stage Investment Companies (ESICs) to access valuable tax offsets and a capital gains tax discount.

- Using Early Stage Venture Capital Limited Partnerships (ESVCLPs) to take advantage of tax incentives for early-stage investments.

- Leveraging negative gearing to reduce the amount of tax you owe through strategic property and share investments.

- Holding income protection insurance to safeguard your earnings while benefiting from tax deductions.

- Maximising your super contributions to take advantage of concessional tax rates and boost your retirement savings.

- Using a discretionary trust to lower your taxable income by distributing this to eligible family members and beneficiaries.

- Prepaying deductible expenses to bring forward tax deductions and reduce your taxable income before the financial year ends.

Navigating the tax system as a high-income earner can be complex, and understanding tax implications is key to making informed financial decisions. Each strategy has its own benefits depending on your income, investments, and future plans. But which one’s right for you? Well, Liston Newton’s tax minimisation advisors specialise in legally and compliantly reducing taxes for high-income earners.

[free_strategy_session]

Book a free financial strategy session

A 90-minute strategy session gives you a clear plan for your bucket company.

- Get a better understanding of your needs

- We generate a detailed report from your strategy session

- Understand your priorities and next steps

[/free_strategy_session]

What is a high-income earner? and how can they minimise tax?

A high-income earner in Australia is anyone earning $190,001 or more per year. At this level, you are taxed at the highest marginal income tax rate of 45%, plus the 2% Medicare levy. This means for every dollar earned over $190,000, 47 cents goes to tax. The total tax payable, inclusive of the Medicare levy on this income, starts at $55,438, with additional tax applied for every dollar above this threshold. Unlike lower income brackets, high-income earners are subject to additional tax, meaning that without proper tax planning, they may be paying more than necessary.

With such a significant overall tax burden as a high-income individual, you’ll need smart tax planning strategies to legally reduce taxes in Australia, maximise deductions, and optimise your investments. In this blog, we break down five of the most effective tax minimisation strategies to help you retain more of your income and build long-term wealth.

Now, let’s look at the eight ways high earners can maximise their tax return.

Strategy 1: Structure your assets to minimise tax

Tax deductions mean that one must spend money, and therefore deduct that expenditure from their tax payable. This often leads to people buying things unnecessarily just to get a tax deduction.

A more beneficial tax-saving strategy is to focus on building profits and personal wealth, rather than trying to minimise tax via spending.

Understanding tax implications can be tricky; when considering where to hold your investment assets, you need to consider a number of factors:

- Holding investments under a trust structure would give you access to a 50% capital gains discount. This structure will also allow you to distribute profits from your investments to lower-income earning beneficiaries.

- A company structure does not receive a CGT discount, has the advantage of having a capped tax rate at 30%, which could be valuable if the investment is generating significant income each year.

From a tax perspective, choosing the right structure can determine how much personal tax and company tax rate you’ll pay on your income.

Investments to reduce taxable income and grow your wealth

Strategic investments to reduce taxable income include negatively geared property, dividend-paying shares, and superannuation contributions. Property investors can deduct losses from their taxable income, while share investors can benefit from franking credits on Australian dividend stocks. Making additional contributions to superannuation also reduces taxable income, as concessional contributions (up to $30,000 per year) are taxed at a lower rate of 15% instead of your marginal tax rate. Each of these strategies helps lower your tax liability while building wealth over time.

The correct structure depends on your personal circumstances, but should be the first conversation you have around tax minimisation. If you'd like to learn more about how to structure your assets for outstanding savings, contact Liston Newton.

[tip_box]

How to save tax by investing

One of the best ways to save tax by investing is through Early Stage Investment Companies (ESICs) and Early Stage Venture Capital Limited Partnerships (ESVCLPs). These investment options provide tax offsets — ESICs offer a 20% tax offset on your investment, while ESVCLPs provide a 10% tax offset. Eligible ESIC investments have modified capital gains tax (CGT) treatment, under which capital gains on qualifying shares that are continuously held for at least 12 months and less than 10 years may be disregarded – capital losses on shares held less than 10 years must be disregarded. Investing strategically in these options can reduce your taxable income while building wealth.

[/tip_box]

Strategy 2: Invest in Early Stage Investment Companies (ESICs) for tax benefits

Early-stage investment companies (ESICs) are relatively new and can be overlooked as a tax minimisation strategy. In July 2016, concessions were introduced for early-stage investors, otherwise known as ‘Angel Investors’, that included a tax offset and a Capital Gains Tax exemption. These concessions can be generous.

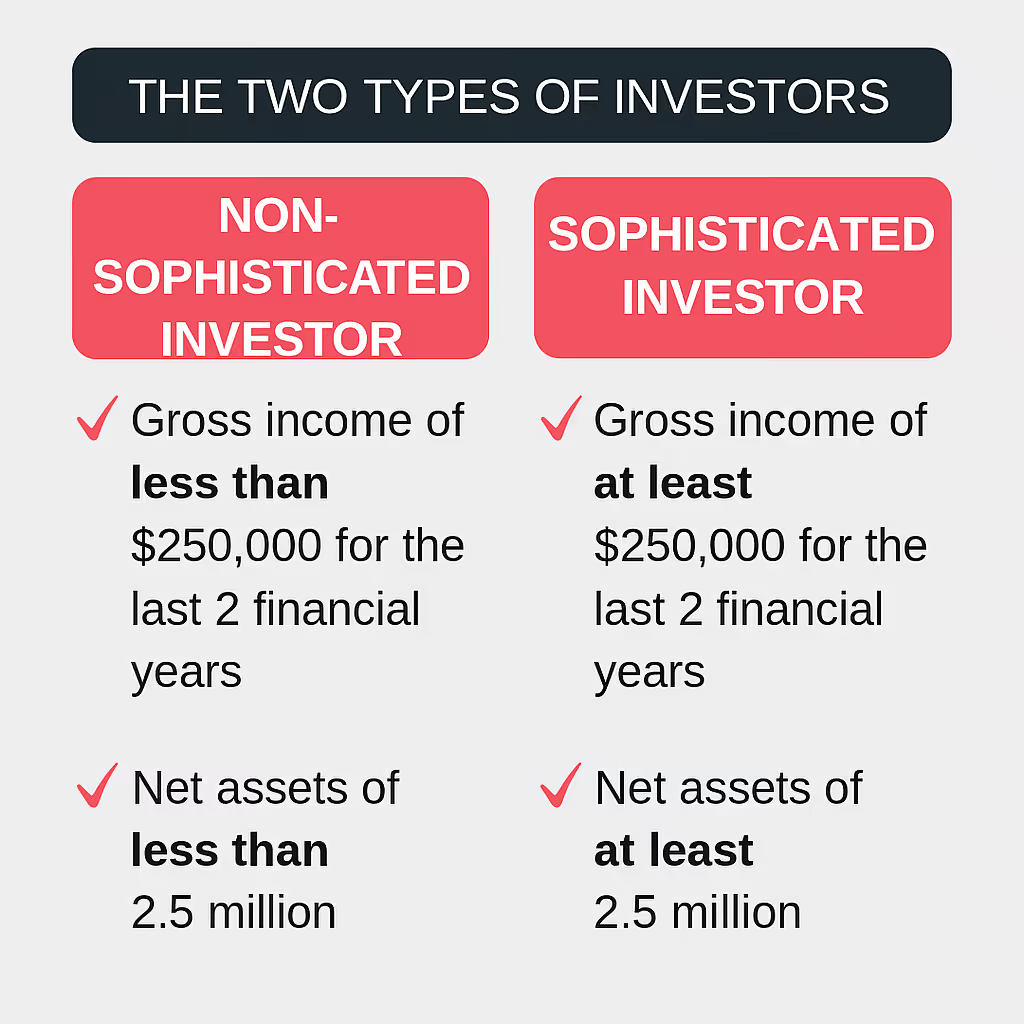

Sophisticated versus non-sophisticated investors

- Sophisticated investors need to have a gross income of at least $250,000 for the last two financial years, and net assets of at least 2.5 million.

- Non-sophisticated investors are anyone that doesn’t qualify for the above. If you are not a sophisticated investor, the maximum amount you can invest in an early stage investment company is $50,000 per year.

Tax offsets

A tax offset is a direct reduction on the amount of tax you need to pay. Let’s look at some tax minimisation examples using tax offsets.

- If you have $100,000 of assessable income for the year, your tax payable would be approximately $26,000.

- A tax offset of $10,000 would reduce your tax payable down to $16,000.

The ESIC concessions allow an investor to claim a 20% tax offset on the amount they have invested in an early stage investment company, making it one of the most effective ways to reduce your tax while investing for growth.

- A sophisticated investor could make a $1 million investment in an early stage investment company and claim a $200,000 tax offset against their tax payable.

- A non-sophisticated investor could invest $50,000 and claim a $10,000 tax offset against their tax payable.

Investments in ESICs are also free from Capital Gains Tax (CGT) for 10 years. If the investment is held for under 10 years, there will be no additional tax when selling the investment. For more details on eligibility and tax benefits, the Australian Taxation Office has defined a few key tax incentives for early-stage investors.

These capital gains tax concessions make ESICs an attractive option for investors looking to maximise tax efficiency.

Strategy 3: Use Early Stage Venture Capital Limited Partnerships (ESVCLPs) to reduce tax

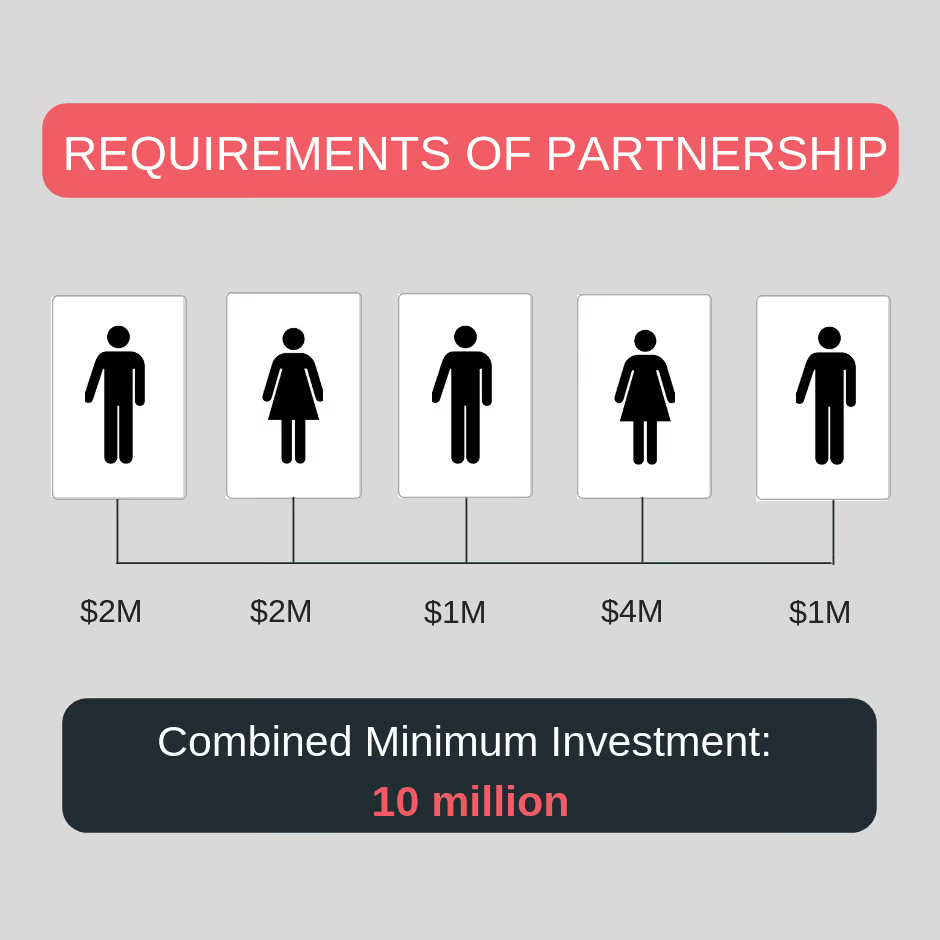

An Early Stage Venture Capital Limited Partnership (ESVGLP) is an investment structure that combines multiple investors into a structure to make investments. It works much the same way as an investment into an early stage investor company.

- All partners have a combined minimum investment of $10 million.

- This type of investment allows a 10% tax offset for the amount of investments made.

If you'd like to learn more about tax minimisation strategies by investing in ESICs or ESVCLP, contact Liston Newton.

Strategy 4: Leverage negative gearing to offset investment losses

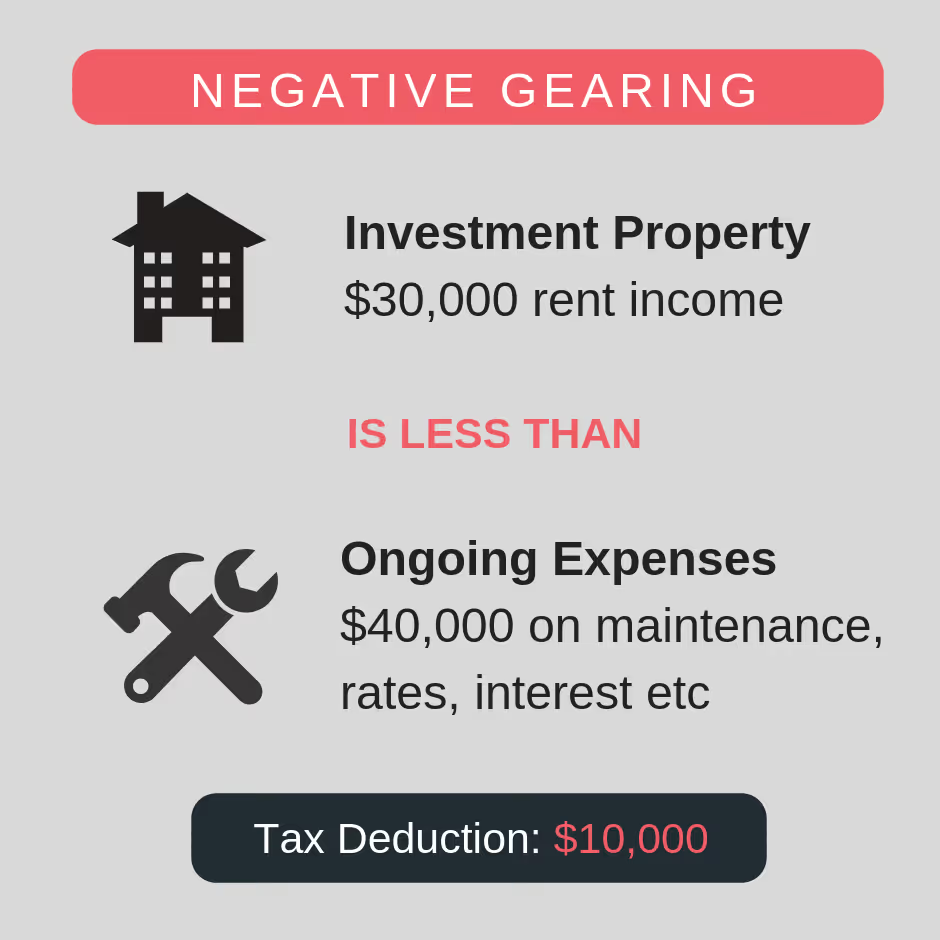

Negative gearing is a common tax-saving scenario, and remains an effective strategy, provided the underlying investment experiences ongoing growth in capital value.

- Negative gearing essentially means that the income you receive from your investment is less than the expenses you paid to hold the investment.’taxable income each year.

Negative gearing works the same way when you borrow to invest in shares. If the dividends on your investment income don’t cover the cost of holding those shares, you are able to claim a deduction for that amount.

This strategy only works well when the underlying asset is increasing in value. For example:

- A good negative gearing strategy may cost you $5,000 per year to hold a property

- The property value must increase by more than the $5,000 each year to justify the cost of the loss.

From a property tax standpoint, negative gearing can also help your overall tax affairs when structured correctly.

Strategy 5: Protect your income while claiming tax deductions

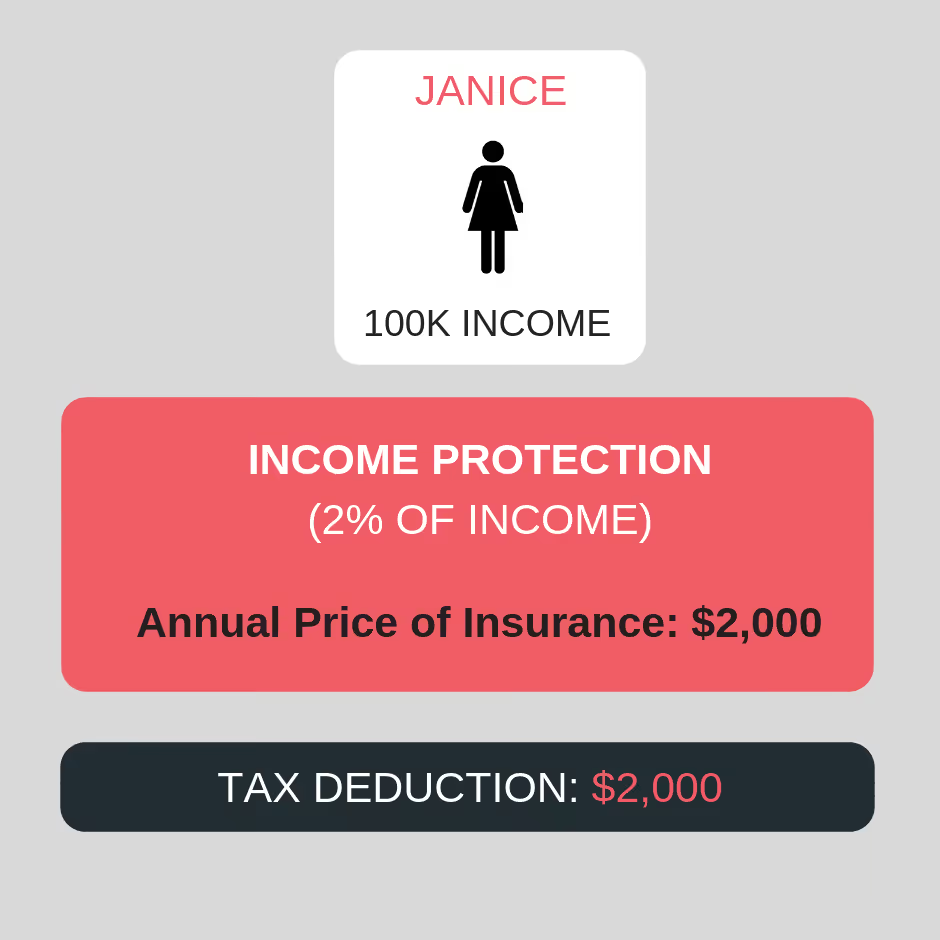

If you have an effective tax planning strategy in place to build wealth over time, then the only thing that may prohibit you from achieving your goal is illness or injury. This is why we strongly advise our clients to acquire income protection. It’s a great way to provide your family with peace of mind.

- If you hold income protection in your own name, you’re able to claim it as a tax deduction.

- Income protection is relatively affordable and on average costs around about 2% of your annual income.

- It should be treated as an essential expense to protect your most valuable asset.

Strategy 6: Maximise super contributions to lower your tax bill

.avif)

Contributing extra to superannuation is one of the most effective ways for high-income earners to reduce taxable income while growing their retirement savings. Superannuation concessional contributions (such as salary sacrifice) are taxed at just 15%, which is significantly lower than the 47% marginal tax rate for incomes over $190,000.

Superannuation contributions are one of the most effective tax planning strategies, especially when it comes to tax planning for retirement.

Here's an example of a super contributions tax minimisation strategy.

Sarah earns $250,000 per year, putting her in the highest tax bracket. If she contributes an extra $20,000 to her superannuation through salary sacrifice, this amount is taxed at 15% instead of her 47% marginal tax rate. This means she saves $6,000 in tax, while also boosting her retirement savings.

To make the most of this strategy, it’s important to understand the following considerations:

- The concessional contributions cap is $30,000 per year, including employer contributions.

- If you earn over $250,000, an additional 15% tax (Division 293 tax) applies to concessional contributions — but even at 30% total tax, it’s still much lower than the 47% marginal tax rate.

- You can carry forward unused concessional cap amounts for up to five years if your super balance is under $500,000, allowing for larger tax deductions in high-income years.

For high-income earners, maximising super contributions is a smart, tax-efficient way to save for a successful retirement while reducing taxable income today.

[tip_box]

Download our guide on preparing for a successful retirement

This guide can help you retire with confidence and make the most of your financial future

Inside you will learn about key strategies and considerations to help you plan a smooth and stress-free retirement:

- How much superannuation you really need

- Transition-to-retirement strategies

- Tax-effective ways to draw down your income

- Estate planning essentials and asset protection

Download it here.

[/tip_box]

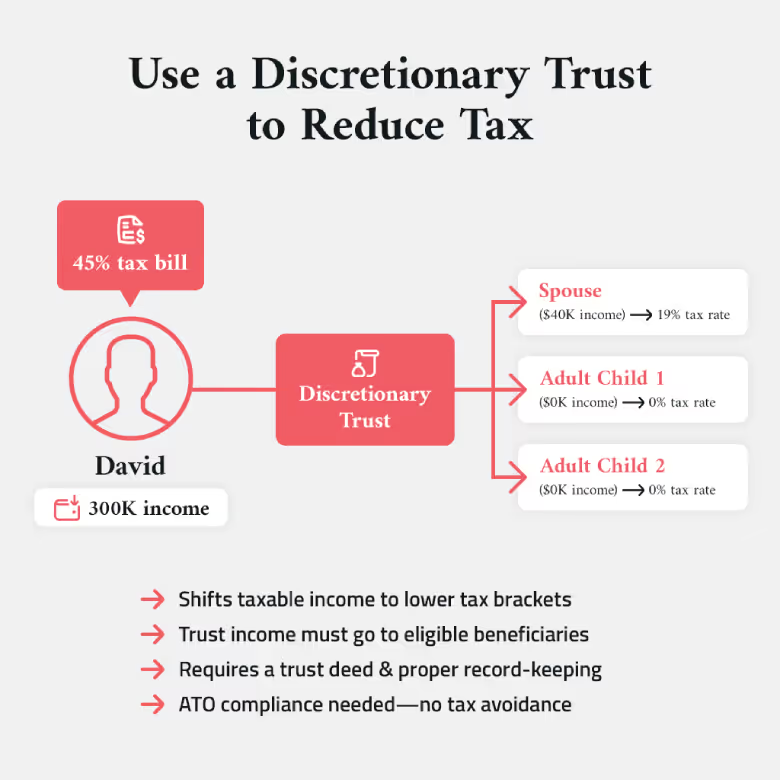

Strategy 7: Distribute income through a discretionary trust

A discretionary trust, also known as a family trust, allows high-income earners to distribute income among family members in lower tax brackets to reduce overall tax liability. Instead of receiving all investment income personally and paying up to 47% in tax, you can allocate income to family members who pay lower tax rates, reducing the total tax paid by the household.

Let’s take a look at an example.

David is a business owner earning $300,000 per year. He sets up a discretionary trust that holds $100,000 worth of investments. Instead of receiving all the investment income himself, he distributes $20,000 each to his spouse and two adult children, who are in lower tax brackets.

- His spouse, earning $40,000 per year, pays only 19% tax on the distributed income.

- His children, who are university students with no other income, pay no tax on their share (as it falls within the tax-free threshold).

- By spreading the income, David reduces his tax liability while keeping wealth within the family.

Before using a discretionary trust, it’s essential to consider the following to ensure compliance and effectively distribute taxable income to beneficiaries:

- You can only distribute trust income to beneficiaries.

- Trusts cannot be used purely for tax avoidance — there must be a genuine purpose.

- A trust deed and proper record-keeping are required to ensure compliance with the ATO.

- By shifting taxable income to family members in lower marginal tax rates, high-income earners can legally reduce their overall tax obligations.

For high-income earners with investment income or business profits, a discretionary trust provides flexibility and significant tax advantages when structured correctly.

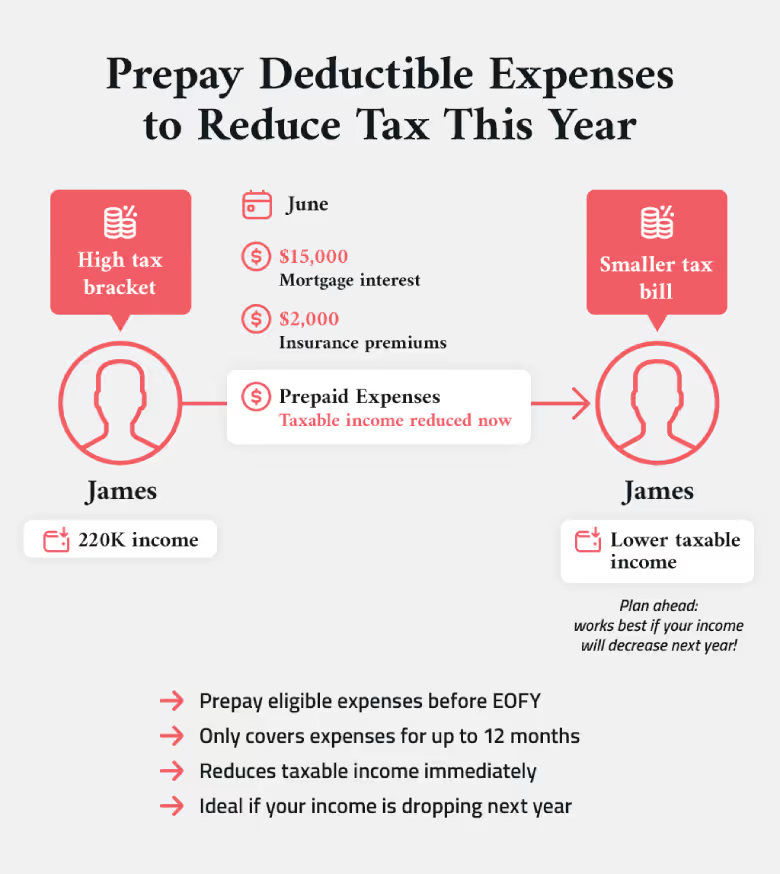

Strategy 8: Prepay deductible expenses to reduce this year’s tax

High-income earners can bring forward tax deductions by prepaying deductible expenses before the end of the financial year. This strategy allows you to reduce taxable income in the current year, which is especially beneficial if you expect your income to drop in the following year.

Let’s see how this works in action.

James earns $220,000 per year and owns an investment property. His mortgage interest, council rates, and maintenance costs total $30,000 annually. In June, he decides to prepay 12 months' worth of interest payments ($15,000) and $2,000 in insurance premiums, reducing his taxable income for the current financial year.

By bringing these expenses forward, James:

- Reduces his taxable income immediately, lowering his current tax liability.

- Takes advantage of deductions while he’s still in the high-income tax bracket, rather than the following year when he expects his income to be lower.

- Improves his cash flow planning, knowing that these costs are already covered.

Before prepaying expenses, keep in mind the following:

- Only certain tax deductible expenses qualify for prepayments, such as loan interest, professional memberships, and business-related costs.

- The 12-month rule applies, meaning prepayments generally must cover a period no longer than 12 months.

- Prepaying works best when your income is expected to decrease in the following financial year, ensuring you maximise deductions while in a higher tax bracket.

For high-income earners, prepaying deductible expenses is a simple yet effective way to strategically lower tax obligations while keeping finances structured.

[tip_box]

Download our guide to tax minimisation strategies

This guide can help you legally reduce your tax bill and retain more of your income

Inside, you will learn about smart strategies that high-income earners can use to structure their finances more effectively:

- Income splitting and family trust benefits

- Superannuation contribution strategies

- Offsetting investment losses and deductions

- Tax-effective investment options

- Common pitfalls and how to avoid ATO scrutiny

Download it here.

[/tip_box]