Selling a business can trigger significant tax on the sale of a business, particularly through capital gains tax (CGT). However, with proper planning, business owners can legally reduce their tax liability and retain more of the value they’ve built.

Several strategies may help minimise the tax impact when selling a business.

Key steps to reduce tax when selling a business:

- Review your business structure early: The tax outcome of a business sale can vary depending on whether the business operates as a sole trader, company, or trust. Reviewing your structure well before a sale can help ensure the most tax-effective outcome.

- Understand how capital gains tax applies: In many cases, selling a business triggers a capital gains tax (CGT) event. The gain is generally calculated by subtracting the asset’s cost base from the sale price.

- Determine eligibility for small business CGT concessions: Eligible businesses may access several small business CGT concessions that can significantly reduce or even eliminate capital gains tax.

- Consider the timing of the sale: The financial year in which the sale occurs can affect your overall tax liability and marginal tax rate.

- Seek advice from a tax professional early: Strategic tax planning for a business sale can identify opportunities to reduce the tax payable before the transaction takes place.

Business owners planning to sell should seek advice early to ensure the sale structure supports the best possible tax outcome. Our team can assist with tax planning and structuring the sale of your business.

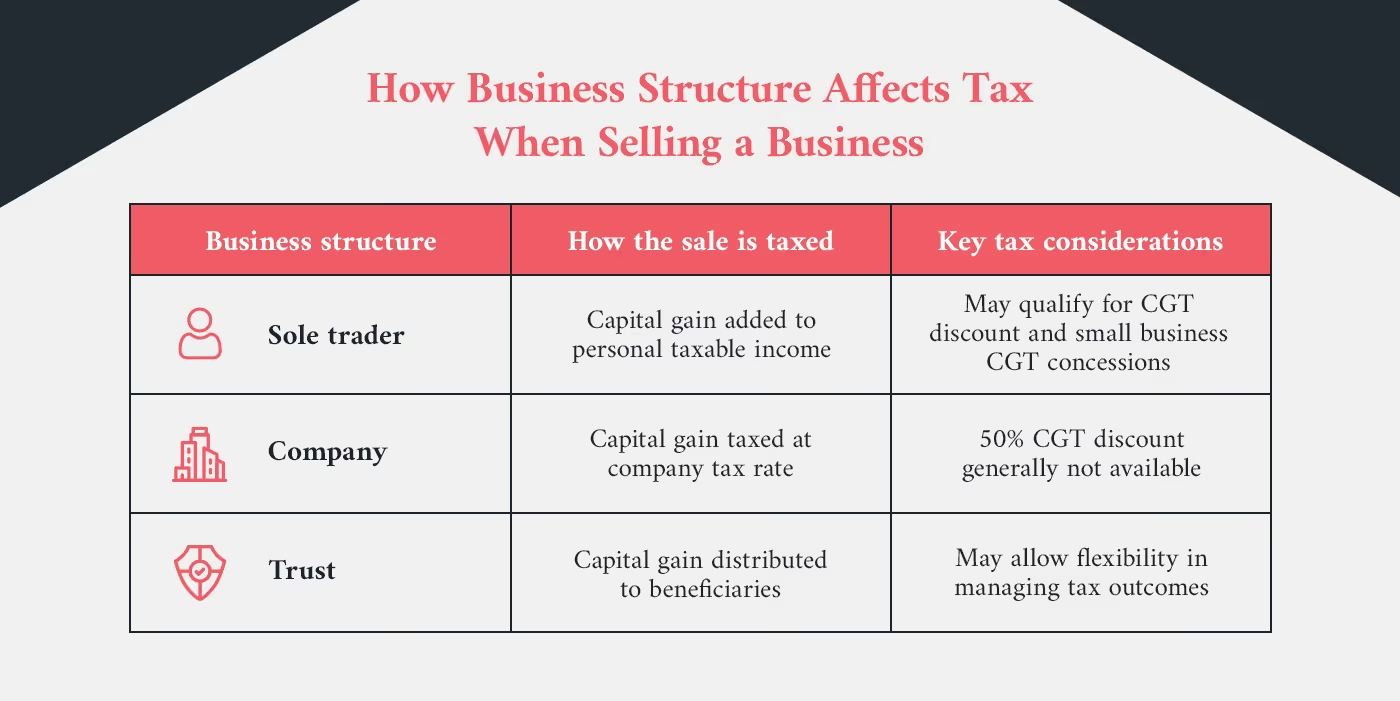

How tax rates apply when selling a business (sole trader, company, or trust)

The tax on selling a business can vary significantly depending on the business's structure. Whether the business operates as a sole trader, company, or trust will influence how the gain from the sale is taxed and the overall tax outcome.

Understanding how tax applies to each structure is an important part of tax planning for a business sale.

Sole trader

When a sole trader sells a business asset, the profit is generally treated as a capital gain and forms part of the owner’s taxable income for that financial year.

The capital gain is taxed at the individual’s marginal tax rate, although eligible business owners may be able to access the CGT discount and small business CGT concessions, which can significantly reduce the tax payable.

Company

If a company sells business assets, the capital gain is usually taxed at the corporate tax rate rather than the owner’s personal tax rate.

Companies generally do not qualify for the 50% CGT discount, but other concessions may still apply depending on the circumstances. In some cases, business owners may sell the company's shares, which can result in different tax outcomes.

Trust

When a business operates through a trust, any capital gains from the sale of business assets are typically distributed to the trust's beneficiaries.

The beneficiaries then include their share of the capital gain in their individual tax returns, which may provide greater flexibility in managing the overall tax outcome.

Choosing the right business structure can significantly impact the tax payable when selling a business. If you’re unsure how your structure affects a future sale, it’s worth reviewing your options early.

Understanding Capital Gains Tax (CGT) and how it applies to business sales

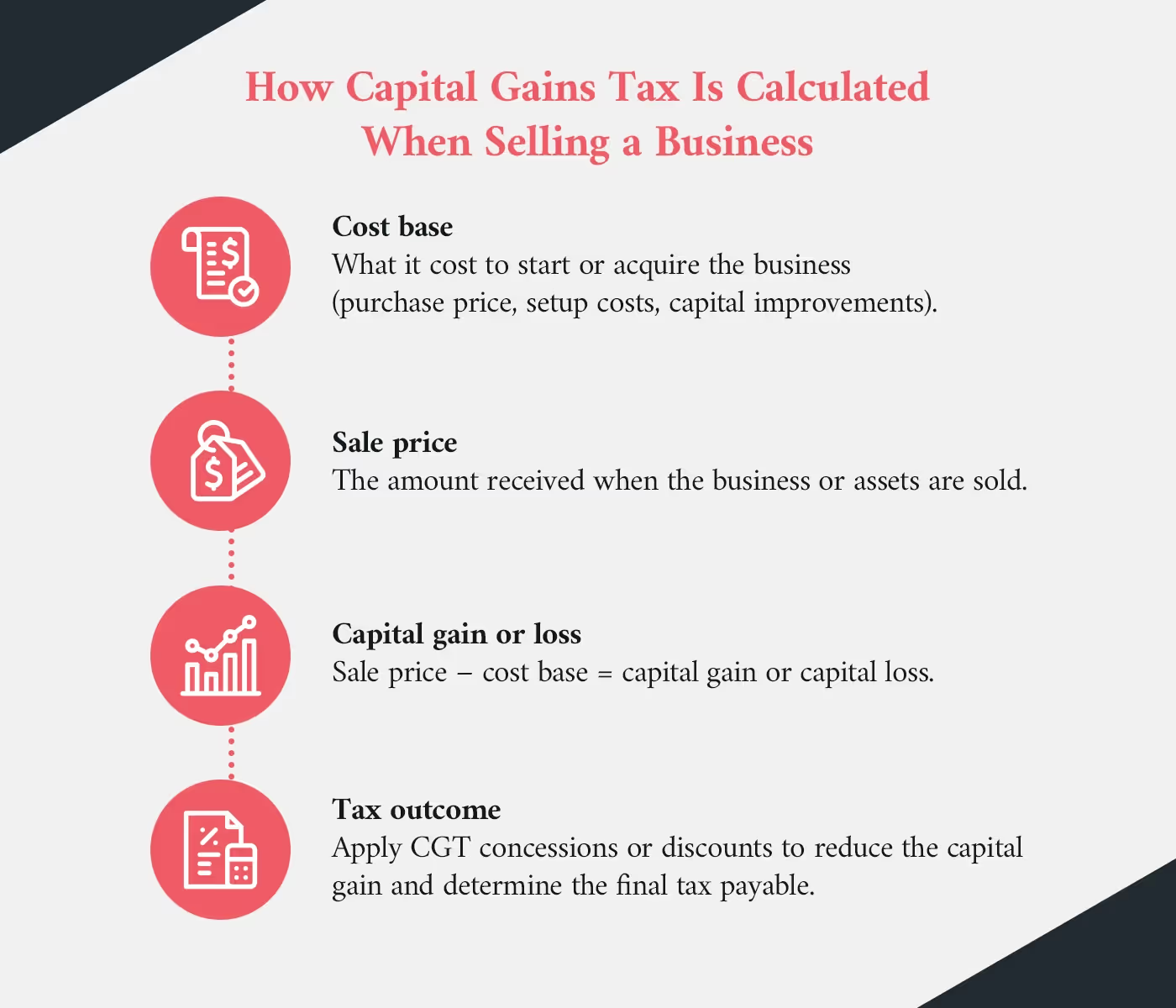

Regardless of your business structure, selling your business is generally treated as selling an asset. When this happens, it can trigger capital gains tax (CGT).

A capital gain refers to the profit made when an asset is sold for more than its cost base. In the context of a business sale, this means that if the sale price of your business is higher than what it originally cost you to establish or acquire it, the difference is considered a capital gain.

This triggers a CGT event, meaning the gain may be subject to capital gains tax on the sale of the business.

The amount of CGT payable when selling a business can depend on several factors, including:

- The cost base of the business: This is the amount it costs you to start or acquire the business. If you purchased the business, the purchase price usually forms the cost base. If you built the business yourself, the cost base may be very low.

- The sale price of the business: The higher the sale price relative to the cost base, the larger the potential capital gain.

- Your business structure: Whether the business operates as a sole trader, company, or trust can influence how the capital gain is taxed.

- Eligibility for CGT concessions: Certain small business CGT concessions may reduce or even eliminate the capital gains tax payable.

- Your income in the financial year of the sale: For individuals and beneficiaries, the capital gain is often included in taxable income, which means the tax payable may depend on the marginal tax rate for that year.

Example

John started his marketing business from scratch and has grown it successfully over several years. He now earns an annual salary of $200,000, placing him in the top marginal tax bracket of 47%.

John decides to sell his business to an interested buyer for $500,000.

Because he started the business himself, his cost base is effectively $0. This means the entire sale price of $500,000 represents a gross capital gain, before any discounts, concessions, or exemptions are applied.

If this capital gain is added to John’s personal income of $200,000, a significant portion of the gain could be taxed at his top marginal tax rate of 47%, potentially creating a substantial capital gains tax liability.

This example highlights why tax planning before selling a business is essential. With the right strategy and access to available concessions, it may be possible to significantly reduce the tax payable on the sale.

Key CGT concessions to reduce tax when selling your business

For eligible business owners, the small business CGT concessions can significantly reduce capital gains tax when selling a business. These concessions apply to certain active business assets and, depending on eligibility, may reduce or defer the capital gain arising from a business sale.

Eligibility is determined by criteria set by the Australian Taxation Office (ATO), including ownership requirements, business use of the asset, and business size thresholds.

Several concessions may apply when calculating capital gains tax on the sale of a business.

15-year exemption

The 15-year exemption allows an eligible business owner to disregard the entire capital gain from the sale of a qualifying business asset.

To access this concession, the asset must generally have been owned for at least 15 continuous years, and additional conditions must be satisfied at the time of sale. This typically includes the business owner being aged 55 or older and retiring, or being permanently incapacitated.

Where the exemption applies, the capital gain can be completely disregarded for tax purposes, meaning no capital gains tax is payable on that portion of the sale.

50% active asset reduction

The 50% active asset reduction allows eligible business owners to reduce the capital gain on an active business asset by 50% before calculating the remaining tax payable.

Active assets are generally those used in the day-to-day operations of the business, such as business premises, equipment, or business goodwill.

This concession may apply alongside other CGT concessions and can substantially reduce the capital gains tax liability when selling a business.

Retirement exemption

The retirement exemption allows eligible business owners to disregard up to $500,000 of capital gains from the sale of active business assets over their lifetime.

If the business owner is under 55 years of age, the exempt amount must generally be contributed to a complying superannuation fund. If the individual is 55 or older, the amount can usually be received directly without contributing it to superannuation.

This concession can be used independently or in combination with other CGT concessions, depending on eligibility.

Small business rollover

The small business rollover allows eligible taxpayers to defer capital gains on the sale of an active business asset.

Instead of paying capital gains tax immediately, the gain can be rolled over into a replacement business asset acquired within a specified timeframe. This defers the CGT liability until the replacement asset is later sold or another CGT event occurs.

Access to these concessions often depends on meeting specific eligibility thresholds, including the $6 million net asset value test or the small business entity turnover test. These tests help determine whether the small business CGT concessions can be applied to reduce the capital gain from the sale of business assets.

A CGT review and early tax planning can significantly influence the capital gains tax outcome when selling a business. Liston Newton works with business owners to assess eligibility for CGT concessions and structure business sales in a more tax-effective way.

[tip_box]

Download our guide to tax-effective business sales

This guide can save you significant amounts of money when selling your business

Inside you will learn about information that will help you keep more of the sale price in your pocket

- CGT concessions for small businesses

- The difference between a share sale and an asset sale

- What does the $6 million net asset test include?

- What is a scrip for scrip rollover?

- How to invest after a business sale

Download it here.

[/tip_box]

Tax-effective strategies for company business sales (asset vs share sale)

When selling a company, the transaction is typically structured as either an asset sale or a share sale. The structure chosen can influence how the capital gain or loss is calculated and ultimately affect the tax you pay on the sale.

[table]

[thead]

[tr]

[th]Sale structure[/th]

[th]How the transaction works[/th]

[th]Potential tax implications[/th]

[/tr]

[/thead]

[tbody]

[tr]

[td]Asset sale[/td]

[td]The company sells individual business assets, such as equipment, intellectual property, or goodwill.[/td]

[td]Each sale of an asset may trigger a capital gain or loss. If the asset sells for more than its cost base, the company may make a capital gain and pay tax on that amount as part of its income tax obligations.[/td]

[/tr]

[tr]

[td]Share sale[/td]

[td]The buyer purchases the company’s shares rather than the individual assets.[/td]

[td]The shareholder sells their ownership interest directly. If the shares have been held for more than 12 months, the seller may qualify for the CGT discount, which can help reduce your capital gain and potentially lower the tax bill.</td>

[/tr]

[/tbody]

[/table]

Choosing the right structure can influence how gains are calculated and which strategies to reduce CGT may be available. In some situations, gains may also be offset against a capital loss, helping reduce the amount of tax payable.

Why early planning is crucial for a tax-effective business sale

Preparing for a business exit early can help small business owners understand the potential tax impact of selling assets and identify opportunities to reduce capital gains tax before the transaction occurs.

Checklist for preparing a tax-effective business sale:

- Review your business structure: The structure of the business can influence how a capital gain or loss is calculated and the rate of tax you pay.

- Assess eligibility for CGT concessions: Some concessions may reduce or even eliminate CGT, helping to reduce your capital gains tax on the sale.

- Review ownership of assets and records: Establishing the cost base, including any capital improvements, helps determine whether you will make a capital gain and how much of the gain may be taxable.

- Consider the timing of the sale: The financial year in which the transaction occurs can affect taxable income, the income tax return, and the tax bill for that year.

- Review gains and losses: In some cases, it may be possible to use capital losses to offset gains, helping to reduce the amount of tax you pay.

For further guidance on financial planning and growth strategies, seek professional advice to maximise the value and tax effectiveness of selling your business.

Next steps for a tax-effective business sale

Selling a business can trigger a capital gain, which may increase the tax you pay in the financial year of the transaction. Understanding how capital gains tax on selling a business works can help business owners identify ways to reduce CGT and structure the transaction more effectively.

A CGT review can help clarify how the capital gain or loss will be calculated, whether existing capital losses may offset gains, and whether concessions could reduce your capital gains tax or reduce the amount payable.

As part of tax planning, business owners often review:

- the sale of assets within the business

- the portion of the capital gain that may be taxable

- whether concessions may help reduce or even eliminate CGT

- the potential impact on income tax and the overall tax bill

For businesses preparing for an exit, reviewing these factors early can help ensure the sale is structured to help you reduce your tax and achieve a lower tax outcome.

As part of this process, Liston Newton works with business owners to review potential CGT implications and support informed decision-making around business sales. Contact Liston Newton today to ensure you're fully prepared for your business sale.

[free_strategy_session]

Planning to sell your business? Book a free 90-minute strategy session.

In this session with Liston Newton, you’ll gain clarity on:

- How capital gains tax may apply to your business sale

- Whether you may qualify for small business CGT concessions

- Practical tax planning strategies to reduce the tax impact of a sale

- Key steps to help structure your exit in a more tax-effective way

A focused 90-minute strategy session designed to help you prepare for a smarter business exit.

[/free_strategy_session]