A family trust is a legal structure where a trustee holds and manages assets under a trust deed and distributes income to beneficiaries. The Australian Taxation Office (ATO) generally taxes the beneficiaries on the income they receive, rather than the trust itself, as outlined in the ATO’s guidance on family trusts.

The trustee is responsible for managing the trust and deciding how income or capital is distributed each year. These decisions must follow the rules set out in the trust deed, which establishes the trust, defines the beneficiaries, and governs how the trust operates.

In many Australian businesses and investment structures, a family trust is used to hold assets such as shares, property or business interests. Because the trustee can distribute income among beneficiaries each year, the structure can provide flexibility for tax planning, asset protection and managing family wealth over time.

[general_awards] [/general_awards]

Types of family trusts in Australia

There are several types of family trusts in Australia. The main difference between them relates to how beneficiaries receive income and how control over the trust is structured.

While the term “family trust” is often used broadly, it usually refers to a discretionary trust that manages family assets and income. Common trust structures include:

Discretionary trust (family trust)

A discretionary trust is the most common type of family trust. The trustee has discretion to determine how trust income and capital are distributed among beneficiaries each year, in accordance with the terms of the trust deed. This allows the trustee to respond to changing financial circumstances within the family group.

Unit trust

In a unit trust, beneficiaries hold units similar to shares. Income and capital distributions are made in proportion to the number of units held, rather than at the trustee’s discretion. Unit trusts are commonly used when several parties invest together in an asset such as property.

Hybrid trust

A hybrid trust combines elements of both discretionary and unit trusts. Some beneficiaries may hold fixed entitlements through units, while the trustee retains discretion over distributions of other income. These arrangements can be more complex and typically require careful structuring.

Each type of trust operates under its own rules, but in most family structures, the trustee manages trust assets and distributes income to beneficiaries in accordance with the trust deed.

What are the tax benefits of a family trust?

The advantages of a family trust include strategic income distribution, reduced tax liability, and asset protection. In some cases, a family trust may also qualify for a tax concession, such as small business CGT relief or other government incentives, depending on eligibility criteria. Unlike a company, a trust itself does not pay tax. Beneficiaries are taxed at their individual rates, allowing for potential tax savings when income is allocated effectively.

However, contributions to a family trust are generally not tax-deductible. Unlike superannuation contributions, which can be claimed as deductions, transferring money or assets into a family trust is considered a private transaction. That said, once assets are inside the trust, they can be managed in a tax-effective way — distributing income to beneficiaries in lower tax brackets and reducing the overall tax obligation.

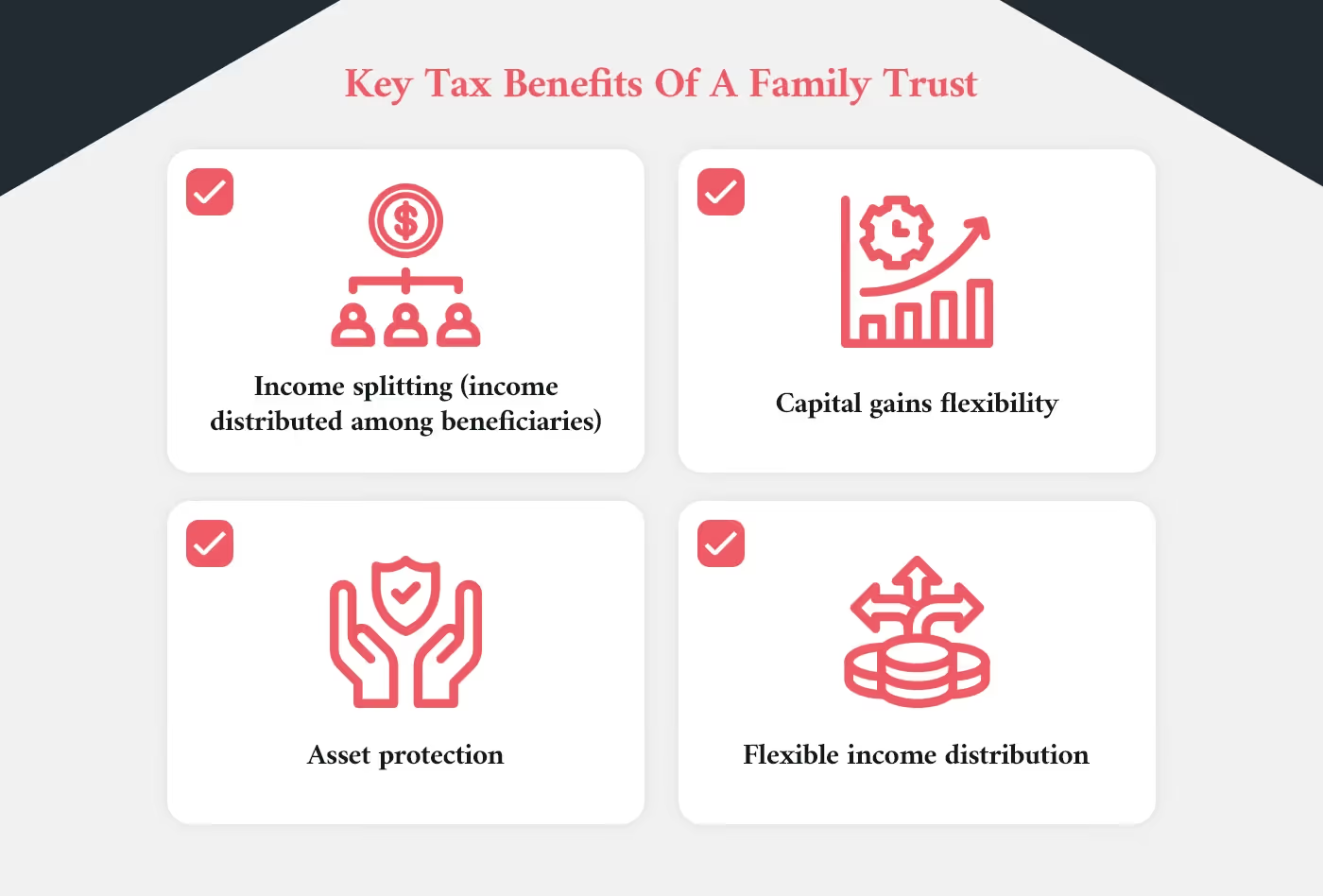

Some of the main family trust tax benefits include:

- Income splitting across beneficiaries: Trust income can be distributed to beneficiaries in different tax brackets, which may reduce the total tax paid across the family group. Each beneficiary generally pays tax on their share of trust income at their individual marginal tax rate.

- Capital gains tax flexibility: When a trust sells assets such as property or shares, the capital gain may be distributed to beneficiaries, who then include that amount in their own tax return. In some cases, beneficiaries may access the capital gains tax (CGT) discount if the eligibility conditions are met.

- Asset protection advantages: Assets held in a trust are legally owned by the trustee on behalf of beneficiaries, rather than by individuals directly. This structure can provide a level of protection if a beneficiary faces personal liabilities.

- Flexibility in distributing income: The trustee can determine how income is allocated each year, provided the distribution follows the rules in the trust deed and complies with ATO requirements.

Although these benefits can be significant, the tax outcomes of a family trust depend on how the trust is established and managed, as well as how income is distributed to beneficiaries.

[free_strategy_session]

Download our tax minimisation guide

This guide could help reduce your tax bill and improve your financial position

Inside you’ll find practical strategies and essential information to help you minimise tax legally and effectively—whether you're an individual, investor or business owner.

- Understanding legitimate tax deductions and offsets

- How to structure your business to reduce tax

- The benefits of super contributions and trust structures

- Tax-effective investment strategies

- Common tax traps and how to avoid them

[/free_strategy_session]

Family trust tax rates in Australia

A family trust typically pays no tax on income earned within the trust. Instead, the income is distributed to the beneficiaries, who are taxed at their personal tax rates. However, a family trust cannot distribute a tax loss to beneficiaries. If a trust incurs a tax loss, it must be carried forward within the trust and offset against future income rather than passed on.

The fund's trustee decides who within the family receives the distributions. They are free to distribute the income to as many beneficiaries as they see fit. You can always check your trust deed to determine which beneficiaries are eligible.

The table below summarises how family trust income is typically taxed.

[table]

[thead]

[tr]

[th]Recipient of trust income[/th]

[th]How the income is taxed[/th]

[th]Key consideration[/th]

[/tr]

[/thead]

[tbody]

[tr]

[td]Adult beneficiary (Australian resident)[/td]

[td]Taxed at the individual’s marginal tax rate[/td]

[td]Income is included in the beneficiary’s personal tax return[/td]

[/tr]

[tr]

[td]Company beneficiary[/td]

[td]Taxed at the company tax rate (currently 25% for base rate entities)[/td]

[td]Often used to retain profits within a corporate structure[/td]

[/tr]

[tr]

[td]Minor beneficiary[/td]

[td]Generally taxed at higher penalty tax rates[/td]

[td]Rules are designed to discourage income splitting to children[/td]

[/tr]

[tr]

[td]Trustee (undistributed income)[/td]

[td]Taxed at the highest marginal tax rate[/td]

[td]Occurs when no beneficiary is presently entitled to the income[/td]

[/tr]

[/tbody]

[/table]

Understanding how trust income is allocated and taxed is essential when managing a family trust, as the tax outcome depends on which beneficiary receives the distribution.

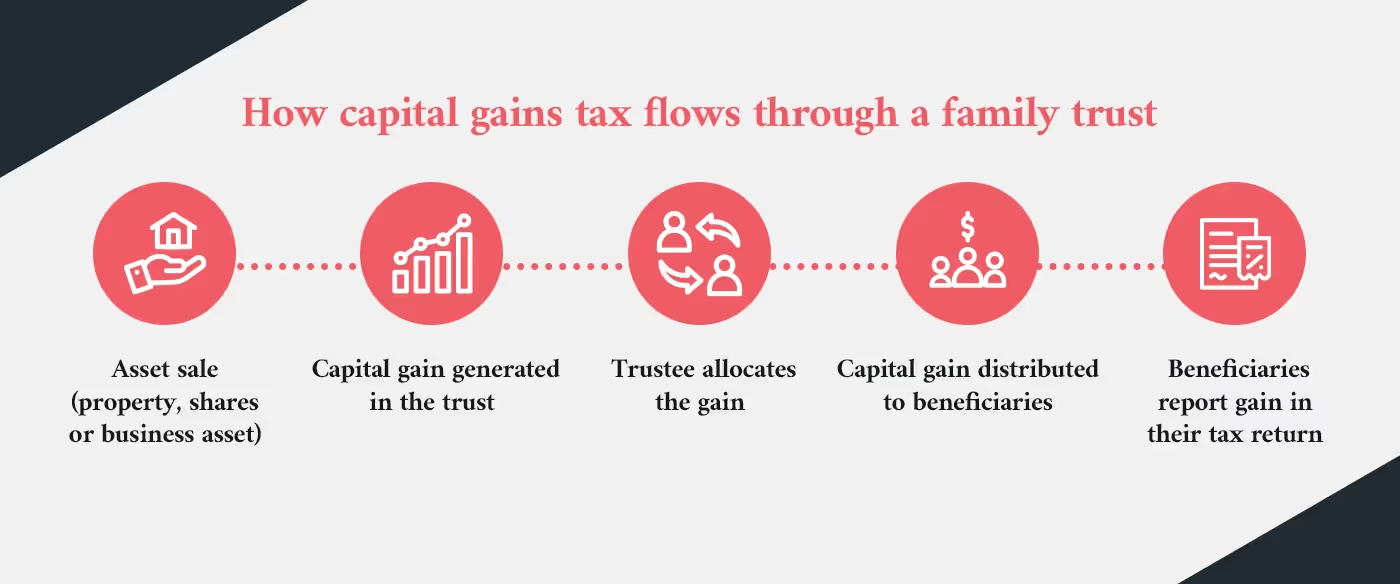

Do beneficiaries pay capital gains tax through a family trust?

Yes. When a family trust sells an asset such as property, shares or a business interest, the resulting capital gain is generally passed through to beneficiaries rather than being taxed at the trust level.

In most cases, the capital gain flows through the trust to the beneficiaries, who then include their share of the gain on their personal tax returns. This approach reflects the way family trusts are taxed in Australia, where trust income and gains are assessed to beneficiaries who are presently entitled to the distribution.

Several factors influence how family trust capital gains tax in Australia is calculated, including:

- whether the asset qualifies for the capital gains tax (CGT) discount

- how the trust deed allows capital gains to be distributed

- which beneficiaries receive the capital gain

- whether any small business CGT concessions apply.

For example, if a trust sells an asset held for more than 12 months, the 50% CGT discount may apply before the capital gain is distributed to beneficiaries. Each beneficiary then includes their share of the net capital gain in their tax return and pays tax based on their individual circumstances.

Because capital gains can be distributed to specific beneficiaries in some trust structures, careful planning is often required to ensure their distribution aligns with tax rules and the trust deed.

How family trusts are taxed in Australia

In Australia, a family trust generally does not pay tax on its income. Instead, trust income is distributed to beneficiaries, who include their share in their personal tax return.

The trustee manages the trust and determines how trust income is distributed each financial year, in line with the trust deed. Beneficiaries who are presently entitled to trust income are responsible for paying tax on that income at their individual marginal tax rate.

Several factors affect how family trusts are taxed in Australia:

- Trust income is assessed to beneficiaries, including business income, investment income or other earnings from trust assets.

- If no beneficiary is presently entitled to the income, the trustee may be taxed at the highest marginal tax rate.

- Certain income types, including capital gains and franked distributions, may be streamed to specific beneficiaries where the trust deed allows it.

Family trusts must also lodge an annual trust tax return with the ATO and maintain records showing how trust income was distributed to beneficiaries.

Example of how a family trust distributes income

Each year, the trustee decides how trust income will be distributed among the beneficiaries, in accordance with the trust deed. The decision is recorded in a distribution resolution before the end of the financial year.

A simplified example of family trust income distribution rules:

- The trust earns income: Income may come from a family business, investments or assets like property held in a trust.

- The trustee reviews the trust income before 30 June: The trustee considers the tax position of each beneficiary of the trust.

- A distribution resolution is prepared: The document records which beneficiaries are presently entitled to the trust income.

- Income is allocated to beneficiaries: The trustee distributes income across members of the family group.

- Beneficiaries report the income in their tax return: Each beneficiary includes their share of the trust income and pays tax based on their individual tax rate.

This process allows a family trust structure to distribute income among beneficiaries while complying with the trust deed and Australian Taxation Office (ATO) rules.

Non-resident and minor beneficiary tax rules

Additional tax rules apply when a family trust distributes income to non-resident or minor beneficiaries. These rules affect how trust income is taxed and may change the tax implications of a distribution. Key rules include:

Non-resident beneficiaries

If a trust distributes income to a non-resident beneficiary, the trustee may be required to withhold tax and remit it to the ATO. Trustees should also be aware of the family trust distributions tax, which may apply when certain distributions are made outside the family group.

Minor beneficiaries

Distributions to minors (under 18 years old) are usually taxed at penalty tax rates on most forms of trust income. These rules limit the ability to reduce tax by distributing income to children.

Expected income

Some income may qualify as excepted income, meaning minors may be taxed at normal rates. This can apply to income derived from employment or certain inheritances paid into a trust fund.

Because of these rules, trustees must consider the tax implications of each distribution decision and ensure the trust continues to comply with ATO requirements and the trust deed.

Family trust setup costs and ongoing expenses

When many families set up a family trust, the structure is created to hold assets such as investments, a family home, or business interests. While a family trust can provide flexibility for managing income and assets, establishing and running the structure involves both setup costs and ongoing expenses.

The cost to set up a family trust varies depending on the level of advice required and the structure's complexity. Professional advice is usually recommended when a trust is created, as the trust deed and setup arrangements determine how the trust operates and distributes income.

[table][thead][tr][th]Cost type[/th][th]Typical expense[/th][th]What it covers[/th][/tr][/thead][tbody][tr][td]Initial setup[/td][td]Often $1,500–$3,500 depending on structure and advice[/td][td]Legal documents, preparation of the trust deed, and establishing the trust structure when you set up a trust[/td][/tr][tr][td]Accounting and tax compliance[/td][td]Annual accounting and tax return fees[/td][td]Preparation of financial statements and the family trust tax return</td>[/tr][tr][td]Ongoing administration[/td][td]Varies depending on trust activity</td>[td]Managing records, preparing distribution resolutions and overseeing trust assets</td>[/tr][/tbody][/table]

A family trust allows assets and income to be managed under a structured legal arrangement, but the costs and administrative responsibilities should be considered before deciding to use one. Professional advice from a taxation accountant can help ensure the trust is structured correctly from the start.

How franked distributions are taxed in a family trust

A franked distribution is a dividend paid by an Australian company with franking credits attached. These credits represent the tax the company has already paid.

When dividends are held in a family trust, the income and franking credits can be distributed to family trust beneficiaries. In most cases, the trust does not pay tax. Instead, the income and credits are distributed among family members.

The beneficiaries include both the dividend income and the franking credit in their personal tax return. The franking credit can then reduce the tax payable on that income.

A properly structured family trust may allow trustees to allocate franked dividends to family members in lower tax brackets. This can increase the benefit of family members receiving income through the trust structure.

Several factors influence how franked distributions are taxed:

- The trust deed must allow income streaming.

- The trustee decides how income is distributed among family trust beneficiaries.

- The trust structure may include a family company acting as trustee.

- A family trust election may affect how income can be distributed within the family group.

Because franking credits represent tax already paid by the company, trustees must ensure that distributions comply with the ATO rules and the trust deed.

Do family trusts pay land tax in Australia?

Yes, a family trust may pay land tax in Australia if land is held in a family trust. Land tax is set by each state or territory, so rules and thresholds vary across jurisdictions.

When property is held in a family trust, the land tax treatment can differ from property owned by individuals. Some states apply lower thresholds or additional surcharges to trust structures.

A family trust is a type of discretionary trust. In many cases, the family trust is a discretionary structure used to hold investments, property or business assets. This allows income to be distributed among family members each year.

Family trusts can also hold land used to run a family business, including commercial property. In these cases, the property is held in a family trust rather than owned by individuals.

However, holding land in a trust can change the tax implications of property ownership. Trust land may be taxed differently under state land tax rules.

Many families establish a family trust for tax planning and asset protection, particularly when switching from a sole trader to a trust. But the advantages of a family trust should be weighed against potential land tax costs.

Before deciding to establish a family trust to hold property, it is important to review the state-based land tax rules and consider how the structure will affect the overall tax position.

Do family trusts need to lodge a tax return?

Yes. A family trust must lodge an annual trust tax return if the trust earns income during the financial year.

Although a trust does not pay tax in most situations, the trustee must still report how the trust income was distributed among family trust beneficiaries. This information allows the ATO to assess tax correctly for each beneficiary.

The trust tax return generally includes:

- the total trust income earned during the year

- details of how income was distributed among family members

- any capital gains, franked distributions or other investment income

- the beneficiaries who are presently entitled to the income.

The trustee is responsible for ensuring the trust tax return is lodged on time and that records support the distribution decisions made under the trust deed.

Many families use a family trust to manage assets, investments or a family business, so accurate reporting is essential. A properly structured family trust helps ensure the income distributions and tax reporting remain compliant each year. Ongoing business accounting support can help ensure the trust remains compliant each year.

Set up your family trust with professional guidance

At Liston Newton, we help establish and manage family trusts so the structure is set up correctly from the start. Our team provides guidance on trust setup, compliance requirements and ongoing management under Australian tax rules.

If you are considering a trust structure, we can help ensure your family trust is established properly and remains compliant over time.

[free_strategy_session]

Book a free family trust strategy session

A 90-minute strategy session gives you a clear plan for setting up and managing your family trust.

- Get a better understanding of how a family trust fits your goals.

- Receive a detailed report outlining tax benefits and asset protection strategies.

- Understand your next steps to maximise tax savings and secure your family’s wealth.

[/free_strategy_session]