[section id="what-is-payroll-tax" format="overview"]

As your business scales, your financial responsibilities evolve. Payroll tax is a state tax on wages paid by employers once their total Australian wages are over the set limit. It is calculated on taxable wages such as salaries, superannuation, bonuses, and certain contractor payments.

While it is a sign of a growing, successful team, it also introduces a new layer of compliance. At Liston Newton, we view payroll tax not just as a lodgement requirement, but as a key milestone in your business's long-term financial journey.

For growing businesses, understanding payroll tax is essential. If your wage bill increases, expands into new states, or you operate through multiple entities, your payroll tax position can change quickly. Getting clarity early helps you stay compliant and plan for growth with confidence.

[/section]

[section id="who-needs-to-pay-payroll-tax" format="ul"]

Who needs to pay payroll tax?

In Australia, payroll tax only applies once your wage bill reaches a certain level. Each state and territory sets its own annual payroll tax threshold and tax rate, which determines when your wages become liable.

That means you may need to pay your payroll tax if:

- You employ staff or engage certain contractors in a state or territory

- Your total Australian taxable wages for the group exceed that state or territory’s annual or monthly limits

- You are part of a group of related businesses, and the combined wages for the group exceed the limit

If your wages are below the relevant limit, you generally will not pay payroll tax. However, you still need to monitor your wage bill. Growing headcount, salary increases, or expansion into new locations can quickly push you over the limit. A taxation accountant can help you forecast when you might become liable and plan ahead.

[/section]

[section id="what-payments-are-included-in-payroll-tax" format="ul"]

What payments are included in payroll tax?

Payroll tax applies to most payments you make to employees in return for their services.

In most states and territories, taxable wages include:

- Salaries and wages, including overtime and paid leave

- Superannuation contributions

- Bonuses, commissions, and incentive payments

- Allowances, such as travel, meal, and site allowances

- Fringe benefits and other non-cash benefits

- Director fees and similar remuneration

- Eligible termination payments, such as some redundancy or severance payments

- Certain contractor payments, when the arrangement is treated as a relevant contract

Some payments may be exempt from payroll tax, and the rules differ between states. If you are unsure, speak with a business accountant.

Once your wage bill exceeds the threshold, these payments and benefits mean your wages are subject to payroll tax in that state.

[/section]

[section id="do-contractors-count-for-payroll-tax" format="mixed"]

Do contractors count for payroll tax?

In many cases, yes. Contractor payments may be included in your taxable wages if the contract is mainly for the contractor’s labour. This type of arrangement is often called a relevant contract.

Contractor payments are more likely to be subject to payroll tax when the contractor:

- Works for your business on an ongoing basis

- Performs core duties similar to those of your employees

- Does not employ their own staff to perform the work

[section_inner_1 id="when-might-the-contractor-payments-be-exempt" format="ul"]

When might the contractor payments be exempt?

Possible exemptions include:

- Genuine one-off or short-term projects

- Contractors who provide services to many unrelated clients

- Contracts mainly for goods, materials, or equipment

Since each state revenue office applies its own rules and exemptions, you should treat contractor payments as a key focus area in any payroll tax review.

[/section_inner_1]

[/section]

[section id="payroll-tax-vs-payg-withholding-whats-the-difference" format="table"]

Payroll tax vs PAYG withholding: what’s the difference?

It is common for business owners to confuse payroll tax with PAYG withholding. They both relate to wages paid, but they are distinct obligations managed by different levels of government. Understanding the difference is a critical step in building a strong financial foundation.

- Payroll tax is a state and territory tax on wages paid by employers. It is an additional cost the employer must pay once their total Australian wages exceed a specific threshold.

- PAYG (Pay As You Go) withholding is a federal system managed by the Australian Taxation Office (ATO). Under this system, you withhold tax from your employees’ wages and remit it to the federal government on their behalf to help them meet their personal income tax liabilities.

[table]

[thead]

[tr]

[th]Feature[/th]

[th]Payroll Tax[/th]

[th]PAYG Withholding[/th]

[/tr]

[/thead]

[tbody]

[tr]

[td]Who pays it?[/td]

[td]Paid by the employer, in addition to wages[/td]

[td]Deducted from the employee's wages and remitted to the ATO.[/td]

[/tr]

[tr]

[td]Who receives it?[/td]

[td]Paid to the relevant state or territory revenue office[/td]

[td]Paid to the ATO[/td]

[/tr]

[tr]

[td]When is it paid?[/td]

[td]Only when total wages exceed a certain threshold[/td]

[td]Must be withheld from the very first dollar paid to an employee[/td]

[/tr]

[tr]

[td]Purpose[/td]

[td]Provides state and territory revenue. This tax helps fund essential public services and infrastructure.[/td]

[td]Acts as a pre-payment of the employee's personal income tax[/td]

[/tr]

[/tbody]

[/table]

In practice, you may pay your payroll tax to several state revenue offices if your group’s total Australian taxable wages exceed wage thresholds across different jurisdictions. At the same time, you will withhold PAYG from employee wages through the ATO system.

A clear understanding of both sets of payroll tax obligations helps your organisation avoid unexpected tax payable and stay compliant from 1 July through to the end of each financial year.

Since payroll tax administration is handled by separate state revenue offices, rules and thresholds differ across Australia.

[tip_box]

Proactive tip: If your business is scaling quickly, you may become liable for both. PAYG runs with regular payroll, but payroll tax needs separate monitoring, so you register as you approach the threshold.

[/tip_box]

[/section]

[section id="payroll-tax-obligations-what-employers-need-to-know" format="mixed"]

Payroll tax obligations: what employers need to know

Once you cross the payroll tax threshold, you move from monitoring to managing an ongoing obligation.

From that point, your business must:

- Register with the relevant state or territory revenue office

- Track taxable wages each month or quarter

- File payroll tax returns on time

- Complete an annual reconciliation at the end of the financial year

Getting these steps right helps you manage tax payable, avoid penalties, and build a strong compliance record as your business grows.

[section_inner_1 id="when-do-you-need-to-lodge-payroll-tax" format="ul"]

When do you need to lodge payroll tax?

You generally need to submit payroll tax returns once:

- Your total taxable wages are over the payroll tax threshold in a state or territory

- Or your state revenue office tells you that you must register for payroll tax based on your wage projections

Most employers will:

- Estimate annual wages at the start of the financial year

- Lodge monthly or quarterly returns, depending on the jurisdiction

- Complete an annual return or annual reconciliation at the end of each financial year

If your wages fluctuate, you may fall above the threshold in some periods and below in others. You should still file returns in accordance with the rules of that state, and report actual wages paid or payable for each period.

If you think your wage bill will increase significantly, contact your state revenue office or your taxation accountant early. It is much easier to register and submit on time than to retrospectively fix missed periods.

[/section_inner_1]

[section_inner_1 id="payroll-tax-thresholds-by-state-and-territory-australia" format="table"]

Payroll tax thresholds by state and territory (Australia)

Payroll tax thresholds and payroll tax rates are set separately by each state and territory. Once your overall taxable wages exceed the relevant threshold, your business must pay payroll tax in that state or territory.

[table]

[thead]

[tr]

[th]State / territory[/th]

[th]Monthly / weekly threshold[/th]

[th]Annual wages threshold[/th]

[th]Payroll tax rate*[/th]

[/tr]

[/thead]

[tbody]

[tr]

[td]VIC[/td]

[td]$83,333 (monthly)[/td]

[td]$1,000,000[/td]

[td]4.85% (metropolitan)[/td]

[/tr]

[tr]

[td]NSW[/td]

[td]$92,055 (28-day month) / $98,630 (30-day month) / $101,918 (31-day month)[/td]

[td]$1,200,000[/td]

[td]5.45%[/td]

[/tr]

[tr]

[td]ACT[/td]

[td]$166,666.66 (monthly)[/td]

[td]$2 million [/td]

[td]6.85% (A new 8.75% rate applies to wages >$150 M from 1 Jan 2026)[/td]

[/tr]

[tr]

[td]QLD[/td]

[td]$25,000 (weekly) /

$108,333 (monthly)[/td]

[td]$1.3 million [/td]

[td]4.75% (Rate increases to 4.95% for wages >$6.5M)[/td]

[/tr]

[tr]

[td]NT[/td]

[td]$208,333 (monthly)[/td]

[td]$2.5 million [/td]

[td]5.5%[/td]

[/tr]

[tr]

[td]WA[/td]

[td]$83,333 (monthly)[/td]

[td]$1,000,000 [/td]

[td]5.5%, with $950,000–$7.5 million receiving a diminishing threshold[/td]

[/tr]

[tr]

[td]SA[/td]

[td]$125,000 (monthly)[/td]

[td]$1.5 million [/td]

[td]Variable from 0% to 4.95%[/td]

[/tr]

[tr]

[td]TAS[/td]

[td]$95,890 (28-day month) / $102,740 (30-day month) / $106,164 (31-day month)[/td]

[td]$1.25 million [/td]

[td]4% ($1.25M to $2M)

6.1% (>$2M)[/td]

[/tr]

[/tbody]

[/table]

*Rates and thresholds may change. Check with the relevant state revenue office for current figures.

In South Australia and the Northern Territory, regional employers may access concessional payroll tax rates once they meet the eligibility criteria.

If your wage bill is approaching any of these thresholds, it is time to review your position. A taxation accountant can help you estimate future wages, assess which states you may become liable in, and set up a process to monitor thresholds and register returns on time.

[/section_inner_1]

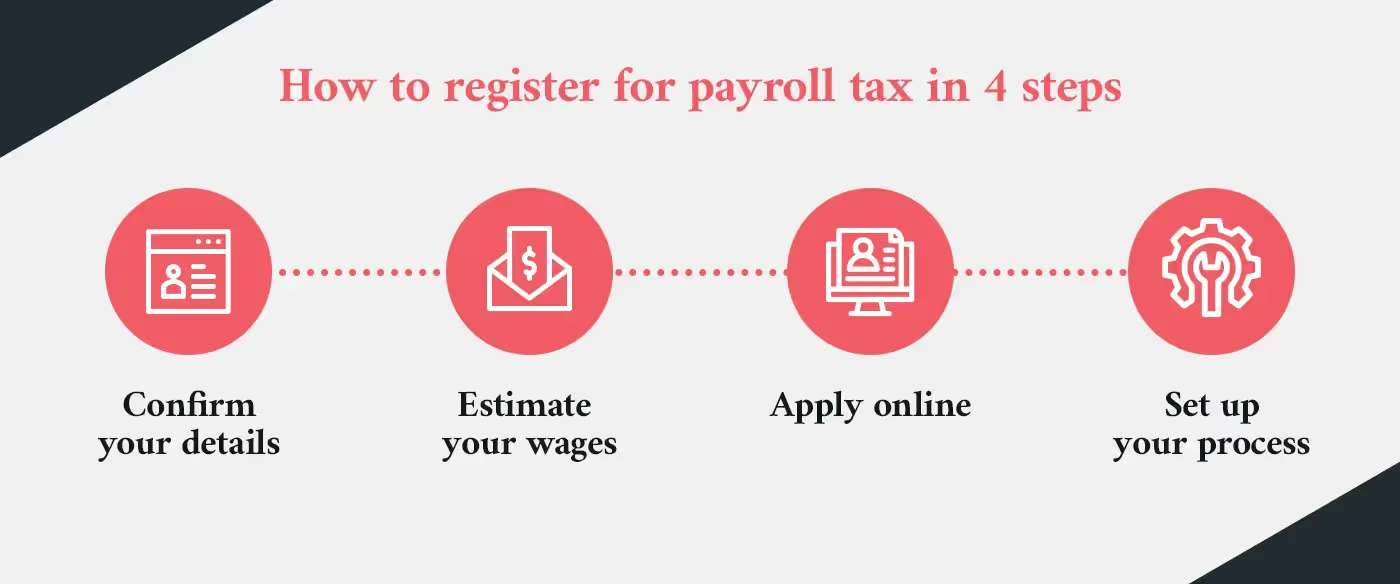

[section_inner_1 id="how-to-register-for-payroll-tax" format="process"]

How to register for payroll tax

Once you need to register for payroll tax, the process is usually completed online with your state or territory revenue office. An employer must register for payroll when their total wages are expected to exceed the relevant threshold, not just after they have already passed it.

Step 1: Confirm your business details

When you start the registration, you will be asked for:

- Your Australian Business Number (ABN).

- Your legal entity name and any trading names.

- A business address and contact details.

- A primary contact for payroll and tax queries.

Step 2: Estimate your wages

Revenue offices want to understand your expected wage bill for the financial year.

You will generally need to provide:

- Estimated total Australian taxable wages for the current financial year.

- A breakdown of wages in each state or territory.

- Details of any grouped entities, where the group’s wages are combined to test the threshold.

This information helps the revenue office decide from which date you must register and pay payroll tax.

Step 3: Complete the online registration form

You then complete the registration through the relevant state or territory revenue office portal:

- Confirm the date your wage bill first exceeded, or is expected to exceed, the threshold.

- Answer questions about your business structure and payroll tax obligations.

- Nominate how often you will lodge returns, such as monthly or quarterly.

Once approved, you will receive details of how to register and pay payroll tax and access the online lodgement system.

Step 4: Set up your internal process

Registration is only the beginning. To stay compliant, you should:

- Configure your payroll system to track taxable wages by jurisdiction, including interstate wages.

- Assign clear responsibility for preparing and lodging payroll tax returns.

- Create a calendar of lodgement and payment dates, including the annual reconciliation at the end of each financial year.

- Keep supporting records so you can respond to any revenue rulings, reviews, or audits.

Your employer obligations do not end at registration. You must register and pay payroll tax on time, lodge accurate returns, and keep records in accordance with the Payroll Tax Act and revenue rulings in each jurisdiction.

[/section_inner_1]

[section_inner_1 id="payroll-tax-example-how-it-works-in-victoria" format="overview"]

Payroll tax example: how it works in Victoria

Gary runs an equipment hire business in Victoria with four employees. Each employee earns $67,500 per year, and the business pays 12% Super Guarantee on top of ordinary time earnings. The employees work at a fixed location and do not receive allowances or fringe benefits.

Gary also pays himself a salary of $130,000 per year, plus 12% super.

Gary’s estimated Victorian taxable wages (including super) are:

- Employees: $67,500 × 1.12 = $75,600 each → $75,600 × 4 = $302,400

- Gary: $130,000 × 1.12 = $145,600

- Total: $448,000 per year (around $37,333 per month)

Because Gary’s total Victorian wages are below the Victorian payroll tax-free threshold of $1,000,000 (from 1 July 2025), the business is not required to pay payroll tax at this stage.

[/section_inner_1]

[section_inner_1 id="payroll-tax-for-businesses-operating-across-multiple-states" format="ul"]

Payroll tax for businesses operating across multiple states

If your organisation operates across several Australian states and territories, payroll tax becomes more complex. Revenue offices look at your total Australian taxable wages, not just wages in one location.

Key points for multi-state employers include:

- You must identify the state or territory in which each employee’s wages are liable for payroll tax.

- Interstate wages are considered when testing whether your wage bill exceeds the tax-free threshold in each jurisdiction.

- You may be required to register in multiple states and lodge returns separately for each.

Most states use harmonised rules to decide where wages are taxable, often based on:

- Where the employee usually works.

- Where the employee is based, if they work across several locations.

- Where wages are paid, if no other test resolves the position.

Getting this analysis right is critical. Incorrectly allocating wages can lead to underpaid payroll tax in one state and overpaid amounts in another. A clear view of group wages helps you manage your payroll tax liability across different states and territories.

Example: payroll tax across two states

Gary’s equipment hire business is headquartered in Victoria.

As the business grows, he expands into Tasmania and hires:

- Tasmania: three staff on $67,500 per year, plus a store manager on $85,000 per year

- The business pays 12% super on top of salaries.

At the same time, Gary’s Victorian operations have also grown.

Across the group, his wages now look like this:

- Victoria taxable wages (including super): about $952,000 per year

- Tasmania taxable wages (including super): about $322,000 per year

- Total Australian taxable wages (including super): about $1,274,000 per year (around $106,167 per month)

What this means for payroll tax:

- Victoria: Because the group’s total Australian wages exceed Victoria’s $1,000,000 threshold, the business must register for payroll tax in Victoria. Victorian payroll tax is then calculated on Victorian taxable wages (after applying Victoria’s threshold rules), generally at 4.85% for metropolitan employers.

- Tasmania: Even though the business has staff in Tasmania, Tasmanian wages are still below Tasmania’s $1.25 million threshold, so no payroll tax is payable in Tasmania yet.

[/section_inner_1]

[/section]

[section id="payroll-tax-for-grouped-businesses-and-common-grouping-rules" format="ul"]

Payroll tax for grouped businesses (and common grouping rules)

Payroll tax grouping rules combine the wages of related businesses to determine whether payroll tax is payable. If the group’s total Australian wages exceed the threshold in a state or territory, the group must register for payroll tax.

You may be grouped if entities share:

- Common ownership

- Common directors or decision-makers

- Related-entity structures

- Employment relationships where workers are shared

When businesses form a group:

- Only one entity in the group can claim the payroll tax threshold deduction, while the other entities pay tax from the first dollar

- All entities must lodge returns if required by their revenue office

- All members are jointly and severally liable for the payroll tax payable

Grouping rules apply even when each entity operates independently. The key factor is the relationship between the owners or controllers, not the day-to-day operations. If your business structure has grown or changed, review your group status each financial year.

[/section]

[section id="what-happens-if-you-miss-payroll-tax-lodgements" format="ul"]

What happens if you miss payroll tax lodgements?

Missing a payroll tax lodgement can lead to interest, penalties, and compliance action from your state or territory revenue office. Because payroll tax is a self-assessed state tax, the employer is responsible for monitoring wage levels, registering on time, and lodging accurate returns. If returns are missed or lodged late, revenue offices can review your wages and reassess tax payable for previous periods.

Consequences of missed or late payroll tax lodgements

- Interest charges apply on outstanding tax from the original due date.

- Penalty tax may be imposed, especially where wages were not reported or registration was delayed.

- Revenue offices may issue default assessments based on their own wage estimates.

- Your business may face a payroll tax audit, where wage records across all entities in the group are examined.

- Long-term non-compliance can affect your standing with revenue offices and increase scrutiny in future years.

[section_inner_1 id="why-does-timely-lodgement-matter" format="overview"]

Why does timely lodgement matter?

Payroll tax is calculated on wages paid or payable, and those wages accumulate quickly during the financial year. A small delay in registration can result in several months of tax payable being due at once. Late lodgements can also affect your annual reconciliation, which must be completed at the end of each financial year.

If you realise you have missed a lodgement or believe your total Australian wage bill exceeds the threshold, it is best to act early. Contact your taxation accountant or the relevant revenue office to correct the position before penalties escalate. Revenue offices are generally more flexible when employers come forward voluntarily.

[/section_inner_1]

[/section]

[section id="get-help-with-payroll-tax-compliance" format="cta"]

Get help with payroll tax compliance

As a small business, you may not meet the payroll tax threshold. But your business might grow, and you might take on more employees.

When you do, it's important that you make an accurate self-assessment of your payable wages and benefits to ensure you lodge your payroll tax correctly and on time.

Ready to review your position? Speak with a taxation accountant, explore our business accounting services, or get support with tax compliance so your payroll tax stays on track.

[/section]

Table of contents