Capital gains tax (CGT) can significantly reduce the profit you keep when selling a property. However, the Australian Taxation Office (ATO) allows certain exemptions that may reduce or eliminate the tax you pay.

One of the most valuable strategies is the six-year rule for capital gains tax, which forms part of the main residence exemption. This rule allows homeowners to move out of their property, rent it out, and still treat it as their main residence for CGT purposes for a limited period. When applied correctly, the rule can reduce capital gains tax on property rented out, particularly when a property increases in value over time.

At Liston Newton, our tax advisors work with business owners and property investors to structure their finances to legally reduce CGT and support long-term wealth planning. In this guide, we explain how the main residence exemption and the six-year rule work, when the ATO allows you to treat a property as your main residence, and what this means for your capital gains tax obligations when selling property.

To help clarify the concept, watch the short video below where our team explains how the 6-year rule works and how it can affect capital gains tax on property.

What is the 6-year rule for capital gains tax?

The capital gains tax 6 year rule allows a property that was previously your main residence to continue receiving a temporary CGT exemption after you move out.

Under Australian Taxation Office (ATO) rules, this provision sits within the main residence exemption and is often called the absence rule. It allows homeowners to move out of their property and still treat it as their main residence for capital gains tax purposes for a limited time.

If the property is rented out, the exemption can generally apply for up to six years under the ATO’s absence rule for treating a former home as a main residence. During this period, you may not have to pay capital gains tax on the property if a CGT event occurs, such as when the property is sold.

If you move back into the property and re-establish it as your main residence, the six-year period can reset, allowing the exemption to apply again in the future.

Because the rule interacts with the ATO’s absence rule and CGT reporting requirements, it is important to understand how the exemption applies before selling or renting out a property.

How the ATO defines your main residence for CGT purposes

To claim the main residence exemption, the Australian Taxation Office (ATO) must recognise the property as your principal place of residence (PPOR) based on the ATO eligibility criteria for the main residence exemption. This determination affects whether the property may qualify for a capital gains tax (CGT) exemption, which can reduce your tax liability when a property is sold.

The ATO does not rely on a single test to determine whether a property is your main residence. Instead, it considers several indicators to assess whether the property genuinely functions as your principal place of residence during that time.

Common factors the ATO reviews include:

- You and your family live in the property and keep personal belongings there

- The property is used as your primary residential mailing address

- You are registered on the electoral roll at that address

- Utilities such as electricity, gas or internet are connected in your name

These factors help the ATO determine whether the property was your main residence during that time, which affects whether a future sale may be exempt from CGT or reduce the net capital gain reported in your annual income tax return.

You also generally cannot treat another property as your main residence at the same time, unless specific exceptions apply under Australian tax rules.

If the circumstances are unclear, professional advice can help ensure the property qualifies for the main residence exemption and that any capital gain is reported correctly for income tax purposes.

[tip_box]

Download our tax minimisation guide

This guide could help reduce your tax bill and improve your financial position

Inside you’ll find practical strategies and essential information to help you minimise tax legally and effectively—whether you're an individual, investor or business owner.

- Understanding legitimate tax deductions and offsets

- How to structure your business to reduce tax

- The benefits of super contributions and trust structures

- Tax-effective investment strategies

- Common tax traps and how to avoid them

[/tip_box]

How the 6-year rule works when renting out your property

The CGT 6 year rule allows you to move out of a home and still treat it as your main residence for capital gains tax purposes for a limited time. In practical terms, the rule allows you to continue claiming the main residence exemption even if the property is no longer where you live.

If you move out and the property is considered a rental investment property, you may still be able to avoid capital gains tax for a period. The 6 year exemption period begins when the property first starts producing rental income.

In simple terms, the rule works as follows:

- You live in the property and establish it as your main residence.

- You move out, and the property is considered a rental investment property.

- Within the 6 year period, the property can still be treated as your main residence for CGT purposes.

- If you sell the property within the 6 year timeframe, the gain may not be subject to capital gains tax.

This means the rule is a powerful way to reduce or even eliminate CGT if your property increases in value during that time.

If you move back into the property and use it again as your main residence, the 6 year exemption period may reset. This can allow you to rent the property again later while continuing to benefit from the exemption as part of a longer-term investment strategy.

However, if the property is rented for more than six years without being re-established as your main residence, part of the gain may become subject to capital gains tax. In that situation, you may need to pay capital gains tax on the portion of the gain that falls outside the exemption period.

When the 6-year rule doesn’t apply

The 6-year rule does not apply in every situation. Certain circumstances can limit or prevent the exemption from applying.

Common situations where the rule may not apply include:

- The property was never established as your main residence before it was rented

- The property is rented for more than six years without you moving back in

- You nominate another property as your main residence during the same period

- The property was mainly used to produce income from the beginning

If any of these situations occur, part or all of the profit from selling the property may be subject to capital gains tax.

This means a portion of the gain may be included in your net capital gain and reported in your annual income tax return. The outcome can affect your capital gains tax liability depending on how long the property produced rental income and how much the property value increased.

Because these rules interact with broader Australian tax rules, it is important to understand whether the property still qualifies for the exemption before you sell.

[tip_box]

Remember the capital gains time limit

It’s important to be aware of the capital gains time limit — if you exceed the six-year period without moving back in, your CGT exemption may no longer fully apply to your situation.

[/tip_box]

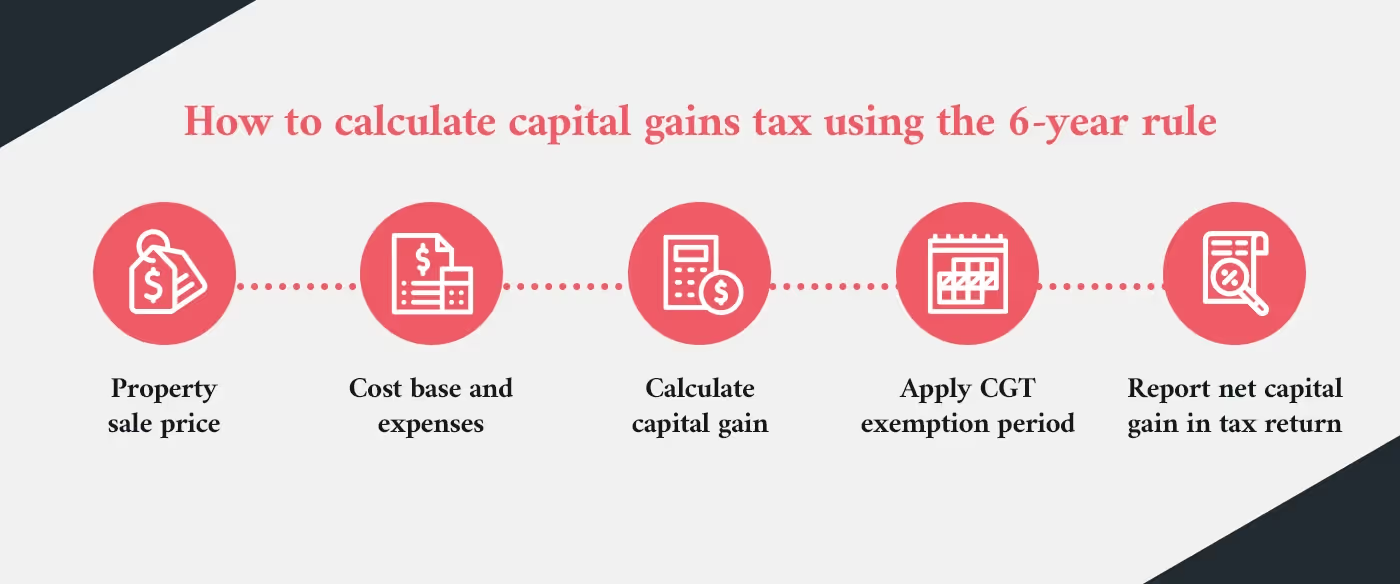

How to calculate CGT when using the 6-year rule

If the six-year rule does not fully apply, you may still need to calculate the taxable portion of the gain when the property is sold.

Capital gains tax is generally calculated by comparing the capital proceeds from the sale of the property with its cost base. The capital proceeds are the amount you receive when the property is sold, while the cost base includes the purchase price and certain costs associated with acquiring and holding the property.

A simple way to calculate the gain is:

- Work out the capital proceeds from selling the property.

- Subtract the property’s cost base to determine the capital gain.

- Identify the period the property qualified as your main residence.

- Determine how long the property was producing rental income outside the six year exemption period.

- Apportion the gain to calculate the amount that may be subject to capital gains tax.

For example, if you owned the property for more than 12 months and part of that time falls outside the exemption period, a portion of the gain may still be subject to capital gains tax. However, the remaining gain may qualify for the CGT discount.

The taxable portion of the gain becomes part of your net capital gain and is reported in your annual income tax return. Ensuring the gain is reported correctly is an important part of maintaining proper tax compliance.

Many property owners use a capital gains tax calculator to estimate the outcome before selling. This can help you understand whether the exemption may reduce or even eliminate CGT, or whether you may still need to pay capital gains tax on part of the profit.

Can you claim the 6-year rule on two properties?

The six-year CGT exemption rule only allows you to treat one property as your main residence at a time for capital gains tax purposes. This means you generally cannot apply the 6-year capital gains tax exemption to two properties simultaneously.

If you move out of your home and begin renting it out, the rule may allow you to continue treating that property as your main residence for tax purposes even while it produces income. During that period, you cannot nominate another property as your main residence unless you choose to stop claiming the exemption on the first property.

In practice, this means you must decide which one property will receive the capital gains tax exemption. If you nominate a new home as your main residence, the previous property may become subject to CGT when it is eventually sold.

The rule can still be valuable because it may allow you to treat a property as your place of residence for CGT for up to six years after you move out. This can provide significant CGT savings when you later sell your property.

However, it is important to consider the CGT implications before choosing which property to nominate as your main residence. The way the property is owned and structured can also influence the tax outcome. Selecting the right business structure can affect whether you pay tax on any profit or whether the gain remains exempt from capital gains tax.

Does the 6-year rule apply to foreign residents in Australia?

The 6-year primary residence exemption rule generally applies to Australian taxpayers who qualify for the main residence exemption. However, the rules are different if you become a foreign resident for tax purposes.

Under current Australian tax law, many individuals who are classified as foreign residents may lose access to the capital gains tax exemption for their former home. This means that when they sell their property, the gain may become subject to CGT, even if the property previously qualified as their main residence.

In these circumstances, the property may no longer be exempt from capital gains tax, and the owner may need to pay tax on any profit when the property is sold.

Because the rules can change depending on residency status, ownership history, and how long the property was used as a home, it is important to consider the CGT implications carefully before relying on the 6-year CGT exemption rule.

Professional advice from experienced property tax specialists can help determine whether the property is still eligible for the exemption and whether the rule can reduce your capital gains tax when you sell.

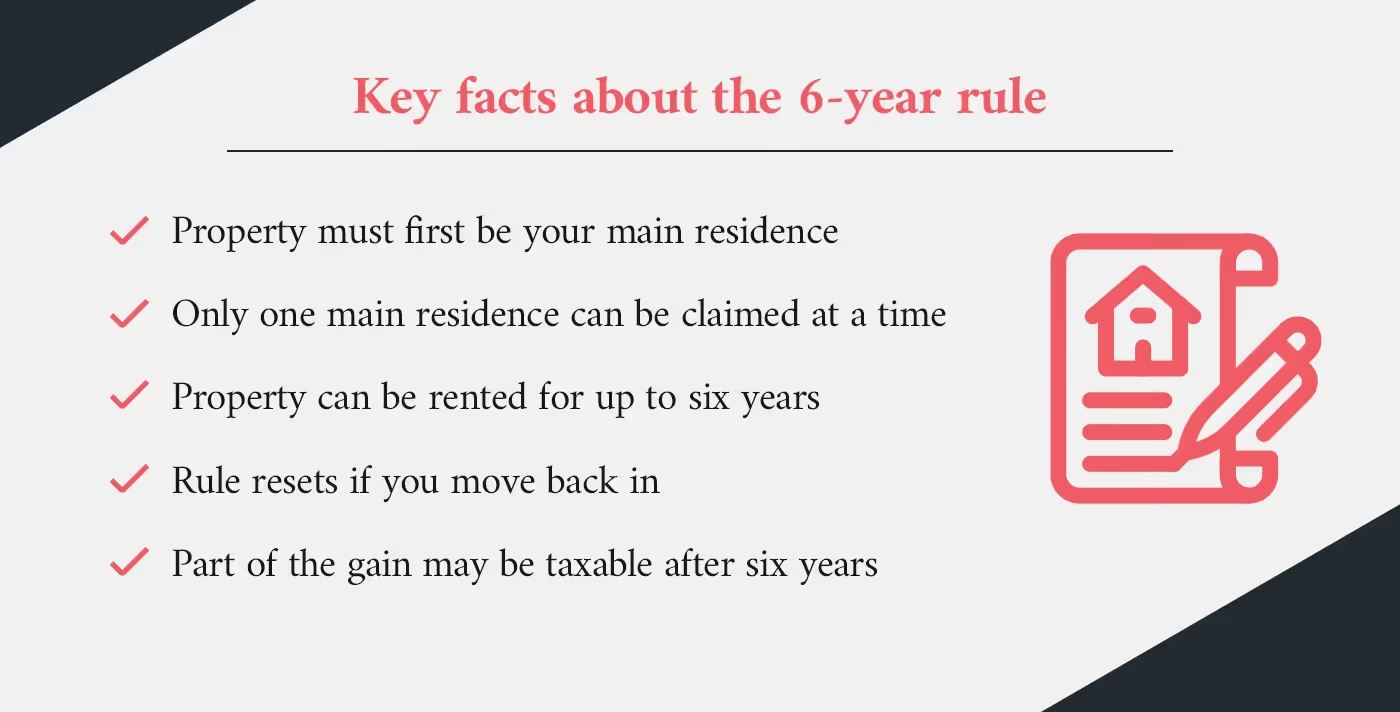

Key facts about the 6-year rule and who can claim it

The 6-year capital gains tax exemption can be a useful way to reduce or avoid CGT when a former home is rented out. However, several conditions must be met for the rule to apply.

Key facts to understand include:

- The property must first qualify as your main residence for tax purposes.

- You can only treat one property as your main residence at a time.

- The rule allows you to continue treating a property as your main residence for tax purposes even if it is rented out, for residence for up to six years.

- If you move back into the property and again use it as your home, the rule resets and a new six-year period may begin.

- If the property is rented for longer than six years without you moving back in, part of the gain may become subject to CGT.

- If you owned the property for more than 12 months, you may still be able to claim a CGT discount if you’re still eligible.

- The rule can significantly reduce your capital gains tax liability, but it is important to consider the CGT implications before you sell your property.

When used correctly, the six-year CGT exemption rule can be a valuable strategy to reduce your capital gains tax and improve long-term CGT savings when selling property.

Other CGT exemptions to know when selling a property

The six-year rule can reduce capital gains tax when selling a former home, but it is not the only concession available. Depending on your circumstances, other exemptions may also reduce your capital gains tax liability.

- Main residence exemption: If the property was your main residence for the entire ownership period, the gain may be exempt from capital gains tax when you sell your property.

- Partial exemption: If the property was your home for part of the ownership period but later became an investment property, only part of the gain may be subject to CGT.

- 50% CGT discount: If you owned the property for more than 12 months, individuals may be able to apply the 50% CGT discount to reduce the taxable gain.

- Six-month overlap rule: When moving between homes, the six-month overlap rule may allow two properties to be treated as your main residence for a short transition period.

- Pre-CGT asset exemption: Properties acquired before 20 September 1985 are generally exempt from capital gains tax under Australian tax rules.

- Superannuation property ownership: If a property is owned through a self-managed super fund, the capital gain may receive concessional tax treatment and may be exempt from CGT in pension phase.

- Increasing your cost base: Certain purchase, ownership, improvement and selling costs can be included in the property’s cost base, which can reduce the taxable capital gain when the property is sold.

Get expert help to maximise your 6-year rule CGT exemption

Understanding how the six-year rule applies can make a significant difference to the amount of tax you pay when completing a property sale. Small differences in how the property was used, how long it was rented, and how it was treated for tax purposes can affect whether the gain is exempt from capital gains tax or whether part of it becomes subject to CGT.

Getting the right CGT advice before selling property can help you understand how the main residence exemption, the six-year rule and other concessions may apply to your situation. Strategic planning for tax minimisation can ensure the correct exemptions are applied and that you do not pay more capital gains tax than necessary.

At Liston Newton, our advisory team works with business owners and property investors to review ownership timelines, rental periods and tax reporting requirements before a property sale takes place. This helps identify opportunities to reduce capital gains tax and ensure the correct exemptions are applied.

If you are planning a property sale and want to understand how the six-year rule may apply to your circumstances, professional CGT advice can help ensure the outcome is structured as effectively as possible.

[free_strategy_session]

Book a free property investment strategy session

Maximise your property’s value and minimise your tax with expert guidance. In a free 90-minute strategy session, we’ll help you:

- Understand how CGT exemptions, including the six-year rule, apply to your situation.

- Gain an understanding of approximate capital gains in relation to your situation.

- Gain clarity on your next steps to make informed, tax-effective investment decisions.

Take the guesswork out of property tax planning.

[/free_strategy_session]