Buying commercial property with super means purchasing business real property through a self-managed super fund (SMSF), so the fund owns the asset and receives rental income and capital growth within the superannuation environment.

For many Australian business owners, this strategy allows you to invest in commercial property, lease it to your business, and build long-term wealth inside your super.

An SMSF commercial property investment can provide control over your investment, but it must comply with strict SMSF property purchase rules. The property must meet the sole purpose test, be held in the name of the SMSF, and align with the fund’s investment strategy.

If you’re establishing a fund specifically for property investment, it’s important to obtain SMSF set up advice before purchasing commercial property through your super.

[smsf_awards][/smsf_awards]

Steps to buy commercial property through your SMSF:

- Review your SMSF investment strategy: Trustees must confirm the fund allows investment in commercial property through your SMSF and that the purchase suits members’ long-term retirement objectives.

- Check the SMSF trust deed: Your trust deed must permit SMSF borrowing or property investment before you purchase property using super.

- Confirm funding method: An SMSF can acquire commercial property via:

- a cash purchase

- borrowing through your SMSF using a Limited Recourse Borrowing Arrangement (LRBA)

- Establish the correct purchase structure: If borrowing is involved, the property is held in a bare trust within your SMSF until the loan is repaid.

- Complete the property purchase: The SMSF trustee signs the contract and the property is held on behalf of the SMSF.

- Lease the property at market value: Commercial property can be leased to a related business, provided rent is paid directly to your SMSF at market rates.

When structured correctly, an SMSF buys commercial property as part of a diversified SMSF investment strategy designed to build long-term retirement assets.

Pros and cons of buying commercial property through an SMSF

Like any commercial property investment, using super to invest in property has both advantages and risks.

Pros of SMSF commercial property investment

- SMSF members can choose and manage the commercial property investment directly.

- Rental income paid to the SMSF is taxed at the concessional super rate.

- You can purchase your business premises and lease it back to your company.

- Commercial property held within super can generate long-term capital growth within the superannuation system.

- The SMSF structure helps protect your assets under superannuation law.

Cons of buying property in an SMSF

- Limited liquidity is a risk because large property investments can reduce the cash amount in your SMSF.

- Strict compliance rules apply because SMSF regulations require careful documentation and ongoing compliance.

- Higher setup costs are involved due to legal, accounting, and audit fees.

- Borrowing restrictions are imposed as lenders limit how much a SMSF can borrow for a property loan.

- Market risk exists because commercial properties can experience vacancy periods.

Because of these factors, consider buying commercial property carefully as part of a broader retirement strategy.

Who should buy commercial property through an SMSF?

Not every investor is suited to property in an SMSF, particularly if they are still building their retirement strategy or learning how superannuation works for business owners. However, for some, it can be a powerful long-term strategy.

Typically, SMSF commercial property investment works best for:

- Established business owners who want to purchase their business premises in their SMSF

- Individuals with a substantial amount in their super

- Investors comfortable managing SMSF compliance and reporting

- People seeking control over their super investments

- Members with a long investment timeframe

For example, many business owners purchase commercial property through a self-managed super fund and lease the property back to their operating company. The rent is then paid to the SMSF, building retirement wealth over time.

Before investing, trustees must ensure the purchase supports the SMSF investment strategy and complies with ATO SMSF regulations.

How to use your SMSF to invest in commercial property

Using super to invest in property requires careful planning and compliance with SMSF regulations.

How the investment process works

- Confirm SMSF eligibility: Ensure the fund allows commercial property investment.

- Identify a suitable investment property: The property must meet the definition of business real property.

- Arrange financing if required: Where borrowing is needed to acquire the asset, the SMSF must establish a Limited Resource Borrowing Arrangement (LRBA) supported by an appropriate bare trust structure.

- Set up the ownership structure: The SMSF acquires commercial property via the correct trust arrangement.

- Complete the property settlement: The property is held in the name of the SMSF.

- Lease the property: The SMSF can rent the property to someone who is not related to the fund or to a related business, provided the rent is based on the fair market rent.

When structured properly, the commercial property through a self-managed super fund becomes part of the fund’s long-term investment portfolio.

[tip_box]

Download our guide to a financially successful retirement

This guide can help you make confident financial decisions as you plan for retirement

Inside you’ll find key insights and practical advice to help you retire on your terms—with enough savings to support the lifestyle you want.

- How much superannuation is enough to retire comfortably

- Tax-effective strategies to boost your retirement savings

- Transition-to-retirement strategies explained

- When and how to access your super

- Investment tips for income and stability in retirement

[/tip_box]

How buying commercial property with super works

Understanding how investing in commercial property really works within an SMSF helps trustees avoid compliance issues.

The key principle is that the property is held by the SMSF, not by the individual members.

Typical SMSF property purchase structure

- The SMSF trustee identifies a commercial property investment.

- The SMSF signs the contract to purchase commercial property.

- If borrowing is used, a bare trust holds the property until the loan is repaid.

- Rental income flows into the SMSF bank account.

- Property expenses such as maintenance, insurance and rates are paid by the SMSF.

The arrangement ensures that commercial property with super remains compliant with superannuation laws and contributes to the retirement savings of SMSF members.

Your SMSF commercial property purchase options

When considering SMSF property purchase options, trustees typically choose between a cash purchase or borrowing through an SMSF using a Limited Recourse Borrowing Arrangement (LRBA). The right option depends on the amount in your super, risk tolerance, and the SMSF investment strategy.

[table][thead][tr][th]Purchase option[/th][th]How the structure works[/th][th]Key considerations[/th][/tr][/thead][tbody][tr][td]Commercial property via a cash purchase[/td][td]The SMSF uses the available cash amount in the fund to purchase commercial property directly. The property is held in the name of the SMSF and rental income is paid directly to the fund.[/td][td]Simpler structure, no property loan, and lower compliance complexity. However, it requires a large cash balance in the SMSF.[/td][/tr][tr][td]Borrowing through your SMSF (LRBA)[/td][td]The SMSF acquires commercial property indirectly via a Limited Recourse Borrowing Arrangement. A lender provides the property loan and the asset is held in a bare trust until the loan is repaid.[/td][td]Allows the fund to invest in commercial property with super sooner, but includes stricter lending rules and higher setup costs.[/td][/tr][tr][td]Related-party business premises purchase[/td][td]The SMSF purchases business real property and leases the property to the member’s business at market rent, allowing rent to flow into the SMSF.[/td][td]Common for business owners wanting to purchase their business premises while building retirement assets within their SMSF.[/td][/tr][/tbody][/table]

Key considerations when buying commercial property through your SMSF

Before purchasing a commercial property through an SMSF, trustees should assess several important factors.

Important considerations

- Liquidity: It is crucial to ensure the SMSF retains enough readily available cash. This cash reserve is necessary to cover ongoing property expenses, such as maintenance and rates.

- Diversification: The fund manager must actively avoid concentrating the fund's total value in a single investment property. This strategy helps mitigate risk by spreading the fund's capital across different assets.

- Valuation requirements: SMSFs are legally obligated to conduct regular property valuations to ensure all assets are accurately reported at their current market value.

These valuation requirements are explicitly outlined in the Australian Taxation Office’s (ATO) guide concerning the valuation of SMSF assets. - Tenant risk: Fund managers need to carefully consider and manage the inherent risks associated with tenants, including potential vacancy periods. They must also assess and ensure the long-term stability and reliability of the current tenants.

- Compliance with SMSF regulations: The investment property purchased by the fund must comply with all relevant SMSF regulations. Specifically, the property must satisfy the "sole purpose test," meaning it is held purely for providing retirement benefits to members.

The decision to purchase property through a self-managed super fund should always align with the long-term financial goals of SMSF members.

Do SMSFs pay stamp duty on commercial property?

Yes. When purchasing commercial property through an SMSF, stamp duty generally applies in the same way as other property purchases.

The amount payable depends on the state or territory where the property is located.

For example, State Revenue Office rules determine stamp duty rates and exemptions. In most cases:

- SMSFs must pay stamp duty on property purchase

- concessions may apply in certain trust restructuring scenarios

- the SMSF trustee must ensure the property is registered in the name of the SMSF

Because stamp duty can be a significant cost, it should be included in the overall SMSF property purchase planning.

Understanding SMSF borrowing rules and LRBAs

Business owners can use their SMSF to borrow money for buying property, but they must adhere to stringent regulations. Some trustees use borrowing when setting up a self-managed super so they can purchase the property and hold property in their SMSF as part of their long-term investment strategy.

In most cases, this borrowing structure uses a Limited Recourse Borrowing Arrangement (LRBA), which is the main way an SMSF can legally borrow to invest in commercial property with your super.

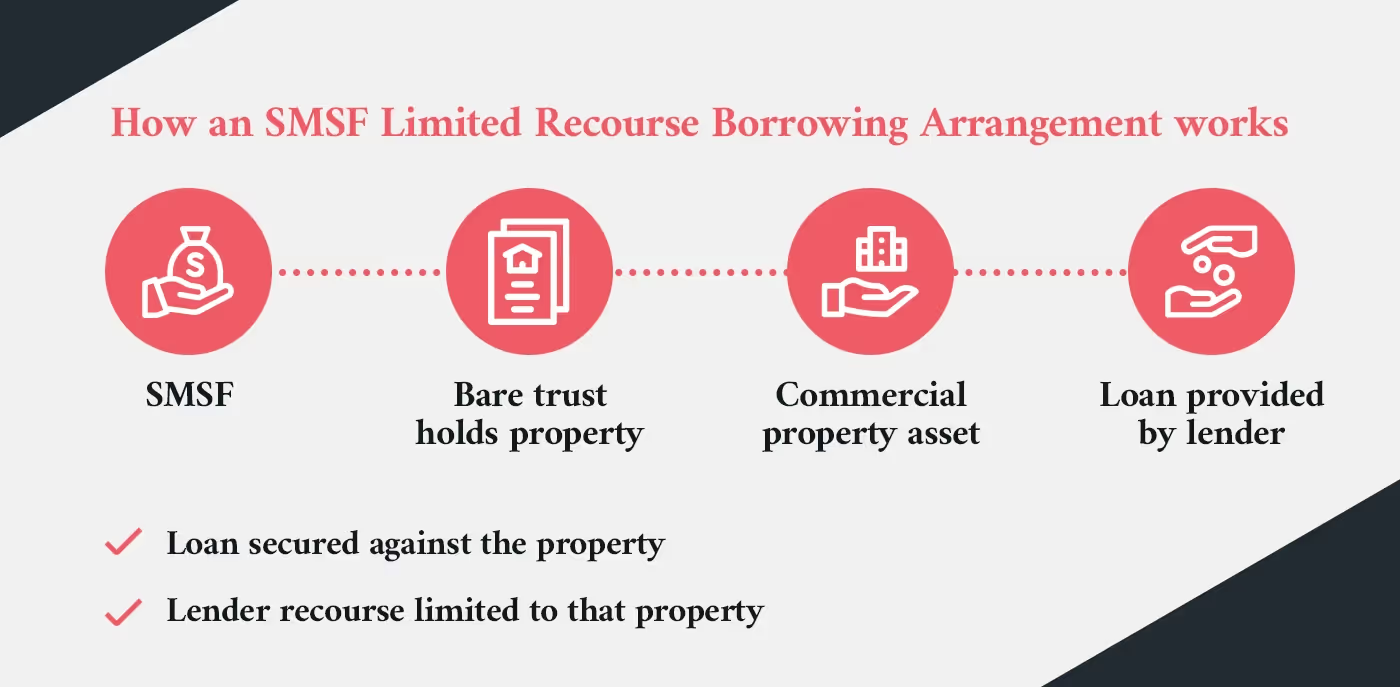

What is an LRBA?

Borrowing to buy property through super is allowed under strict conditions set by the ATO, particularly when using a Limited Recourse Borrowing Arrangement (LRBA). According to the ATO, LRBAs allow an SMSF to borrow for a single asset while limiting the lender’s recourse to that asset only (ATO).

Key features include:

- the loan is secured against a single property asset

- the property is held in a bare trust within your SMSF

- the lender’s recourse is limited to that property

How much can a SMSF borrow to buy property?

Most lenders apply conservative lending criteria for SMSF property loans.

Common requirements include:

- a deposit of 30–40% of the property value

- sufficient rental income to service the loan

- a strong SMSF cash balance

Because borrowing rules are complex, professional SMSF experts explain the risks and benefits before proceeding.

What fees and costs apply when buying commercial property through an SMSF?

Before completing a purchase, trustees should understand the SMSF property purchase fees and the ongoing costs of holding property in an SMSF. These expenses must be paid by the SMSF, so the fund needs sufficient liquidity.

[table][thead][tr][th]Cost category[/th][th]Typical fees involved[/th][th]Why it matters for your SMSF[/th][/tr][/thead][tbody][tr][td]Upfront property purchase costs[/td][td]Stamp duty, legal fees, property due diligence, conveyancing and trust setup costs.[/td][td]These fees apply when the SMSF acquires commercial property and can significantly increase the total purchase cost.[/td][/tr][tr][td]Borrowing and lender costs[/td][td]Loan establishment fees, lender legal costs, valuation fees and ongoing property loan interest.[/td][td]Applies when borrowing through your SMSF using an LRBA structure.[/td][/tr][tr][td]Ongoing SMSF and property expenses[/td][td]Annual SMSF audit, accounting fees, property management, insurance, maintenance and council rates.[/td][td]Trustees must ensure the fund retains enough cash to meet ongoing property expenses and SMSF compliance obligations.[/td][/tr][/tbody][/table]

SMSF property purchase compliance checklist

Before completing a SMSF property purchase, trustees should confirm the following:

- The investment strategy allows commercial property investment

- The property meets the definition of business real property

- The purchase complies with SMSF regulations

- Any borrowing structure uses a compliant LRBA

- Rent is paid at market value

- The property is held in the name of the SMSF or bare trust

- All transactions occur at arm’s length

- The fund retains sufficient liquidity for expenses

Maintaining compliance with SMSF regulations is essential to protect the tax advantages of the superannuation system.

Get expert SMSF advice before buying commercial property

Buying commercial property with super can be a powerful strategy for building long-term wealth and securing business premises, but it requires careful structuring and compliance.

Professional advice from experienced SMSF accountants helps ensure:

- The investment fits your SMSF strategy

- Borrowing structures comply with SMSF borrowing rules

- Property transactions meet ATO compliance requirements

At Liston Newton, our advisory team helps business owners understand how commercial property through your SMSF can form part of a broader financial plan.

If you are considering using super to invest in property, speak with our team for strategic SMSF advice and guidance on property structuring.

Book a free strategy session with our advisory team to discuss your SMSF property investment options.

[free_strategy_session]

Free 90-minute strategy session

Thinking about buying commercial property with super? Speak with our advisory team before making a decision.

• Understand SMSF property purchase rules and borrowing limits

• See if commercial property in your SMSF fits your strategy

• Get clear next steps for structuring the purchase correctly

Book your free strategy session

[/free_strategy_session]